Sun Pharma is marrying Organon

In today’s Finshots, we briefly explain Sun Pharma’s acquisition of Organon.

But here’s a quick sidenote before we begin. If you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

Now, on to today’s story.

The Story

A few days ago, the largest overseas pharmaceutical deal in India’s history was announced. Sun Pharmaceutical Industries said it would acquire US-based Organon & Co. for $11.75 billion.

So let’s skip the fluff and get straight to the meat of this deal.

Sun Pharma needs little introduction. There’s a good chance you’ve used its medicines, whether it’s Volini Gel for aches and pains or Pantocid, the generic version of a patented drug used to treat acidity.

But Sun Pharma isn’t just a branded generics player. And it didn’t start out as one either. The company was founded by Dilip Shanghvi, who began his career working in a modest pharmaceutical distribution business in Kolkata with his father. That early exposure gave him a sharp understanding of medicine pricing and supply chains, something that proved invaluable when he launched Sun Pharma in 1983.

Back then, it was a tiny operation with just a two-person marketing team. And in its early days, Sun Pharma focused on a handful of psychiatric medicines, including treatments for bipolar disorder. It wasn’t a random choice. This was an underserved segment at the time, which meant fewer competitors and better margins.

In the same year, the company set up its first manufacturing facility for tablets and capsules in Vapi, Gujarat. From there, it expanded steadily, moving into cardiology, investing in research, and tapping into exports.

Today, Sun Pharma is India’s largest pharmaceutical company, present in over 100 countries. It clocks over ₹52,000 crore in global sales and ₹10,900 crore in profits, growing at a CAGR of 12% and 39%, respectively, since FY21.

But no company suddenly becomes this big, no? There’s always something in between. And for Sun Pharma, that “in between” is a story of acquisitions.

The company leaned heavily on acquisitions to speed up its growth, picking up plants, brands, and overseas businesses across India, the US, and other markets. Some of the most notable ones include Taro Pharmaceuticals in 2010, known for dermatology and generic over-the-counter medicines, and Ranbaxy Laboratories in 2015, another speciality generics company. Over time, these deals helped Sun Pharma become far more international than most of its Indian peers, with a large chunk of its revenue, about 60%, coming from overseas markets.

And now, it wants to go a step further to move up the global pharma ladder. And for that it’s acquiring Organon.

Organon is an American pharmaceutical company that was spun off from Merck & Co. in 2021. It generated roughly $6 billion in revenue in 2025, with an adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortisation) of about $1.9 billion, translating into a margin of nearly 30%.

But here’s the thing. Organon derives about a third of its revenue from the US. So does Sun Pharma. So even after the acquisition, Sun Pharma’s exposure to the US isn’t really going to change much.

There are a few other problems too. A 2025 probe found that Organon pushed excess sales of Nexplanon, a women’s contraceptive implant, to wholesalers, inflating numbers in the short term. That eventually showed up in its performance, with 2025 sales slipping by 3–4% compared to the previous year. In fact, management has already guided that 2026 sales will remain more or less flat.

And then there’s Organon’s balance sheet. When it was spun off from Merck, it inherited a hefty $8.6 billion in debt, but had just $574 million in cash. That translates to a net leverage of nearly 4.5 times. That’s a measure of how easily a company can pay off its debt using its operating earnings.

Compare that to Sun Pharma, which has stayed almost debt-free all these years, and you’ll be forced to ask, “Why take over a company that’s recently been caught in controversies, has slowing sales, and, more importantly, brings a large pile of debt onto the books?”

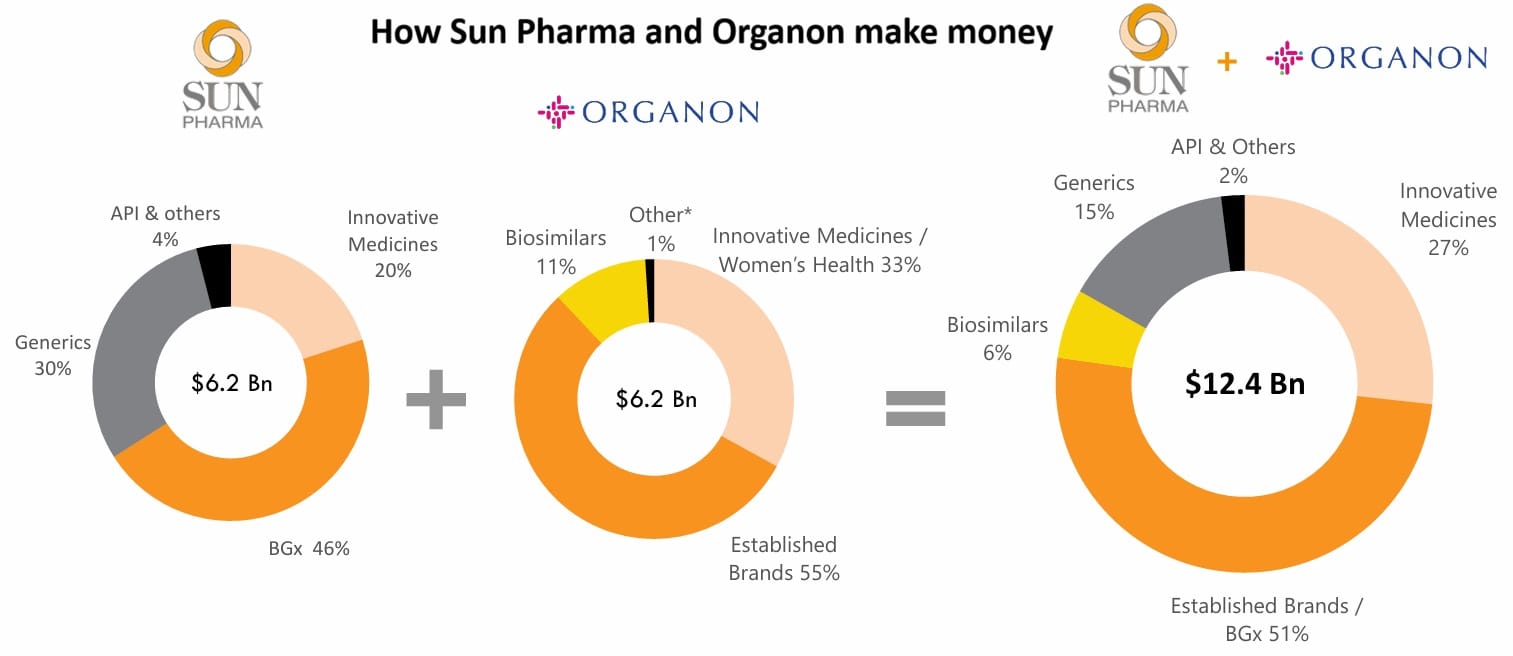

Well, the answer lies in understanding how Organon makes its money and a bit of its past. Much like Sun Pharma, where a big chunk of revenue (nearly half) comes from branded generics, about 55% of Organon’s revenue also comes from a similar business. But it’s the rest of Organon’s business that Sun Pharma doesn’t really have.

For context, Sun Pharma earns the remaining share of its revenue from unbranded pure generics (30%), innovative medicines (20%), and APIs (Active Pharmaceutical Ingredients) and others (4%).

But the remainder of Organon’s revenue mix looks quite different.

First, there’s innovative medicines and women’s health, which together bring in about 33% of its revenue. This is an area Organon has always been deeply focused on. But after inheriting a massive pile of debt from its Merck spin off and dealing with bloated supply chains that took time to fix, the company found itself in a tight spot. Much of the cash its business generated had to be paid out as dividends to keep investors on board. That left very little room to invest in growth — things like new products or marketing.

Then there’s the bit about Nexplanon. It’s a matchstick-sized implant placed under the skin of a woman’s inner arm to prevent unplanned pregnancies by releasing the hormone progestin, which stops ovulation. At its peak, it was Organon’s top-selling product, generating over $1 billion annually.

But things changed when its patents began to expire. Cheaper generic versions entered the market, pulling sales down. And Organon couldn’t fight back effectively since it didn’t have enough capital to invest in improved versions or new alternatives, as we told you earlier. On top of that, the controversy around inflating Nexplanon’s sales numbers didn’t help its reputation either.

This is where Sun Pharma could step in and change the script. With its cost-efficient, India-style manufacturing and deeper pockets for research and development, it can potentially tweak and revive these products. More importantly, it also gets access to Organon’s global sales network. That means it can in-license (acquire rights to Organon’s drugs) and launch products faster, while investing in brand upgrades and operational synergies to scale them up again.

So, in a way, this deal is about taking assets that are losing steam and trying to turn them back into growth engines.

The second, and arguably the most important part of Organon’s revenue mix is biosimilars. They make up about 11% of its revenue, and interestingly, this is an area Sun Pharma had been quite sceptical about until now.

Biosimilars are a bit like generic medicines, but for complex diseases like cancer and arthritis. Unlike simple generics, they don’t just need to prove they’re chemically identical. They require rigorous clinical testing to show they’re highly similar to the original drug, though not full-blown new drug trials.

But the reason Sun Pharma stayed away from this space for so long was mainly because of regulatory uncertainty, especially around substitution and interchangeability, and the high costs and complexity involved in development, which can stretch over years. Instead, Sun Pharma stuck to what it knew best: making generics and simple molecule drugs. Meanwhile, competitors like Biocon, an early mover in oncology biosimilars, and Dr. Reddy’s built strong platforms and moved ahead.

But things have started to change. Dilip Shanghvi himself has pointed out that regulatory clarity, especially around how easily a biosimilar can replace the original reference product, has improved. And that makes the heavy investment in biosimilars easier to justify now.

More importantly, Sun Pharma isn’t starting from scratch. By acquiring Organon, it gets access to an existing biosimilars platform. And there’s an added bonus — its entry into China, where Organon generates over $800 million annually. It’s the world’s second-largest drug market, and Sun Pharma has had very limited presence there so far. So this deal opens multiple doors at once.

In fact, it could push Sun Pharma into the world’s top 25 pharmaceutical companies, up from being among the top 50 earlier.

And as for the debt, it’s true that it’s going to spike. Sun Pharma’s net leverage could jump to around 2.3 times from what was earlier a net-cash position. That likely means higher borrowing costs and possibly a pause on big dividend hikes until the debt is brought down. And then there’s the immediate pressure from Organon’s flat 2026 revenue outlook.

But if there’s one thing Sun Pharma is known for, it’s disciplined turnarounds.

A good example is its acquisition of Ranbaxy, which was Dilip Shanghvi’s 17th turnaround at the time. Sun Pharma bought the struggling Ranbaxy Laboratories for $4 billion in an all-stock deal from Japan’s Daiichi Sankyo, which was looking to exit after the US FDA banned Ranbaxy’s plants over data fudging and quality issues. Ranbaxy had lost access to the US market, sales had plunged, and debt had piled up.

But Sun Pharma took it up as a challenge and over the next 3–4 years upgraded plants, cleared re-inspections, shut down inefficient factories, and shifted focus to higher-margin drugs while expanding in emerging markets. The end result was that Ranbaxy stopped bleeding, added about 25% to Sun Pharma’s size, and helped it become India’s largest and the world’s fifth-largest generics player.

That track record offers some hope that Sun Pharma could attempt a similar transformation with Organon. There’s also an old link here. Sun Pharma’s psoriasis drug, Ilumya, actually traces its roots back to Organon’s labs.

So yeah, if things fall into place, the cash flows that the combined entity generates could effectively help it bring down debt quickly enough. The real test, though, is whether it can convert this scale into consistent profit growth. And that is something only time can tell.

Until then…

Liked this story? Share it with a friend, family member or even strangers on WhatsApp, LinkedIn, or X.

A message to all the breadwinners

You work hard; you provide and make sacrifices so your family can live comfortably. But imagine when you're not around. Would your family be okay financially? That’s the peace of mind term insurance brings. If you want to learn more, book a FREE consultation with a Ditto advisor today.