What are capital controls anyway?

In today’s Finshots, we explain why governments keep interfering with money flows and the impossible balancing act sitting behind every modern currency.

Before we begin, if you're someone who loves to keep tabs on what's happening in the world of business and finance, then hit subscribe if you haven't already. We strip stories off the jargon and deliver crisp financial insights straight to your inbox. Just one mail every morning. Promise!

If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

Last week, Prime Minister Narendra Modi laid out a seven-point framework aimed at strengthening India’s economic resilience in an increasingly uncertain world. The speech touched on growth, supply chains, domestic capability, and financial stability. But underneath many of those themes sat one idea that shapes almost every modern economy: control over how money flows.

Because in today’s financial system, currencies are no longer influenced just by exports, imports, or domestic economic growth. They are constantly being pulled around by global capital moving across borders in search of higher returns, lower risk, or safer assets.

And that creates a difficult problem for governments.

Because a weakening currency does not just make foreign vacations expensive. It can raise the cost of imports, increase inflation, make foreign debt harder to repay, and destabilise financial markets. For countries that rely heavily on imported energy, such as India, currency weakness can ripple through the economy very quickly.

This is why central banks and governments spend so much time trying to influence their currencies.

Broadly speaking, they have three major levers.

The first is interest rates. Higher interest rates make a country more attractive to investors because they can earn better returns on bonds and deposits. And if enough foreign money flows in, demand for the local currency rises, which can support its value.

The second lever is foreign exchange reserves. Central banks can directly buy or sell currencies in the market using their reserves. If a currency weakens too rapidly, the central bank can sell dollars from its reserves and buy the local currency to stabilise it.

And the third lever is capital controls.

Capital controls are rules that regulate how money enters or leaves an economy. These restrictions can take many forms. Governments may limit how much money residents can move abroad, restrict foreign ownership in certain sectors, impose taxes on foreign outflows, or create approval systems for large capital transfers.

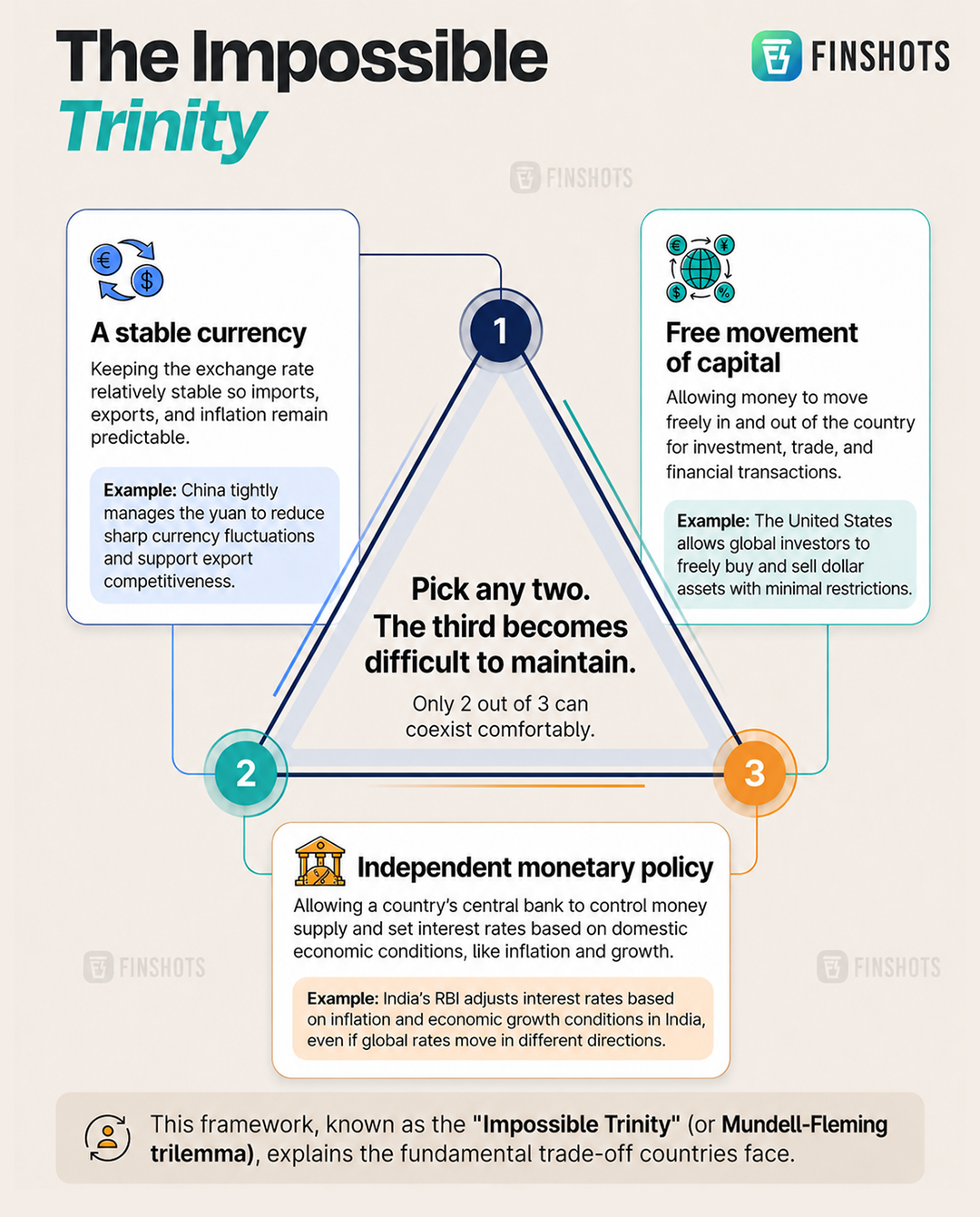

At first glance, these rules can seem unnecessarily restrictive. But once you understand how quickly global money moves, the logic becomes clearer. This is where economics introduces one of its most famous trade-offs: the “Impossible Trinity” or the Mundell-Fleming Trilemma.

The idea is surprisingly simple. A country can only fully achieve two out of three goals at the same time:

You can either have a stable currency, free movement of capital, or an independent monetary policy.

Trying to maintain all three simultaneously usually does not work. And the reason this trade-off exists comes down to something surprisingly simple: arbitrage.

Imagine a country fixes its currency while also allowing money to move freely across borders. Now, suppose the central bank suddenly raises interest rates well above global levels. Investors around the world would immediately move money into that country to capture higher returns.

That creates massive demand for the local currency, pushing it upward. But because the government is trying to maintain a fixed exchange rate, the central bank is forced to intervene constantly by printing more local currency and buying foreign assets to hold the currency peg in place.

Over time, this becomes extremely difficult to sustain. Foreign exchange reserves get stretched, financial imbalances build up, and eventually markets begin questioning whether the fixed exchange rate can survive at all.

This is why economists Robert Mundell and Marcus Fleming argued in the 1960s that countries cannot simultaneously maintain free capital movement, a fixed exchange rate, and an independent monetary policy at the same time.

Take China, for example.

China prefers maintaining significant control over its currency while also preserving an independent monetary policy. To do that, it imposes strict capital controls. Money cannot move freely in and out of the country without oversight. That gives Chinese authorities more room to manage interest rates and currency stability internally.

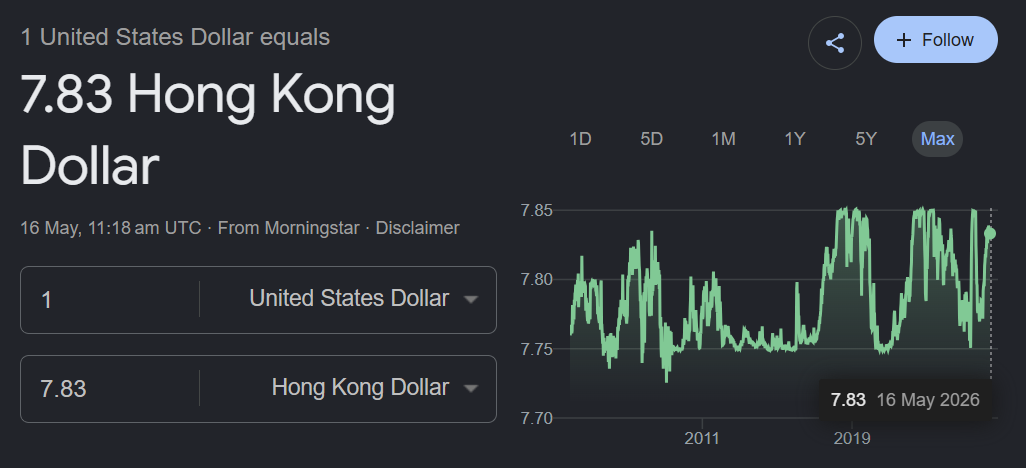

Hong Kong represents an even more extreme version of this trade-off.

To maintain its status as one of the world’s freest financial hubs, Hong Kong chose almost completely free capital movement while tightly pegging its currency to the US dollar. But that came with a major sacrifice: it effectively gave up independent monetary policy.

In practice, this means Hong Kong’s interest rates often move in line with the US Federal Reserve, even if local economic conditions look completely different. The city retains currency stability and open capital markets, but loses flexibility over domestic monetary decisions.

Now compare that with the US.

The US allows capital to move almost completely freely and maintains an independent monetary policy through the Federal Reserve. But the trade-off is that the dollar fluctuates openly in global markets.

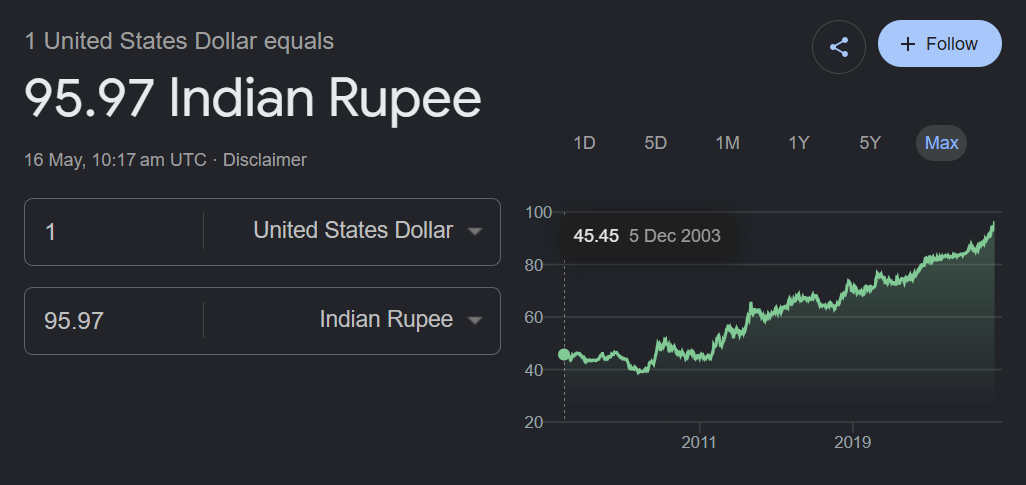

India sits somewhere in between.

The country allows substantial foreign investment and relatively open capital flows, but it still intervenes heavily in currency markets and maintains selective restrictions where needed. The Reserve Bank of India actively uses forex reserves to smooth volatility, while policies like the Liberalised Remittance Scheme place structured limits on how much money residents can move abroad annually.

This balancing act exists because global capital is incredibly fast and highly sensitive to interest rates and risk.

Imagine the US Fed suddenly raises interest rates sharply. Investors around the world may decide that dollar assets now look safer and more attractive. Money begins flowing out of emerging markets and back into the US.

When that happens, countries like India can experience pressure on their currencies. The rupee weakens, imported inflation rises, and domestic policymakers face difficult choices. Raising Indian interest rates too aggressively could slow growth. Failing to raise them could worsen currency pressure.

And entire economies have collapsed under this kind of stress.

One of the clearest examples came during the Asian Financial Crisis of 1997.

Several Southeast Asian economies tried to maintain relatively stable exchange rates while also keeping capital flows open and pursuing domestic monetary priorities. For a while, the system appeared stable. Foreign capital flowed in aggressively, asset prices surged, and growth looked unstoppable.

But once investor confidence weakened, money exited just as quickly as it had entered. Central banks burned through foreign exchange reserves trying to defend their currencies, speculative attacks intensified, and several economies experienced devastating currency collapses within months.

Argentina faced a different version of the same problem in the early 2000s. The country had pegged its currency tightly to the US dollar while allowing free capital flows. Over time, large parts of the economy became dependent on dollar-denominated debt. When the peg eventually broke, the peso collapsed, debt burdens exploded, and the financial system spiralled into crisis.

This is why capital controls are not simply bureaucratic obstacles designed to frustrate investors. They function as economic shock absorbers.

So, by slowing or regulating capital movement, governments gain some breathing room during periods of financial stress. They may not stop crises entirely, but they can reduce the speed and severity of capital flight.

Of course, there are trade-offs here too.

Excessively strict capital controls can discourage foreign investment, reduce financial market depth, and make economies less attractive globally. Investors generally prefer environments where money can move freely. Too many restrictions can create inefficiencies and reduce confidence.

But fully open capital accounts come with their own risks, especially for developing economies that remain vulnerable to volatile external shocks.

That is why most countries end up somewhere in the middle rather than at either extreme.

And perhaps that is the deeper reality behind currency management today.

In fact, some economists now argue that the “Impossible Trinity” may no longer even be a trinity. Economist Hélène Rey from London Business School has argued that in a world dominated by massive global capital flows, floating exchange rates alone may no longer protect countries from external financial shocks.

According to this view, global liquidity cycles driven by institutions such as the US Fed have become so powerful that countries effectively lose monetary independence unless they actively regulate capital flows in some form.

In other words, even countries with floating currencies may not be as economically independent as they appear.

So there you have it, folks. No country truly has complete control over its currency anymore (unless you’re North Korea 🤷). Global finance is too interconnected for that. Every economy is constantly making compromises between stability, openness, and policy independence.

Some prioritise investor freedom. Others prioritise monetary sovereignty. Most, including India, attempt to navigate an uncomfortable middle ground where capital remains relatively open, but the state still retains tools to intervene when needed.

Which is precisely what makes currency management so difficult. There is no perfect formula. Only different ways of managing an impossible balancing act.

Until next time…

If you liked this story on capital flows and the hidden trade-offs behind economic policy, share it with your friends, family or even strangers on WhatsApp, LinkedIn, and X.

Message to all the Breadwinners

You work hard, you provide, and make sacrifices so your family can live comfortably. But imagine when you're not around. Would your family be okay financially? That’s the peace of mind term insurance brings. If you want to learn more, book a FREE consultation with a Ditto advisor today.