And then there were two: The NSE IPO

In today’s Finshots, we break down the business behind the long-awaited NSE IPO.

But here’s a quick sidenote before we begin. We’re looking for a business writer to join Finshots’ newsletter team. If you’re someone who can tell compelling stories and explain financial concepts in plain English without drowning readers in jargon, do consider applying through the link here. Or share this with someone who might be a good fit for the role.

Now onto today’s story.

The Story

After years of delays, regulatory scrutiny and legal hurdles, the National Stock Exchange (NSE) has filed its Draft Red Herring Prospectus (DRHP), bringing one of India's most anticipated IPOs a step closer to reality.

And on the face of it, the excitement is understandable.

NSE sits at the centre of India's financial system. It dominates trading volumes across equities and derivatives, benefits from powerful network effects and generates the kind of profitability most companies can only dream of.

Every time you place an order through a broker like Zerodha* or Groww, that order is routed to an exchange, typically NSE or BSE. The exchange charges a tiny fee for providing the marketplace where buyers and sellers meet.

Individually, those fees are almost negligible. But when billions of trades flow through the platform every year, they add up very quickly.

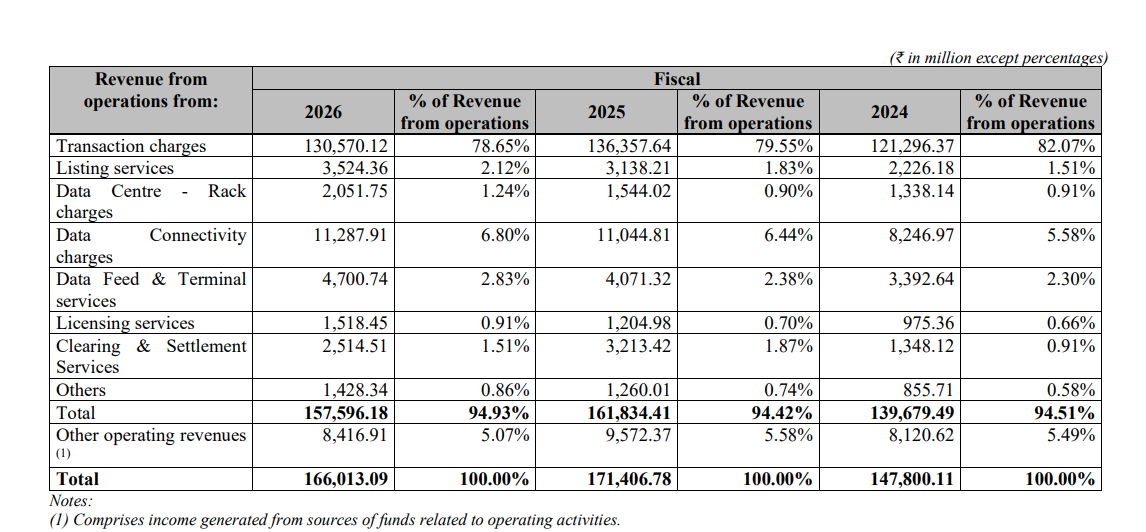

That's why transaction charges remain the lifeblood of NSE's business.

In FY26, NSE earned over ₹16,600 crore from operations. Nearly ₹13,057 crore of that came from transaction charges. In other words, every time trading activity rises, NSE gets a small cut.

NSE had a 92.99% share of India’s cash market by turnover in FY26. In equity futures, its share was 99.79% and in equity options, it was 74.71% by premium turnover.

To appreciate how dominant that is, consider BSE.

BSE may be India's oldest exchange and the only listed one today, but when it comes to trading activity, NSE operates in a different league altogether. In several segments, particularly derivatives, it has become the default venue for traders, institutions and market makers.

And that matters because liquidity attracts liquidity. Traders naturally gravitate towards the exchange where everyone else is already trading. The result is a powerful network effect that becomes increasingly difficult for competitors to break.

This is why exchanges can become exceptional businesses. They don't take credit risk like banks or need factories and warehouses. Once the infrastructure is built, every additional trade can be highly profitable.

That shows up in the numbers. NSE’s normalised operating EBITDA margin stood at 76.23% in FY26. Its profit for the year was ₹10,302 crore. There are very few large companies in India that can convert revenue into profit at that scale.

Which raises an interesting question.

If NSE is such an extraordinary business, why has it taken so long to list?

That's because the exchange isn't simply a venue where buyers and sellers meet anymore. Over three decades, it has evolved into one of India's most important market institutions.

In fact, transaction charges still account for nearly 79% of NSE's operating revenue. But the exchange also earns from listing fees, data products, Nifty licensing, clearing services and colocation facilities. In short, as India's markets grow, NSE finds more ways to monetise them.

The most important shadow over NSE’s listing has been the co-location matter. Co-location allows trading firms to place servers close to the exchange's systems to execute trades faster, a common practice among high-frequency traders.

But in NSE’s case, allegations arose around preferential access to tick-by-tick data and the exchange’s co-location. SEBI issued show cause notices in 2017 and 2018. In April 2019, SEBI passed orders too. Among other things, it also directed NSE to disgorge amounts and barred it from accessing the securities market for six months.

The financial impact is visible in its books. NSE’s other expenses in FY26 included SEBI settlement fees of ₹1,431.6 crore, more than double the ₹670.2 crore in FY25.

Its biggest strength though, is its dominance. But that same dominance also attracts scrutiny. The larger and more important the exchange becomes, the more closely regulators watch the products it offers, the fees it charges and the way it operates.

That matters for investors. Because when you buy NSE, you are not just buying a high-margin business. You are also buying into a business whose future is closely tied to regulation.

SEBI can influence the products that exchanges offer, the charges they levy, the risks they must manage and the way derivatives trading grows. The DRHP itself points to this clearly. In FY26, NSE’s transaction-charge revenue fell 4.24%, partly because of lower trading volumes across cash market, equity futures and equity options. The company links this to regulatory changes.

This is important because derivatives, especially options, are central to NSE’s business model. Options alone contributed 60.2% of NSE’s revenue from operations in FY26. If regulators continue to tighten rules around weekly expiries, contract sizes, margins or retail participation, NSE’s biggest revenue engine could feel the impact.

And we've already seen how regulatory changes can alter the competitive landscape.

Take BSE, for instance. While it remains a fraction of NSE's size, FY26 turned out to be a tale of two exchanges. NSE's profit fell 15% year-on-year to ₹10,302 crore, partly due to tighter derivatives regulations. BSE, meanwhile, reported an 88% jump in profit to ₹2,487 crore.

A big reason was derivatives. When SEBI restricted exchanges to a single weekly expiry per index, the change affected NSE more than BSE because NSE had built a much larger business around multiple weekly expiries. At the same time, BSE benefitted from the relaunch and restructuring of its SENSEX and BANKEX contracts.

NSE remains the dominant exchange by a considerable margin. But the episode is a useful reminder that even market leaders are not immune to regulatory shifts.

That does not make NSE a weak business. It simply means it is a regulated monopoly-like business, not an unregulated one.

And that brings us to the IPO itself.

This is a pure offer-for-sale. Existing shareholders are selling up to 14.89 crore shares, meaning NSE itself will not receive any proceeds. The listing is essentially a liquidity event for existing investors and an entry point for new ones.

Some of the sellers are among India’s biggest financial institutions. State Bank of India is offering up to 2.475 crore shares. Bank of Baroda, Stock Holding Corporation of India, General Insurance Corporation of India, New India Assurance and others are also selling. Foreign investors such as Canada Pension Plan Investment Board and Aranda Investments are part of the selling shareholder list too.

The offer represents roughly 6% of NSE’s post-offer equity share capital. The final price band and issue size are yet to be announced.

Interestingly, NSE's shares won't trade on NSE itself. Since exchanges cannot list on their own platforms, the company's stock is expected to trade on BSE, its much smaller rival.

So what are ordinary investors really being offered?

Investors are being offered a company whose best qualities come with constraints. Its dominance invites scrutiny. Its public role limits how freely it can behave like a normal private company. And its biggest revenue stream depends on trading activity that regulators may want to cool if speculation becomes excessive.

That is the trade-off.

NSE is not a flashy consumer company. It does not need to persuade people to buy a new product every month or chase customers with discounts. It sits at the centre of a market that millions of Indians now use almost daily.

If India’s financialisation story continues, NSE is one of the clearest businesses to benefit from it.

That's what makes the NSE IPO so unusual.

Investors aren't just buying one of India's most profitable businesses. They're buying one of India's most important financial institutions.

And while the business benefits enormously from India's growing capital markets, it operates under rules that can change at any time.

In that sense, NSE is both a beneficiary of regulation and a prisoner of it.

Which means investors aren't just buying the tollbooth. They're buying the tollbooth on a road where the regulator decides the speed limit.

Until next time….

*Zerodha, through its fund Rainmatter, is an investor in Finshots.

If you like stories that make business and finance actually make sense, then hit subscribe by clicking here. If you’re already a subscriber (or reading this on the app), thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet via WhatsApp, LinkedIn, and X.

The smart way to stay secure

This week we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday (tomorrow), 20th June at 11:30 AM: Life Insurance How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 21st June at 11:30 AM: Health Insurance How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.