Can you trade rainfall?

In today’s Finshots, we talk about a different kind of futures contract whose underlying asset is rainfall.

Before we begin, if you're someone who loves to keep tabs on what's happening in the world of business and finance, then hit subscribe if you haven't already. We strip stories off the jargon and deliver crisp financial insights straight to your inbox. Just one mail every morning. Promise!

If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

For most of human history, the weather was treated as an uncontrollable force of nature.

A drought could destroy economies. Floods could paralyse cities. And businesses simply absorbed the damage as part of life. An “Act of God’, if you will.

But financial markets have a habit of trying to price every form of uncertainty eventually. Interest rates became tradeable. Oil futures became tradeable. And then volatility itself became tradeable.

Weather followed surprisingly soon after. And one of the biggest pioneers of this was Enron (Yes, that Enron). Their logic was simple. If weather could materially affect revenues, then weather uncertainty could also be bought, sold, and hedged.

Soon, traders were creating contracts linked to wind, snowfall, and temperature patterns.

And now, the National Commodity & Derivatives Exchange (NCDEX) in India may soon attempt something even stranger: trading rainfall.

For context, the NCDEX is preparing to launch derivative contracts linked to Mumbai’s rainfall patterns. In simple terms, businesses and traders may soon be able to hedge against rain the same way they already hedge against oil prices or currencies.

Sidebar: A derivative is basically a financial contract whose value depends on something else like gold prices, stock prices, currencies, or even rainfall. For example, imagine you and your friend make a deal based on gold prices. You say, “If gold prices go up this month, you pay me ₹1,000. If they fall, I’ll pay you ₹1,000.” So, the contract simply depends on what happens to gold prices, without you actually buying or selling gold.

At first glance, this sounds bizarre. After all, how exactly do you “trade” rain, right?

NCDEX has come up with an answer. The proposed derivative contract, called RAINMUMBAI, uses Mumbai’s historical Long Period Average (LPA) rainfall or historical average rainfall as its reference point. Based on past weather data, the exchange estimates that a normal monsoon in Mumbai usually brings about 2206.7 millimetres of rainfall. So now, during the monsoon, actual daily rainfall is compared with this average. If Mumbai gets more rain than usual, the difference is counted as a positive number. If it gets less rain than usual, the difference turns negative.

Let’s think about why it makes sense. A weak monsoon affects agriculture, excessive rainfall floods cities, and heatwaves increase electricity demand.

So, in other words, the weather directly affects a company’s revenues, people’s productivity, and even demand across sectors. And in a country like India, where over 46% of the workforce is employed in agriculture, rainfall itself becomes an economic variable worth managing.

That is precisely what weather derivatives attempt to do.

And the appeal is quite obvious. Over the last 30 years, India has lost around $180 billion due to extreme weather. So a financial hedge offers businesses at least some cushion against these uncertainties.

But this is also where the idea starts becoming much more complicated than it initially appears.

The first challenge is that rainfall is hyperlocal. Even city-wide rainfall numbers do not always reflect what people actually experience on the ground. Anyone who has lived in cities like Mumbai or Chennai already understands this intuitively. One neighbourhood can be completely submerged under water while another receives barely enough rainfall to cause inconvenience.

And that creates a problem for financial contracts like these. For a derivative to work properly, the underlying variable must closely match the real-world risk being hedged. But a company operating across India may not gain much protection from a Mumbai-specific rainfall contract.

This is known as “basis risk” or the risk that the payout from the derivative does not perfectly match the actual losses (from the underlying asset) experienced in the real world.

Which is why the real underlying asset here is not just rainfall itself, but trust in the measurement system. Because the entire contract only works if participants believe the weather data is objective, standardised, and impossible to manipulate.

Then comes the second concern: speculation.

Because financial markets rarely remain limited to genuine hedgers. The moment a market becomes liquid enough, traders with no direct exposure to the underlying risk begin participating simply to profit from price movements. That means rainfall contracts could eventually attract speculators who are effectively betting on weather outcomes without having any real business exposure to rainfall risk itself.

In fact, this concern has existed almost since the birth of weather derivatives themselves. However, Enron’s later collapse left the market with a lasting stigma. And people began questioning whether trading weather was genuine risk management or simply another sophisticated form of gambling disguised as finance.

Now, to be fair, speculation itself is not inherently bad. Most derivatives markets depend on speculators to provide liquidity and make trading easier for genuine hedgers. But the concern is what happens if speculative activity eventually comes to dominate the market itself. At that point, prices may begin reflecting trading sentiment rather than actual hedging demand.

And this could slowly transform climate volatility into another “casino-style” financial market detached from the real economy. To some extent, that concern is valid. Financial markets are extremely efficient at pricing measurable risks, but climate systems are not always easily predictable. Extreme weather events often create cascading second-order effects that are difficult to model. Flooding in one city can affect supply chains elsewhere, or crop failures can alter food inflation months later. So, in other words, climate risk is not always neat enough to fit inside a financial model. And that creates a deeper philosophical tension around products like these.

Which makes you ask, should climate risk become a tradable asset class at all?

Some would argue that financialising weather risks distracts from solving the underlying problems themselves. After all, a booming market for climate hedges is not necessarily proof of climate resilience. Similarly, rainfall derivatives do not prevent floods or improve drainage systems. At best, they redistribute the financial losses after damage has already occurred.

And that perhaps captures the deeper limitation of financial solutions to climate problems. They cannot replace real-world adaptation. Better drainage systems, flood-control infrastructure, and climate-resilient agriculture still matter far more to ordinary people than financial hedges ever will.

Because in reality, the first beneficiaries of products like these will likely be insurers, utilities, and large financial institutions with the resources to actively manage climate risk. Meanwhile, farmers, informal workers, and vulnerable households may continue to absorb the direct physical consequences of floods, droughts, and extreme heat.

This creates an uncomfortable tension that financial markets are becoming increasingly sophisticated at pricing climate risk precisely because the physical world itself is becoming more unstable.

But then again, that is also how insurance has historically worked, and it’s not necessarily a bad thing. For instance, life insurance does not prevent death. What it does instead is create a mechanism that allows a family to maintain the same quality of life despite the loss.

And perhaps that is exactly what is happening here, too.

As climate volatility intensifies globally, businesses can no longer treat weather as a background variable. It directly influences revenues, costs, logistics, and economic stability itself.

Financial markets are therefore doing what they have always done when uncertainty becomes economically meaningful: attempting to quantify it, price it, and mitigate that risk.

Which is why the launch of rainfall derivatives in India is not really about “trading rain”.

It signifies that climate change is slowly evolving from just an environmental problem into a financial one. The markets are merely responding to that by building new systems around that reality.

Until next time...

If you liked this story on how the financial markets are treating weather uncertainty, feel free to share this with your friends, family or even strangers on WhatsApp, LinkedIn or X.

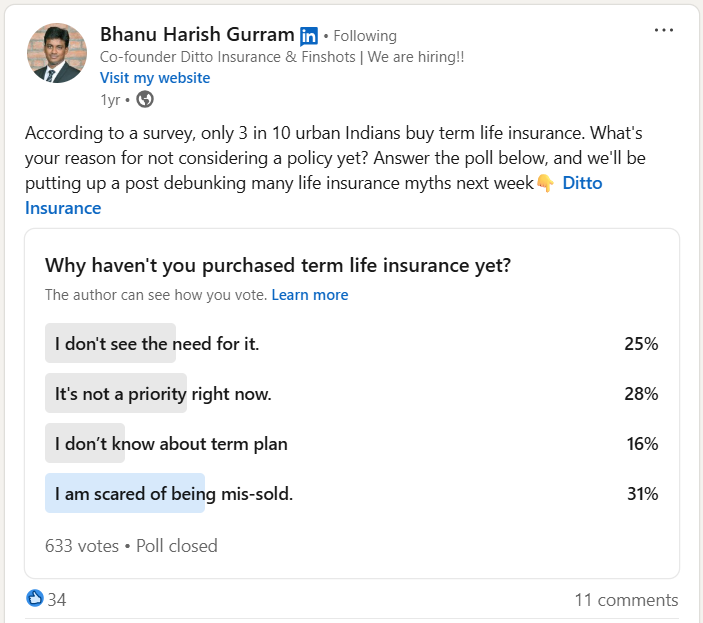

Our co-founder asked people why they avoid Term Insurance. The top reason? Right here. 👇🏽

31% said their biggest fear is being mis-sold. Many worry that agents may push costly plans or add confusing extras without full transparency.

That's a valid concern. After all, how can you trust something you don’t completely understand?

That’s why Ditto, a product of Finshots, has pioneered India’s #1 Spam-Free insurance platform. Our IRDAI-Certified advisors offer honest advice and help you find the right plan. Book a FREE consultation today.