What’s up with all the excitement around Reliance Industries?

In today’s Finshots we tell you why Reliance Industries is making big pivots in two of its verticals and why the street is getting bullish all over again.

The Story

Unless you live under a rock, you know that Reliance Industries (RIL) is one of India’s most influential conglomerates, housing hundreds of brands under its umbrella. Chances are you’ve interacted with a few Reliance products even before reading this sentence.

And when you stack it up in numbers, it’s massive.

It coughed up a consolidated net profit of ₹81,300 crores in FY25. Its total assets have crossed over ₹19 lakh crore. And the market currently values the company at over ₹20 lakh crore.

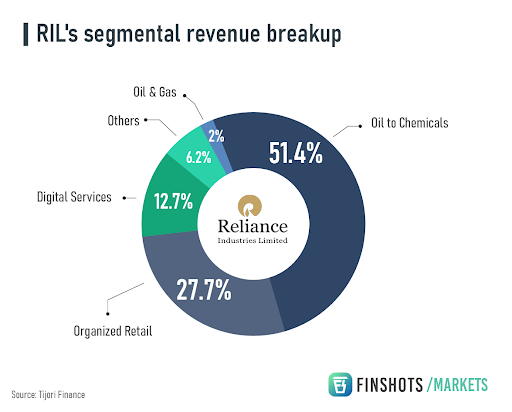

Now, with all the businesses Reliance dabbles in — from oil refining to telecom to retail, things can feel a bit jumbled. But if you slice it down, the core segments are pretty clear: Oil to Chemicals (O2C), Organised Retail, Digital Services and Oil & Gas — most of which are doing pretty well in terms of growth.

But today, we’re focusing on just two segments and pivots that have got analysts excited all over again.

The first one is its ‘New Energy’ vertical.

Think of this as an empire that RIL is building for its future. And we say that because within a year of its announcement, the company has started pouring money and building capacity for it in Jamnagar.

It recently built its first 1 GW (gigawatt) capacity solar panel manufacturing plant, and has already started production. These aren’t just any panels but high-efficiency Heterojunction Technology (HJT) modules, which offer better efficiency (by over 20%) than standard tech and command a premium selling price. They’ve even made it to the government’s Approved List of Models and Manufacturers (ALMM), meaning they can be used in subsidised projects.

If that seems like a big deal, hear this out — it’s just the beginning; because RIL wants to scale this 1 GW to 10 GW by 2026, and eventually a target of 20 GW of fully integrated solar manufacturing — from raw polysilicon to finished modules. So while its own solar power projects may take time to come online, it’s already selling panels to domestic players.

And it’s not stopping at panels. Reliance is building a 30 GWh annual capacity battery factory to store renewable energy by 2026. That’s huge because batteries are crucial infrastructure of this business chain and as India transitions to renewables, this new plant could give RIL a new foothold in that future. And talking about the future, the company also wants to build a fully integrated Green Hydrogen line and aims to be among the first large-scale producers globally.

So obviously, market participants are bullish.

Nuvama estimates that at 75% utilisation rate, just the solar module plant we spoke about, could add ₹3,800 crore to net profits (which is 6% of the company’s FY25 profits). By FY30, New Energy profits could soar to ₹11,000 crore, contributing 9% of overall profits. And applying similar valuation multiples of its peers like Waaree and Premier Energies, RIL’s solar business alone could be valued at a whopping ₹1.7 lakh crore.

Then there’s the second big rejig – FMCG.

Reliance is grouping all its in-house and acquired consumer brands—Campa Cola, Independence, Sosyo, Lotus Chocolates and more, under a new company: New Reliance Consumer Products Ltd (New RCPL). The idea? Give focused attention to FMCG brands (which are currently scattered across its retail verticals like Reliance Retail and Reliance Consumer Products), ready the retail arm for a share sale (since the FMCG business will be separated) and eventually unlock shareholder value.

You see, Reliance has one of the deepest retail distribution networks in India — over 18,000 stores and millions of kirana partners. So if it plugs its FMCG brands (which is already the fastest growing in India) from a separate entity into this network efficiently, it can build consumer stickiness the way it built Jio’s subscriber base. Fast, aggressive and widespread.

And there’s enough excitement on the street for this spin off, especially because it will allow RIL to IPO its retail business.

All of which brings us to the question we want to answer: Is all the excitement around these changes justified?

Well, you could say yes for a few reasons.

The New Energy business isn’t just diversification. It’s a play for long-term survival. O2C, which is still Reliance’s biggest profit engine, faces long-term headwinds from climate regulations, carbon taxes and falling oil margins. So, the New Energy shift is a hedge against the future, and a way to ensure energy dominance even after oil.

The FMCG restructuring mirrors its telecom and retail disruption play. Own the product, own the distribution, price aggressively, scale rapidly and turn it into a separate entity when the time is right. And this sends out a strong brand messaging. With the brands now grouped under one clear FMCG play, the path to monetising it is more visible and lucrative.

And then you need to look at RIL’s transition history and execution.

Think back to the 2000s. Reliance made most of its money refining crude oil and converting petrochemicals into polyester. But around 2010, when margins were starting to shrink, it made a telecom pivot by pouring billions into fibre and towers and triggering a price war. Suddenly, Reliance wasn’t just a refinery company anymore. It was digital, retail and subscription-driven.

And that tells us something crucial about how it thinks. When old cash flows start looking vulnerable, it doesn’t defend. It attacks. And today, we’re seeing that same playbook unfold again.

Investors still remember how the street was sceptical of Jio in 2016, and how quickly that changed. Betting against Reliance’s scale and ability to pull off complex projects hasn’t paid off well in the past.

And the final piece of the puzzle is valuations. Assign standalone valuations to Jio Platforms, the Solar + New Energy segment, factor in O2C’s steady cash flows, plus the growth in retail and FMCG brands — and the math does point to an upside. Of course, that hinges on Reliance actually delivering on execution.

But of course, there are hiccups too.

Solar manufacturing, for one, is a margin game. Chinese players flood the market with ultra-cheap modules. HJT panels, while superior, are costlier to produce. If Reliance can’t cut costs fast, premium pricing might not be sustainable. In fact, Reliance already felt a similar squeeze in its O2C business last quarter when Chinese oversupply dragged prices down. So it diverted exports to India (where profits margins were better) to cushion the blow and it worked well. But whether a similar playbook can be replicated in solar remains to be seen.

FMCG is another battlefield. It’s dominated by legacy giants like HUL, ITC, Nestlé. And building mass-market love needs years of marketing muscle, brand building, and consistency. So far, there’s limited visibility on how much money RCPL will make. That said, the intent for long term market capture with Jio-like strategy seems clear. Take Campa Cola, for instance. It’s crushing the bottled beverage market, and new launches are ramping up.

And finally, there’s the risk of capital stretch. Between New Energy, telecom expansion, retail growth, and FMCG scaling, Reliance is investing across the board. Managing these capex-heavy bets without straining debt levels and free cash flows will be key.

Nevertheless, what the Street is betting on isn’t just the numbers but RIL’s track record — one which shows that when it picks a sector, it doesn’t just dip its toes in; it rewires the whole thing. And that’s why you’re seeing 15–20% upside targets from various research houses.

But should you buy into the hype?

Well, we’re no stock or valuation experts. And at the end of the day, projections are just that — best guesses wrapped in a layer of optimism. Some might hit the bullseye, others could shoot past it and a few might not even come close.

So if you want to track the story yourself, just follow the signals.

See how fast those solar modules move off the line and at what profit margins. Whether the battery ambitions are charged up with consistent capacity additions. If green hydrogen moves from promise to production. Perhaps even keep an eye on what RCPL adds to the FMCG basket, and how much of it ends up in yours. Listen in when the AGM rolls around, especially about New Energy targets and spin-off timelines. Check how Jio and retail keep adding to the cash pile. And whether Reliance can juggle all of this without letting its balance sheet wobble.

Because for now, it’s not just a growth story but a transition story. But for the excitement to last, the delivery will have to do the heavy lifting.

Until then…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

Did you know? Nearly half of Indians are unaware of term insurance and its benefits.

Are you among them?

If yes, don’t wait until it’s too late.

Term insurance is one of the most affordable and smartest steps you can take for your family’s financial health. It ensures they do not face a financial burden if something happens to you.

Ditto’s IRDAI-Certified advisors can guide you to the right plan. Book a FREE 30-minute consultation and find what coverage suits your needs.

We promise: No spam, only honest advice!