Why is India giving foreign investors a tax break?

In today’s Finshots, we explain why the government is changing bond tax rules for foreign investors.

But here’s a quick sidenote before we begin. We’re looking for a business writer to join Finshots’ newsletter team. If you’re someone who can tell compelling stories and explain financial concepts in plain English without drowning readers in jargon, do consider applying through the link here. Or share this with someone who might be a good fit for the role.

With that out of the way, let’s dive into today’s story.

The Story

Every year, the government needs to borrow trillions of rupees, be it for infrastructure, skill development, or any number of government initiatives.

And one way to do that is to issue government securities or G-Secs. Think of them as IOUs. You lend money to the government today, and in return, it promises to pay you interest and repay you the principal later at a predetermined date.

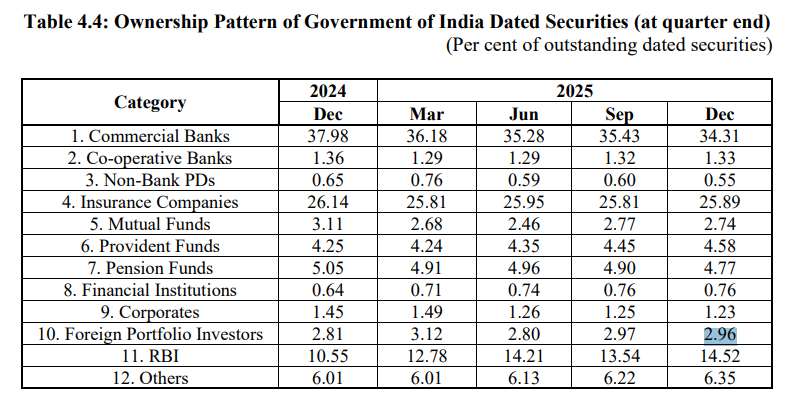

Mostly banks, insurance companies, and pension funds buy them, apart from retail investors.

And over the years, India has tried to make our domestic bond market more attractive to foreign investors, too. They did this through something called the FAR or ‘Fully Accessible Route’.

This was introduced back in 2020, and it basically allows foreigners to invest in certain government bonds without restrictions.

Before FAR, foreign portfolio investors (FPIs) could only buy government securities up to specified quotas. Once those limits were exhausted, no additional foreign investment was allowed. FAR changed this by designating certain Government of India securities as FAR-eligible bonds, which eligible non-resident investors can purchase without any cap.

And this move paid off.

Since then, India has steadily opened up its bond market and secured inclusion in some of the world's biggest bond indices, including JPMorgan's Emerging Market Bond Index and FTSE Russell's Emerging Markets Government Bond Index.

Now, a few years later, the government has announced tax exemptions for foreign investors on interest income and capital gains in eligible government bonds. Which makes you ask, “Why would India willingly give up tax revenue by exempting foreign investors from taxes?”

Well, the answer is that India is trying to solve multiple problems at the same time.

The most immediate one is participation.

See, despite years of reforms, foreign portfolio investors own just 2.96% of India's government securities.

The reason is simple. Foreign bond investors have options. And lots of them. Whether it’s a pension fund sitting in Canada, an insurance firm in Japan or an asset management company in Europe, they aren’t just picking Indian bonds over nothing.

They constantly have to choose among Indian G-secs, US Treasuries, Japanese government bonds, German Bunds, and dozens of other debt instruments worldwide.

So when they’re comparing options, they’re not only looking at the returns. They also ask themselves the following questions:

- How easy is it to invest?

- How easily can money move in and out of the country?

- How tricky are the tax rules?

- How liquid is the market?

- And how much paperwork is involved?

In other words, the challenge is no longer convincing investors that India is worth investing in. India, being one of the world's fastest-growing major economies, has already done that.

Rather, the challenge is to convince them that India is an easy place to invest.

Besides, commercial banks, insurance companies, and the RBI collectively hold close to 75% of all government securities. By removing taxes on interest income and capital gains, India hopes to make its bonds more competitive with alternatives such as US Treasuries and Japanese government bonds.

India has already seen a glimpse of what that can look like.

When Indian government bonds entered JPMorgan's Emerging Market Bond Index in June 2024, analysts estimated that the inclusion could bring in another $30 billion of inflows as India's weight in the index increased.

Plus, more participation can have an underrated side effect. The Indian government borrows trillions of rupees every year. And like any borrower, it benefits when more lenders are willing to show up.

A larger pool of investors can make the bond market deeper and more liquid. And if enough investors compete to buy government bonds, borrowing costs could eventually come down as well.

But another very interesting reason for these tax breaks is India’s long-running pursuit of inclusion in the Bloomberg Global Aggregate Index.

Think of it like this. When a company is included in the Nifty50 Index, billions of rupees from index-tracking funds start flowing into its stock. Similarly, when a country gets included in the Bloomberg Global Aggregate Index, it can suddenly find itself on the radar of a much larger pool of global capital.

In a way, index inclusion acts like a distribution network. Without it, India has to convince thousands of investors individually that its bonds are worth buying. But with it, India's bonds automatically become visible to funds that track or benchmark themselves against the index.

Reports suggest that being included in the index could add up to $25 billion in inflows to the bond market. That's why countries spend years trying to qualify.

And that's also why India has been steadily removing barriers that foreign investors have complained about. However, despite years of reforms, India is still not part of the index.

In fact, Bloomberg reviewed India's case in January this year and decided to postpone a decision, saying it wanted more time to evaluate operational and market-access issues. It promised to revisit the matter in the second half of 2026.

And now, with the second half of 2026 fast approaching, India had to strengthen its case. So the timing of the move may not be accidental either.

With oil prices rising and the rupee under pressure, attracting foreign money into government bonds could bring additional capital into the country. And because many bond investors are long-term institutions such as pension funds and insurers, those inflows could be more stable than equity.

That said, a tax break alone may not be enough. Foreign investors don't earn returns in rupees. They ultimately measure their gains in dollars, euros or yen. Which means currency movements matter.

Even if an investor earns an attractive return on an Indian government bond, a weakening rupee can eat into those gains once the money is converted back into their home currency.

That's one reason why many global investors favour markets such as the United States. US Treasuries may offer lower yields than some emerging-market bonds, but they come with the backing of the US dollar and one of the deepest financial markets on the planet.

So while the tax break removes one hurdle, it doesn't eliminate every concern investors may have.

Seen this way, the tax break doesn't look like an isolated giveaway. It looks like the latest step in a strategy that has been unfolding for years.

The bigger question is whether that will be enough and whether global investors will walk through it.

Until next time…

If this story helped you understand why the government is giving tax breaks to foreign investors, share it with a friend, family member or even strangers on WhatsApp, LinkedIn and X.

🚨 ATTENTION: FINSHOTS FAMILY

This week we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Friday, 19th June at 6:30 PM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Saturday, 20th June at 10:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.