Weekly Wrapup: The Dhanlaxmi bank fiasco

Before we get to today's story, a quick recap of all the things we covered this week. On Monday we took the day off. On Tuesday we discussed CCI's issue with MakeMyTrip and OYO. On Wednesday we talked about India's battle with affordable housing. On Thursday we discussed why Google was fined by the CCI and finally we talked about ants.

With the wrapup out of the way, let's get to today's big story, shall we?

The Story

Running a bank is simple, right? You raise deposits. You mobilize funds. You lend some money out and you keep the interest. And as long as you keep doling out money to creditworthy individuals who pay you back in time, you’ll be good as gold.

You just need to keep repeating this simple maxim. Seems easy enough, no?

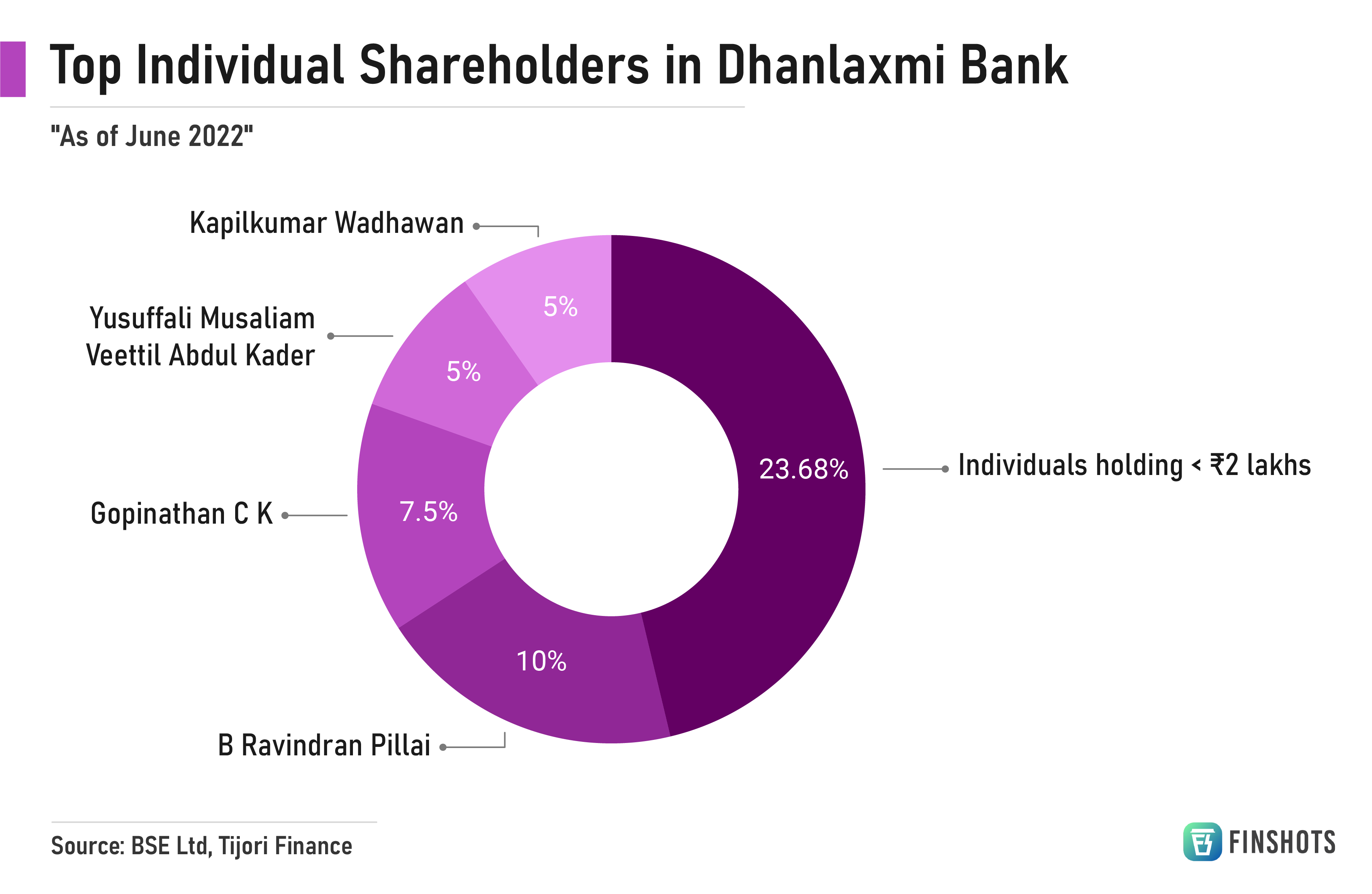

Well, tell that to the shareholders of 95-year-old Kerala-based Dhanlaxmi Bank. The bank’s share price has crashed by 93% since 2010. It’s almost a penny stock now (below ₹10). Meaning if you has invested ₹1 lakh back in 2010, you would be left with a paltry sum of ₹7,000 now.

And last week, the shareholders had enough.

They think that the CEO is spending money willy-nilly when the bank is already in dire straits. So they revolted. They now want to restrict his spending power. So if he wants to open new branches, that won’t be possible. If he wants to upgrade the IT systems, that’s a no go too. He can only pay staff salaries and he can’t do much else.

That’s harsh!

Now here’s the thing…this isn’t the first time shareholders have revolted at Dhanlaxmi Bank. And it probably won’t be the last. But to understand what’s going on, we have to understand the legacy bank’s history.

Since its inception in the 1920s, Dhanlaxmi Bank followed the basic principles of banking. Raise deposits. Lend money. Pocket the interest. And it did this quite well. It focused on building relationships with small businesses. It built up its retail book slowly and steadily. It stuck to its area of competence and didn’t experiment all that much.

But times change and the bank didn’t want to be left behind. It wanted to change its image — from a sleepy old legacy bank to a nimble gazelle. It wanted to be tech-savvy. It wanted a pan-India presence.

And in 2008, Amitabh Chaturvedi came on board to usher in a new era for the regional bank. He was someone who’d risen through the ranks at ICICI Bank and then at Reliance Capital. Everyone believed he could bring private sector aggression into Dhanlaxmi.

It worked.

In just 3 years, the bank’s loan book grew from ₹2,500 crores to ₹10,100 crores. Its deposits surged from ₹3,400 crores to ₹13,800 crores. It opened 66 new branches across the country. And its employee strength tripled.

Chaturvedi also did this by staying in the good books of the Trade Union. He raised salary levels, gave jobs to the employees’ children, and he even offered to relocate the Keralites working in other metros. Things were looking up.

Oh, he actually changed the name of the bank — from Dhanalakshmi to Dhanlaxmi. Don’t ask why!

But all this came at a cost. And the cracks began to appear soon after. Expenses were rising out of line. Income began lagging behind. The old guard began retiring and new employees weren’t allowed to join the employees’ union.

3 years into his tenure, tensions flared up again. In October 2011, the employees’ union said that the top management was window-dressing the accounts. That they were finding novel ways to show profits. That they were recognising income that they didn’t receive upfront, while staggering expenses over a period of time.

The RBI got involved and began an investigation. After all, the capital adequacy ratio — a figure that tells you about the kind of money available to cushion against future losses, fell from 14.44% in 2009 to 10.81% in 2011. The bank was pursuing its expansionary goals too quickly by spreading itself too thin.

The Bank’s board stopped backing Chaturvedi. They wanted him to cease the wanton expansion and cut back on lending. And he did. Soon, income dried up, while the costs remained elevated.

Chaturvedi really had no option but to quit the bank.

And by August 2012, its auditor Walker Chandiok and Co. threw its hands in the air and resigned too. Something to do with financial irregularities.

Things were so bad that in 2015, the RBI stepped in. The regulator placed the bank under something called the Prompt Corrective Action (PCA) framework.

Being put on this list is usually bad news. Sure, the objective is to ensure that the bank protects its capital and does not go bust. But it also means restrictions on lending out money. You know, the very things that pad the coffers.

And it took nearly 4 years for the bank to get its financial act together and become a free bird again. Well, sort of.

Because financial matters are one thing. But what if there’s another problem? The elephant in the room — Culture.

For a Kerala-based legacy bank trying to find its feet in the new world, the biggest hurdle was preserving the ‘culture’ built so painstakingly over the years.

You see, between 2003 and 2020, the Bank had 7 CEOs. And 5 of them did not last their full term. Even seasoned Board members jumped ship citing problems with the management and a toothless board.

And when in 2020, the RBI appointed Sunil Gurbaxani as the CEO, shareholders waited just 6 months before ousting him. Apparently, he was making the same mistakes as his predecessors — ignoring the bank’s South Indian roots in the quest for growth.

At that time, the general secretary of the All India Bank Employees’ Association wrote to the RBI Governor. His request was simple — “Please find a person who understands the bank’s history. Its legacy. Its customers and shareholders.”

Or, as one expert told Forbes, “Essentially, the problem is that Dhanlaxmi is a Kerala-based bank, and as management, you really need to understand the local sentiments. You need to behave and act like a local to win over the shareholders which had been missing for many years.”

Running a bank isn’t so simple after all. Being overly aggressive is one thing, but, you need to cater to ‘sentiments’ too it seems. Especially if you’re an outsider who has been brought in to run the show. You’re beholden to the shareholders and their whims and fancies.

So you could argue that shareholders ought to be selecting the top brass then?

And they kind of did. The next appointment was Kerala-based banking veteran J K Shivan. In fact, the RBI actually asked the bank’s board to get support from the shareholders before appointing him. Which they did. 99.81% of the shareholders gave the green light.

But barely 1.5 years later, it’s the same J K Shivan who’s facing the ire of shareholders. It’s his powers they want to curtail now.

So now the question is — if an RBI-appointed person isn’t good enough; if someone the shareholders chose is also not good enough; what’s next for the bank that’s clinging on to its ‘DNA’?

Also, how responsible is the RBI for this mess — You see, the RBI has nominees on the board of the bank too and it’s being accused of sleeping at the wheel.

How will Dhanlaxmi Bank get out of this mess?

The simple answer is that it needs to urgently raise capital to get its house in order.

But it also needs to sort out the constant battle among the shareholders, board, and management. If that doesn’t happen, it won’t be the last time you hear about troubles at the 95-year-old Dhanlaxmi Bank.

Until then…

Don't forget to share this Finshots on Twitter and WhatsApp.

Ditto Insights: The best way to save on health insurance premiums

A recent survey claims that 38% of Indians saw their health insurance premiums rise by 50% in just a year!!

It’s no secret that insurance is becoming costly every year with treatment costs on the rise.

Here are a few ways you can avail discounts on your plan to massively save on premiums:

1. Multi-year plans: In case you’re unaware, a multi-year plan is an amazing way to save on premiums. Insurers offer customers the option to lock in premiums for 2–3 years by paying a lumpsum amount. This is often accompanied by discounts in the range of 10–12%.

Now you might say- “This is just another way for insurers to make more money”. But price hikes have become common nowadays and with medical inflation at major highs, buying a multi-year plan makes some sense.

2. Wellness Discounts- Every insurer wants its policyholder to stay fit. If no health issues come up, insurers can kick back & relax. This is why they’ll offer you discounts if you show some initiative to remain healthy.

This may be judged through a series of tests or may be measured by how many steps you walk in a day. Either way, you have another incentive to stay fit :)

3. Buying early: Some insurers even offer you discounts if you buy really early in life. What’s more, when you buy when you’re young and healthy you get very comprehensive policies at low premiums.

And if you’re looking to buy comprehensive health insurance, you can always talk to our advisors at Ditto.

1. Just head to our website — Link here

2. Click on “Chat with us”

3. Put in your query

4. Sit back and relax! Our advisors will take it from there!