Rajesh Exports' House of Cards?

In today’s Finshots, we break down what SEBI believes may have gone wrong at Rajesh Exports.

The Story

If you’ve ever looked at Rajesh Exports’ stock chart, there’s a good chance you would have walked away confused. Especially if you didn’t know much about the company.

Because despite going public way back in 1995, the stock only seems to have started attracting serious investor attention over the last decade or so. And in that time, the company has seen some dizzying highs and brutal lows.

Just to give you some context, in 2022, Rajesh Exports comfortably sat in the large-cap bucket, with a market cap of over ₹20,000 crore. Then for the next three years, until 2025, it slipped into mid-cap territory (valued between ₹5,000 crore and ₹20,000 crore) Since January this year, however, it has entered the small-cap zone, with a market cap below ₹5,000 crore.

And as it turns out, this dramatic fall wasn’t random. It forms the backdrop to what could become one of the biggest accounting fraud investigations in Indian corporate history.

For the uninitiated, Rajesh Exports Limited (REL) is a company that describes itself as a gold refiner and jewellery manufacturer. Recently, market regulator SEBI issued a sweeping interim order against the company in a case involving what appears to be massive financial misrepresentation.

And we’re not talking about small numbers here. According to SEBI’s interim order findings, REL may have allegedly misrepresented close to a staggering ₹15 lakh crore in revenues over the last five years. Unsurprisingly, the market didn’t take kindly to the allegations and the stock tanked.

But here’s the interesting bit. This investigation didn’t begin with some whistleblower inside the company.

Like many corporate scandals, it started with something ordinary. Back in 2024, a shareholder wrote to SEBI claiming something felt off about REL’s books. Specifically, there were huge sums of money that customers supposedly owed the company, but those dues had remained unpaid for over two years.

That was enough to put REL on SEBI’s radar. Naturally, the regulator launched a formal investigation and started with the obvious first step — asking for financial records.

But even before investigators could begin digging, they hit a wall. REL, according to SEBI, refused to fully cooperate.

At one point, the company reportedly argued that Swiss privacy laws prevented it from sharing records related to its foreign subsidiaries. But when SEBI examined those laws, it found the argument to be shaky at best. Swiss privacy protections, it noted, mainly apply to individuals, not corporations. And even where they do apply, exceptions exist for regulatory investigations.

With that out of the way, forensic auditors picked a sample of purchase transactions and asked REL for supporting documents. The company managed to provide complete documentation for just 2% of what was requested.

Yup, 2%.

When auditors moved to sales transactions, things weren’t much better. Only around 35% had proper documentation. The rest, amounting to lakhs of crores of rupees, allegedly had little or no backing.

And this is where the numbers start becoming hard to ignore. REL had presented itself as a giant global business with enormous consolidated revenues. In FY26 alone, it reported consolidated revenues of roughly ₹7.6 lakh crore. Between FY21 and FY25 (the period of investigation), annual revenues ranged between ₹2.5 lakh crore and ₹4.2 lakh crore.

But there was one problem. REL’s own India business was actually tiny in comparison. In FY25, for example, REL India generated only about ₹7,000 crore in standalone revenue. Which means roughly 98–99% of total revenues supposedly came from foreign subsidiaries.

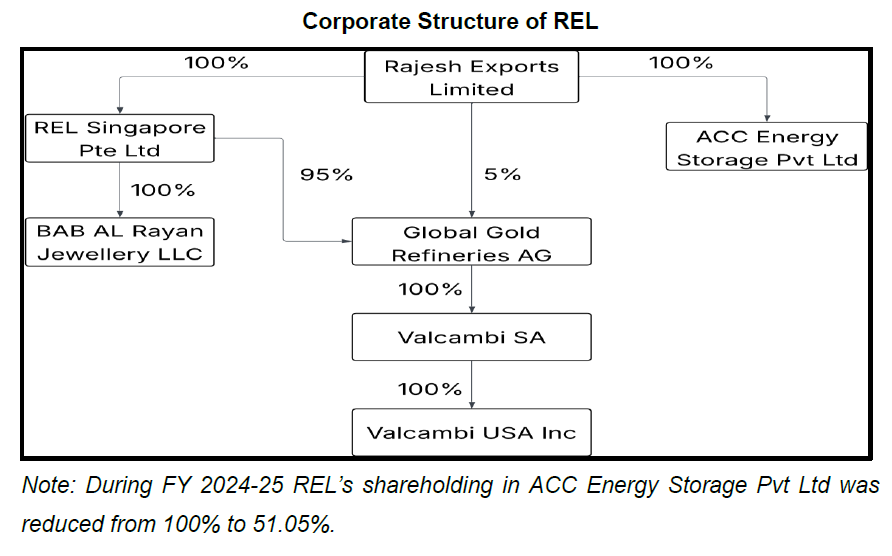

So naturally, SEBI began looking at those subsidiaries, whose corporate structure itself is a bit of a maze.

REL owns a Singapore subsidiary called REL Singapore and an Indian company called ACC Energy Storage Pvt. Ltd. REL Singapore, in turn, owns a few other foreign entities. But to keep things simple, you’ll only need to remember two of them. Because, according to REL, much of the group’s gigantic revenue came from these companies. One, a Swiss company called Global Gold Refineries AG (GGR) and another, Valcambi SA, a wholly owned subsidiary of GGR and one of the world’s most prestigious gold refineries.

So SEBI did the obvious thing. It examined their financial statements.

What it found was startling. Valcambi’s audited financial statements, signed off by KPMG, showed annual revenues of less than 0.2% of what REL had been claiming.

But REL argued that Valcambi only recorded “processing fees” in its books, while the real gold sales revenue sat in GGR’s books.

That explanation created another problem, though. GGR itself is merely a parent holding company. It doesn’t actually run business operations. What’s worse is that GGR’s consolidated financial statements were not required to be audited under Swiss law.

So what SEBI alleges is quite serious. It claims that REL took unaudited and internally prepared numbers from a holding company, presented them as real revenues in annual reports, and ignored the audited numbers of the only actual operating business in the chain.

And this is exactly what SEBI estimates may have amounted to a misrepresentation of nearly ₹15 lakh crore in revenue over five years, or roughly 99.8% of revenues attributed to subsidiaries.

And yet, that’s only one part of the story. Because when SEBI turned to REL’s standalone Indian business, it found another set of strange transactions. Between FY22 and FY24, REL recorded sales and purchases worth ₹11,000 crore each to a company called Affluence Shares and Stocks Private Limited. In fact, these transactions accounted for almost 66% of REL’s standalone sales during that period.

Now think about that for a moment. A company buying and selling nearly identical amounts to the same counterparty, while making virtually no profit in the process, doesn’t exactly look like normal business activity.

SEBI decided to investigate further. And things quickly began falling apart. Affluence’s own filings showed it was primarily a stockbroker involved in financial advisory, brokerage and consultancy. Over those three years, the company itself reported revenues of just ₹113 crore. Nothing about its filings suggested it dealt in gold.

So when SEBI summoned Affluence, it got a shocking response from the company: “REL was never our client. We never had any agreement or transactions with REL.”

At this point, things became difficult to ignore. SEBI cross-checked bank records to understand what was really happening.

And here’s what it found. Affluence did have a client — Rajesh Mehta, the founder and Executive Chairman of REL. Mehta reportedly held a personal trading account with Affluence and used it to trade gold derivatives on the MCX commodity exchange. REL had transferred around ₹7.45 crore to Mehta’s personal account for this activity, and Mehta may have lost nearly half the money in derivatives trading before returning the balance.

Now, whenever a company transacts with promoters or connected parties, it must disclose those dealings to investors as “related party transactions”. But none of this was done. And seemingly, to cover this up, REL allegedly booked Mehta’s personal derivative trades as company-level gold sales and purchases.

The ₹7.45 crore transferred was merely margin money. But the actual trading value of derivatives would be much larger, which allegedly helped inflate REL’s turnover by over ₹11,000 crore using transactions that may never have been genuine business activity in the first place.

And if all of this wasn’t enough, SEBI says REL allegedly inflated revenues in other ways too.

Things like foreign exchange gains and losses, which are normally shown separately as “forex gain/loss”, were added into operating revenues and purchases. Even interest income from fixed deposits and mutual funds was allegedly booked under “Revenue from Operations” instead of “Other Income”.

Small accounting changes perhaps. But together, they made REL look like a much bigger operating business than it may actually have been.

But here’s the thing. Any scheme to intentionally mislead investors can only go unnoticed for so long. In REL’s case, cracks had already begun showing in 2023 when the company failed to publish its audit report and comparative cash flow statements. That’s a serious governance lapse. Because when a company doesn’t show you a cash flow statement, it’s effectively refusing to show where the money actually went.

The market did what it normally does. It reacted swiftly. The stock started falling sharply from its peak, and analysts increasingly began wondering whether something was fundamentally fishy.

And yeah, SEBI’s interim order now seems to connect many of those dots. In some ways, the market had already begun punishing REL years before the full picture emerged. What SEBI appears to have done is formally lay out the evidence behind suspicions that had quietly been brewing for nearly three years.

But there’s still one important thing to remember. This is just an interim order. Meaning REL and Rajesh Mehta have 21 days to respond, after which a full hearing will follow. The company, for its part, has strongly denied wrongdoing. It says there has been no revenue inflation and that SEBI’s findings stem from misunderstandings and incorrect assumptions.

That’s one heck of a confident response to allegations backed by detailed evidence and numbers. So for now, we’ll just have to wait and see where Rajesh Exports goes from here.

Until then...

Liked this story? Share it with a friend, family member or even strangers on WhatsApp, LinkedIn, or X.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

A message to all the breadwinners

You work hard; you provide and make sacrifices so your family can live comfortably. But imagine when you're not around. Would your family be okay financially? That’s the peace of mind term insurance brings. If you want to learn more, book a FREE consultation with a Ditto advisor today.