The OYO IPO Explained

In today’s Finshots, we break down OYO’s latest IPO attempt and explain why the company hitting the public markets looks nothing like the one you remember.

But here’s a quick sidenote before we begin. We’re looking for a business writer to join Finshots’ newsletter team. If you’re someone who can tell compelling stories and explain financial concepts in plain English without drowning readers in jargon, do consider applying through the link here. Or share this with someone who might be a good fit for the role.

Also, just a heads-up before we dive in. This is one of those stories that’s going to be a bit longer than usual.

With that out of the way, let’s dive into today’s story.

The Story

Few Indian startups have enjoyed a journey quite as dramatic as OYO.

Launched back in 2013 as a quirky budget-hotel aggregator, the company’s initial playbook was simple. Paint the town red. Literally.

OYO went on a hyper-aggressive expansion spree, slapping its red-and-white logo on thousands of independent guest houses and budget hotels across India. Before long, it replicated this massive blitzscaling model overseas, expanding into Southeast Asia, Europe, and the US, briefly becoming one of the world's largest hotel chains by room count.

Then, reality hit. Mounting disputes with disgruntled hotel partners and a pandemic that brought global travel to a grinding halt meant the company found itself battling massive operational losses until as recently as 2023. As a result, it was forced to shelve its highly anticipated initial public offering (IPO) and head back to the drawing board.

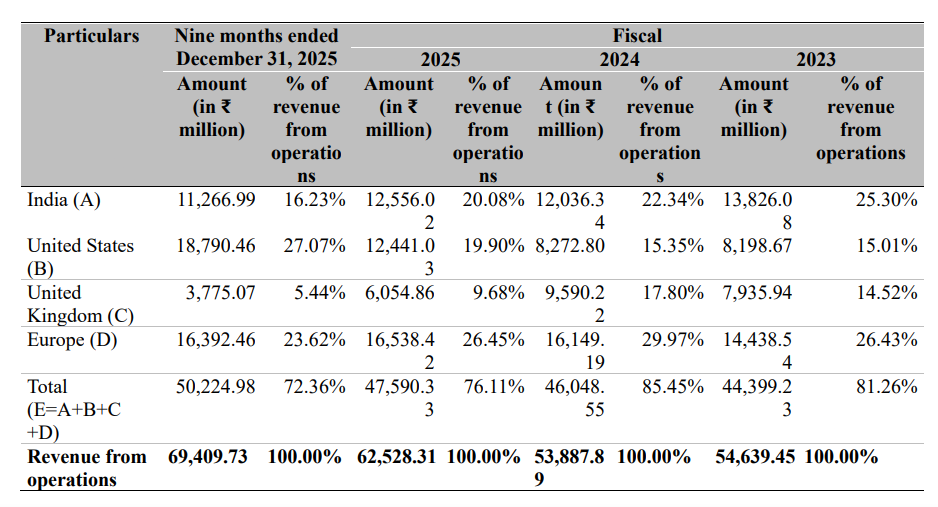

Fast forward to today, and OYO is back for a second round at the stock market. But if you look closely at its draft prospectus, you'll quickly realise that this is a completely mutated beast. In fact, it is barely even an Indian business anymore.

Because only around 20% of OYO’s revenue last year originated from India. A massive chunk of this international shift is thanks to its aggressive global footprint and, specifically, its recent acquisition of G6 Hospitality (the massive US operator behind the iconic Motel 6 and Studio 6 lodging chains).

And that’s not the only unusual thing about this listing.

Usually, when a high-profile startup goes public, the founders pitch a grand narrative about chasing growth, entering new markets, or building futuristic tech. OYO isn’t doing that. Instead, it is using the bulk of the public’s money to clean up its house.

For context, out of its massive proposed fresh issue of ₹6,650 crore, the company has earmarked a whopping ₹4,987 crore purely to repay the debt it took on to acquire G6 Hospitality.

To put into perspective how massive this financial engineering move is, the fresh issue itself is actually larger than OYO’s entire net worth, which stood at ₹6,146 crore as of December 31, 2025.

This brings us to the ultimate question on every investor’s mind: Is OYO actually a good business now?

If you look at the profitability metrics, OYO was bleeding cash not too long ago, reporting a loss of ₹1,286 crore in FY23. But then, in FY24, it swung into the green, scraping a profit of ₹229 crore, which ticked up to ₹245 crore in FY25. The momentum seems to be compounding, too. During just the first nine months of FY26, OYO’s profits surged to an impressive ₹748 crore.

But how did a company that was structurally unprofitable for a decade suddenly start minting money?

Well, it wasn't because revenues went through the roof. It happened because of three main things.

One, it slashed its employee costs by more than half, from around ₹1,548 crore in FY23 to about ₹600–700 crore from FY24 onwards.

At the same time, its gross profit margin expanded from 42.6% in FY23 to nearly 61% in the first nine months of FY26 (9M FY26). OYO proudly claims this margin profile is now among the highest in the entire listed hospitality sector.

An even more meaningful metric that supports this is Adjusted EBITDA (or operating profit) margin. Back in FY23, OYO’s Adjusted EBITDA margin was 5% of revenue. By the first 9 months of FY26, that figure had climbed to 28.35%.

What's even more surprising is how OYO stacks up against some of the world's biggest travel platforms. Measured as a percentage of Gross Booking Value (GBV), OYO reported an Adjusted EBITDA margin of 8.6%, comfortably ahead of Booking.com (5.4%), Airbnb (5.0%), MakeMyTrip (2.0%), and TBO Tek (Travel Boutique) (1.1%).

So operationally, OYO appears to be in a far healthier position than it was just a few years ago. However, profitability isn’t just about operating margins, and that’s where things get a little complicated.

Which brings us to the biggest accounting surprise ahead of the IPO: the deferred tax credit.

Simply put, it's an accounting adjustment that lets a company recognise tax benefits today for losses or tax deductions it expects to use in the future. It doesn't bring in any cash, but it can make profits look higher on paper. And in OYO's case, that's exactly what it has done.

To give you a sense of how significant that is, in FY24, OYO’s deferred tax gain was about ₹51 crore. In FY25, it jumped to about ₹767 crore, and in the first nine months of FY26 it was still very large at about ₹559 crore. That accounting benefit helped lift reported profit sharply even though profit before tax was much lower.

Strip out that benefit, and the picture looks far more subdued. In 9M FY26, OYO reported a profit before tax of about ₹245 crore. Even that included another one-off gain of ₹129 crore from selling or reducing its stake in subsidiaries. So it's a much better indicator of the company's underlying operating performance than the headline profit after tax of ₹748 crore. And since the company has not yet reported Q4 FY26 numbers, the full-year outcome is still not known.

Yet, the most fascinating part of this story isn't the financial adjustments or cost-cutting, but the massive strategic pivot happening behind the scenes. OYO is killing off the exact business model that made it a household name.

For years, OYO was known as the ultimate saviour for budget travellers looking for a cheap, ₹999 room. Today, OYO wants to be a premium hospitality player.

Starting in FY24, the company began aggressively rolling out its "CheckIn" portfolio, which features upscale, curated brands like Sunday, Townhouse, Palette, and Clubhouse. Crucially, instead of just listing these independent hotels on an app and hoping for the best, OYO is shifting toward a company-serviced model.

This means OYO steps in to directly manage or heavily service these premium properties, giving it total control over the things that used to plague its budget network: service quality, dynamic pricing, food, housekeeping, and the end-user experience.

In FY24, these company-serviced premium hotels accounted for a measly 2.6% of OYO’s Gross Booking Value (GBV) in India. Fast forward less than two years, and that tiny sliver has exploded to 49.3%.

In other words, nearly half of OYO's Indian booking value now comes from premium, company-managed properties. OYO has essentially embraced the Pareto Principle (Of course, it’s not exactly 80/20, but the principle still stands). Instead of onboarding thousands of low-yield budget hotels that cause operational headaches, it is focusing heavily on earning far more money from fewer, higher-quality properties.

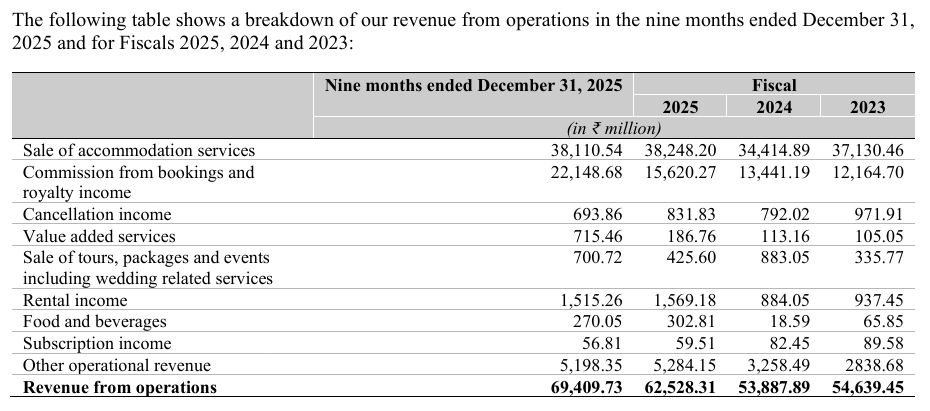

The company's revenue mix reflects this diversification. While traditional accommodation bookings still account for 55% of operating revenue, 32% now comes from commissions, franchise royalties, and management fees (especially post the Motel 6 deal). It’s also unlocking niche revenue streams like workspace rentals, marketing services for hotel owners, travel packages, OYO Wizard subscriptions, food services, and even cancellation fees. It is trying hard to morph from a simple booking app into a diversified corporate hospitality platform.

But before retail investors get completely swept up in this turnaround narrative, there are some serious, unresolved risks hanging over this IPO.

First is their operational strategy.

Managing premium properties directly is a double-edged sword. It boosts margins and control, but it also locks the company into higher operating costs. So, investors can only wonder whether OYO can grow its premium business fast enough to offset the gains from cost-cutting.

Second, there is a massive legal dark cloud floating above OYO’s head: the long-running litigation with rival startup Zostel.

The dispute dates back to OYO's failed attempt to acquire Zostel nearly a decade ago. Both companies had signed what OYO says was a non-binding agreement to explore a deal. But when the acquisition did not go through, Zostel argued that OYO had backed out despite Zostel fulfilling its obligations, while OYO maintained that no final contract was ever signed and the deal was never meant to be binding.

That disagreement has snowballed into a legal battle that's dragged on for years.

And it’s still far from over. After the Delhi High Court set aside an earlier arbitral award that favoured OYO's parent company (Oravel Stays) last year, Zostel appealed to the Supreme Court.

OYO has already filed its official reply, and the matter is officially on the calendar for a final hearing and arguments on July 8, 2026 (yes, next week).

But legal feuds happen all the time. Why should an investor care about this, you ask?

Because if OYO loses this battle and the courts issue a final, non-appealable order against it, it could be legally required to transfer or issue up to 7% of its total equity shareholding to Zostel and its partners.

Alternatively, the court could order OYO to pay the cash equivalent of that 7% stake. Either way, it would trigger a massive equity dilution or a cash drain, severely damaging the company’s ownership structure, financials, and public reputation right after listing.

So there you have it, folks ― a brief breakdown of the Oravel Stays IPO.

Even after all this, the one thing that I keep wondering is the supreme irony of this IPO. The company is seeking public funds while actively dismantling the identity it spent a decade building. It became a unicorn by promising scale over margins and chasing volume at the bottom of the pyramid.

Today, that philosophy has been completely flipped on its head. OYO has realised that doing fewer things with greater precision is more profitable than trying to aggregate every budget guesthouse on the planet.

But the transformation is far from complete. With most of the IPO proceeds going toward debt repayment rather than funding future innovations, and a significant equity litigation risk coming to a head in court next week, investors will have to decide whether they are willing to back this premium avatar.

Because if they decide to bet on it, they will no longer be betting on an Indian budget hotel aggregator, but on a global, asset-light hospitality platform trying to prove that it can outrun its past.

Until then…

If this story helped you make sense of OYO’s current business and DRHP, share it with a friend, family member or even strangers on WhatsApp, LinkedIn, and X.

🚨 ATTENTION: FINSHOTS FAMILY

This weekend, we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Friday, 3rd July at 6:30 PM: Life Insurance: How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Saturday, 4th July at 10:00 AM: Health Insurance: How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.