FPE #3: How economics can help you think rationally during bubbles

In today’s Finshots Pocket Economics, Edition #3, we’re talking about financial bubbles and how economics can help you avoid falling for real-life bubble-like situations.

Okay, that’s no guarantee, but at least you’ll learn how to think a little more rationally when everyone else is losing their minds.

But before we begin, here’s a quick recap of what we wrote over the past week. On Monday, we wrote about a different kind of futures contract whose underlying asset is rainfall. On Tuesday, we explained India’s plan to build a gas pipeline to Oman. On Wednesday, we wrote about why Japan’s 7-Eleven works so differently and three lessons Toshifumi Suzuki left behind for retail. On Thursday, we talked about the Indian Premier League (IPL) and why its growth is slowing. And on Friday, we wrote about Airtel’s new trick up its sleeve to get ahead in the revenue race.

With that out of the way, let’s dive into FPE, Edition #3.

Hey folks!

Last week, something so interesting happened that it felt perfectly timed for us to use as the opening anecdote for this edition.

Thanks to Prime Minister Narendra Modi! During his visit to Rome, he carried a bunch of Parle Melody toffees as a gift for Italian Prime Minister Giorgia Meloni. And we don’t have to remind you what a viral moment that turned into. Melody toffees suddenly became a topic of global conversation and even started going out of stock on quick commerce shelves.

But the toffees becoming an internet sensation was only one part of the story. The other part was that ever since this moment went viral, the stock of a company called Parle Industries started soaring and even hit upper circuit for five straight days.

There was just one tiny problem.

Parle Industries has absolutely nothing to do with Melody toffees.

It’s actually an infrastructure and real estate company. And the real Parle — the one that makes Melody, isn’t even listed on the stock exchange.

But people mistook the namesake Parle Industries for the Melody maker and started piling into the stock. Maybe someone Googled “Parle stock”, saw that a company called Parle Industries was listed, didn’t bother checking what the company actually does (especially since Google wrongly shows the Parle logo when you search for “Parle Industries stock”), and blindly bought in. Then others simply followed the rally.

And that, folks, is pretty much what irrational exuberance looks like. This fancy term describes a situation where investors get so excited that asset prices rise far beyond what they’re actually worth. Or you could say, it’s when emotions start overtaking logic, often creating speculative bubbles that eventually burst.

Of course, buying a stock like Parle Industries without doing basic research is more about herd behaviour or, very bluntly, plain stupidity. But incidents like these can still fuel irrational exuberance.

Now, the phrase “irrational exuberance” became popular after economist Robert Shiller wrote a book by the same name in 2000, where he famously warned about the dot-com bubble. He later released a second edition in 2005, cautioning about the housing bubble that eventually led to the Global Financial Crisis. He later even won the 2013 Nobel Prize in Economics for his work on asset prices, but he was no magician predicting the future. He simply showed that if you want to understand financial markets, you first need to understand human behaviour.

But how do you, who may not be a Nobel Prize laureate, figure out if something is a bubble? And more importantly, how do you avoid getting swept up in it?

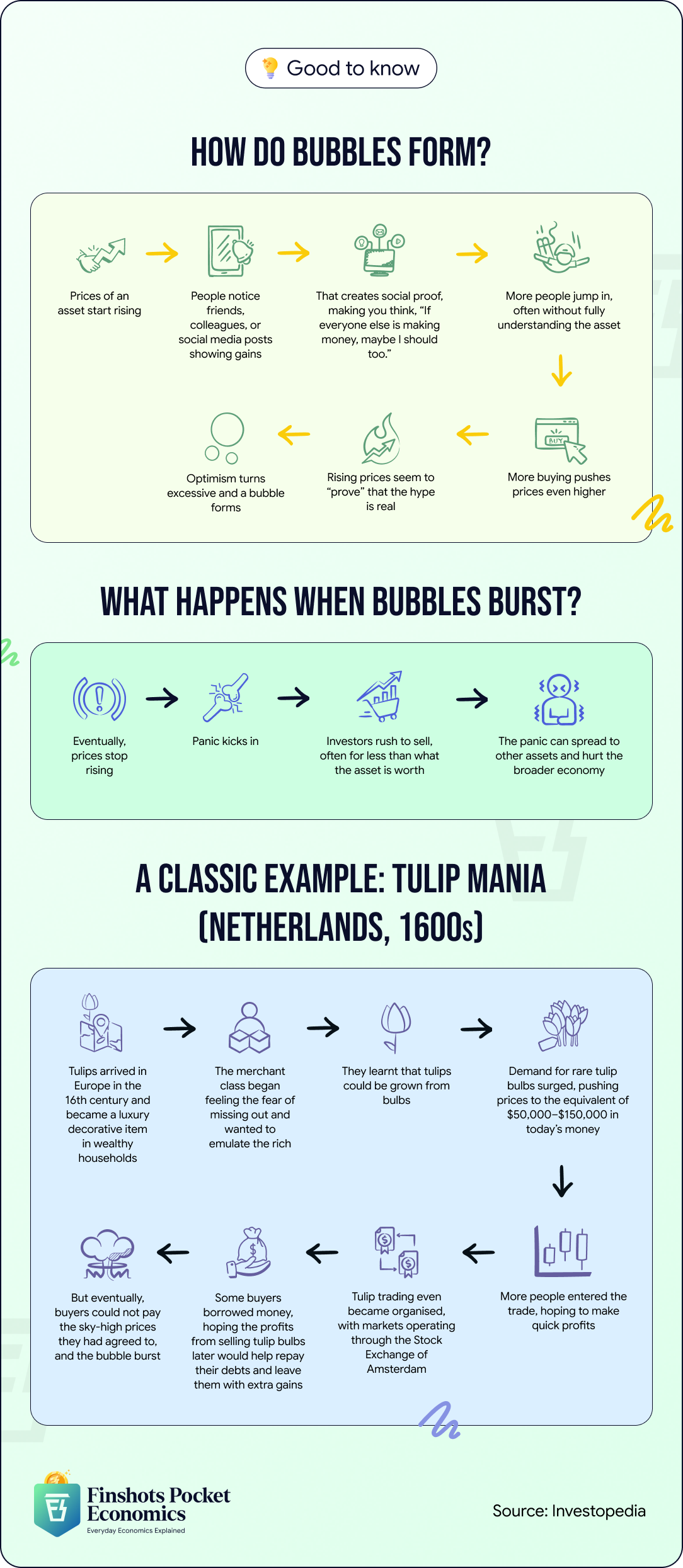

To understand that, you first need to get through a few boring but important basics. Like how bubbles form in the first place.

Yup, there’s a pattern. And historically, we’ve seen it play out in almost every financial bubble.

It usually begins with the price of an asset, or something linked to it, starting to rise. Think back to the 1990s when the internet became popular. Suddenly, every company with “dot-com” attached to its name seemed to have caught everyone’s fancy.

That makes you think, “If everyone’s making money, maybe I should try my luck too.”

This is where people often make their first mistake. You may not do your basic homework to understand the asset or ask whether it’s actually valuable. Instead, people start buying in, hoping prices will keep rising. Millions of others think the same way and pile in too.

Obviously, prices go up.

That makes you feel like you’re winning and making money. And to be fair, you might actually make some money, at least for a while. But that excitement and greed can trap everyone in a loop, pushing prices far beyond what the asset is fundamentally worth.

And beyond that point, you’re in bubble territory.

The problem is that bubbles only survive until something goes wrong. During the dot-com bubble, for instance, many unprofitable internet startups got listed on the bourses and rapidly burned through cash without generating much revenue. When funding eventually dried up, panic kicked in, stock valuations collapsed, and a massive wave of bankruptcies followed.

And now that you know the basics, let’s look at where situations like these actually show up in real life and how you can think clearly about them instead of simply joining the herd. Just to be clear, not all of them turn into financial bubbles because some can’t really be measured in money. But they’re definitely examples of real life irrational exuberance.

Okay, this isn’t a real term. It’s something I made up because, honestly, one of the most common bubbles we face in life is when we see others doing well. Or better still, when our parents see others doing well.

The best example is probably someone like me in their late twenties or early thirties. Once you hit that age, there’s suddenly pressure to get married, buy a car, buy a house, and have kids. But who really decides whether doing all these things are worth it?

Most of the time, at least in India (and I know many of you will agree) it’s either society or your own family. Of course, sometimes you can be the culprit too. You see your friends “settling” down and looking happy. And suddenly you start feeling FOMO (Fear of Missing Out). If they seem happy, you assume maybe you’ll be happy doing the same things too.

But there are a few ways to avoid blindly imitating Sharma ji ka ladka.

Firstly, and there’s no math for this one, it may be worth asking yourself if you actually want these things. Do you want to get married? Buy a house or a car? Have kids? Because sometimes we chase milestones simply because everyone around us seems to be doing the same.

But sometimes the answer can also be “yes”. You genuinely want these things and feel mentally and emotionally ready. The only question is whether you’re financially ready too.

Take weddings, for instance. It’s easy to get carried away seeing celebrities throw lavish destination weddings or friends posting dreamy pictures online. But weddings are also a one-time expense. So stretching your finances or taking on debt for something you won’t really earn back is probably worth thinking through.

But what about situations where you can potentially make your money back?

A good example is buying a house. Let’s say you live with your parents and feel like buying a house because your friends are doing it too. So you decide to take a home loan for a 2BHK in a neighbourhood that everyone claims will become the “next Bengaluru”.

You find an apartment worth ₹1 crore. The home loan costs 9.5% interest. “But no worries,” you think, “I’ll rent it out and use that money to pay off the loan.”

But pause for a second and look at the math.

That apartment rents for ₹30,000 a month. That’s ₹3.6 lakh a year. Which means the property generates a rental yield of just 3.6% annually (that’s the annual rent divided by the cost of the apartment), far lower than the 9.5% interest you’re paying on the home loan.

In simple words, you’re paying more to own the house than it earns. And any gains from the apartment’s rising value only really matter if you sell it (which, if it’s the only house you buy for yourself, you’re probably less likely to do).

But rising home prices can stop you from questioning the math. You could end up convincing yourself that if home prices rise further, you’ll miss your chance forever. And that’s usually how FOMO works. It nudges us into wanting what everyone else seems to have.

So yeah, comparing your home’s rental yield to your home loan interest rate is one small way to think a little more clearly before jumping in.

And if you want to dive deeper into this, we’ve already done a Finshots Money series in the past where we break down whether you should buy or rent a home, and the things worth thinking through before deciding to become parents.

Irrational exuberance doesn’t stop at the things we buy. Sometimes, it unknowingly creeps into our career decisions too.

A good example is deciding whether to take a high-paying, fast growing startup job or stay in your current role that has been around for years and pays reasonably well.

We’ve all seen this play out. A few people on LinkedIn announce that they quit their job to launch a startup. Someone else posts about landing a ₹40 lakh package. Another person claims their side hustle now earns more than their salary.

All of this can make staying where you are feel like a boring decision. And before you know it, you begin wondering if you should quit too, start something of your own, or worse, whether you’re somehow falling behind.

But what we rarely stop to think about is that you’re seeing outcomes, not probabilities. And social media is great at showing these outcomes, while ignoring the probabilities. Let’s explain.

For every founder announcing a fundraise, there are many startups quietly shut down. And that’s not us saying it (come on, Finshots and Ditto are startups too 🙂). Anand Mahindra once pointed out that 90% of Indian startups fail within the first five years. But let’s not debate the exact number. Let’s just assume, for the sake of optimism, that there’s a meaningful 50% chance that things may not work out.

Even after knowing this fact, our brains rarely compare ourselves to that silent majority. Rather, we compare ourselves to the loud exceptions. And that’s where irrational exuberance kicks in.

Let’s put this into an example. Suppose you earn ₹25 lakh a year today. A startup offers you ₹20 lakh in salary plus ₹10 lakh worth of equity after a few years. On paper, that sounds like ₹30 lakh.

But is it really ₹30 lakh?

Well, not exactly.

Because equity only matters if the startup survives and actually creates value.

So instead of looking at the most exciting outcome, it may help to think about probabilities.

Let’s say, very simply, you mentally cut the equity value (or any income that isn’t guaranteed) by 50% to account for the possibility that things may not go as planned. And when you do that, the ₹10 lakh equity starts looking more like ₹5 lakh in expected value.

So your startup offer becomes: ₹20 lakh salary + ₹5 lakh realistic equity value = roughly ₹25 lakh.

In other words, almost the same as what you earn today. Except one option is relatively predictable, while the other comes with a lot more uncertainty.

Of course, things could go brilliantly as well and that equity could be worth much more.

The point is not that startup jobs are bad. Sometimes, taking the bold bet can absolutely work. Or maybe you’re comfortable taking that risk because you have some financial backup and can afford a setback if things don’t work out.

It’s just that excitement isn’t a replacement for evaluation. And you can use this method for almost any career decision where the payoff looks promising but isn’t guaranteed. Things like starting your own business, turning a side hustle like content creation into a full-time career, or anything that feels exciting but doesn’t offer a stable, predictable income.

Because irrational exuberance begins when a compelling story starts feeling more convincing than the ground reality and the actual probabilities. And that’s probably not something you want to fall for without thinking things through practically, right?

There’s also a third, and probably the most common scenario: the behavioural trap of buying into stocks or fancy assets like crypto.

But we won’t get into that separately, simply because there’s no one clear way to evaluate whether a stock is worth buying or not.

That said, there is one simple thumb rule. If you don’t understand something, don’t rush into it. And if you still want to get into it, spend some time learning about it first.

That reminds us, we already have an entire series on crypto that you can check out here, before we see you again with another FPE edition next week.

Until then, tell us what you thought of today’s edition. Just hit reply to this email (or if you’re reading this on the web, drop us a message at morning@finshots.in).

Or even better, share it with your friends and family on WhatsApp, LinkedIn, and X.

Finshots Weekly Quiz v2.0 🧠

As you probably already know, the Finshots Weekly Quiz has a new avatar. If you missed out on it in the last couple of months, don’t worry. Click here to check out the rules and set a reminder to participate consistently starting next month!

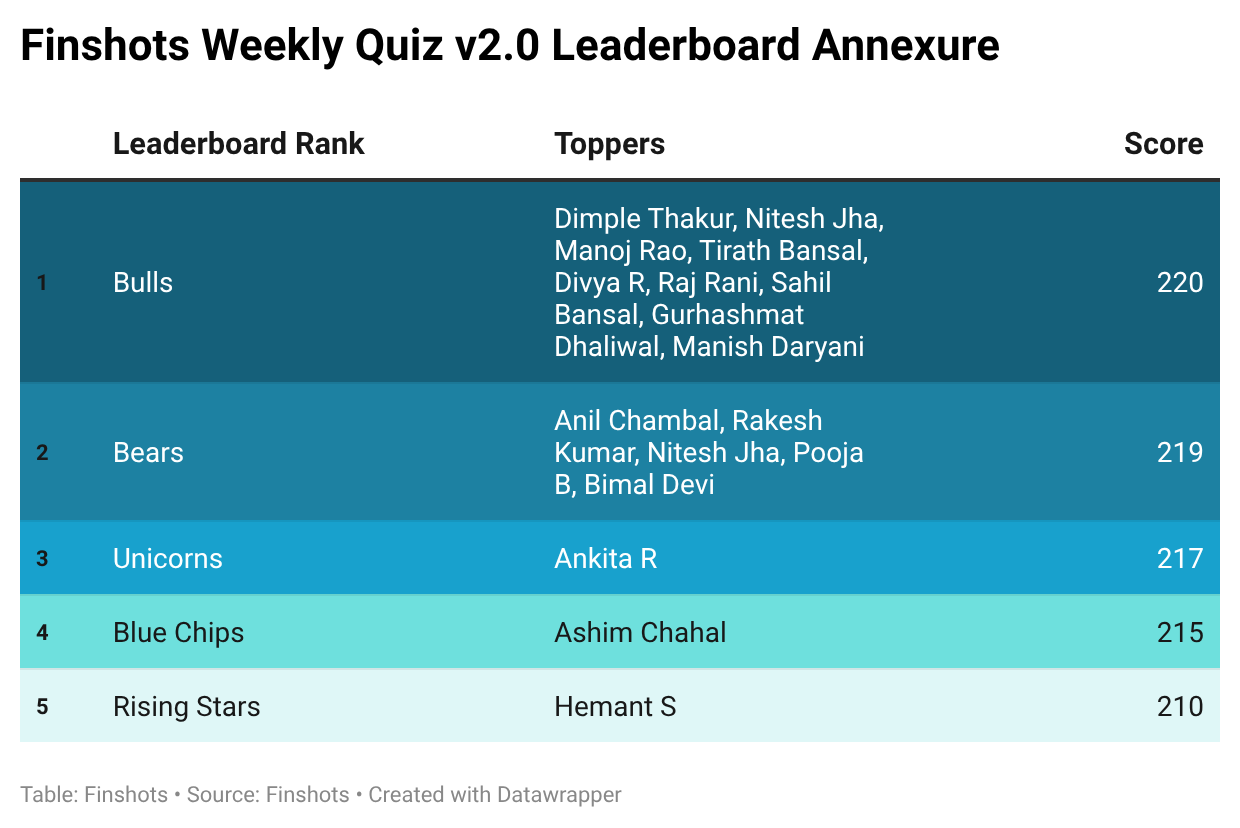

Next, let’s move on to the top scorers from our previous weekly quiz. There were a whole bunch of you who participated, and many of you ended up with the same scores. So we’re calling you Bulls, Bears, Unicorns, Blue Chips, and Rising Stars. Here’s how the leaderboard looks right now:

If your name has been featured on the leaderboard, then congratulations! If not, don’t lose hope. If you attempted last week’s quiz, keep at it and answer all the weekly quizzes this month. You never know when the turntables! Click on this link to take this week’s quiz, which is open till 12 noon, Friday, 5th of June, 2026. The more answers you get right, the better your chances of appearing on the Finshots Weekly Quiz leaderboard. We’ll publish it every Saturday in this edition. And the winner will be announced in the first week of June.