Why gold worries the Prime Minister

In today’s Finshots, we tell you why the Prime Minister doesn’t want you to buy gold and what could happen to the economy if you actually listen to him.

But here’s a quick sidenote before we dive in. We’re hiring a Content Writer at Ditto Insurance. If you like turning messy, complex topics into clear, helpful content that actually ranks (and gets read), and enjoy going beyond surface-level research, this might be for you. Check out our careers page for more or share it with someone who’d be a great fit.

Now onto today’s story.

The Story

You heard it. It’s all over the news and the internet. Prime Minister Narendra Modi does not want you to buy gold for another year, even if you have a wedding or special occasion at home.

The reason is simple. There’s a war in the Middle East. And that war is indirectly affecting India and the world by increasing the cost of fuel, food, and fertiliser. That’s because a large share of our fuel and fertiliser supplies comes through shipping routes in the Middle East.

If the Strait of Hormuz, through which many of these ships pass, gets disrupted because of the war, prices naturally go up. And when fuel and fertiliser become expensive, food prices rise too because you need fertiliser to grow food and fuel to transport it.

So the Prime Minister’s point is that even though prices are rising, the government is trying its best to avoid burdening the public. For instance, it is still providing fertilisers at subsidised rates and has not sharply increased petrol and diesel prices despite soaring crude oil prices.

In return, he suggests, citizens could also try to do their part by reducing expenses that force the government to spend more. For example, use less cooking oil because India imports over half of its edible oil needs. Reduce commuting by personal vehicles and use public transport, carpool, or even work from home when possible, since India imports nearly 85% of its crude oil requirements.

And most importantly, cut down on gold purchases because nearly 90% of India’s gold is imported. All of this forces the government to spend more of its foreign exchange reserves on imports.

While all of this may make sense, you may have noticed that the stock prices of most popular listed jewellery retailers fell by over 5% on average since Monday, the day after the Prime Minister’s speech.

And that may have been natural because investors worried that if people actually cut back on buying gold, demand could fall and these jewellers could earn less revenue.

Which makes you ask: “If I stop buying gold, how will it affect India’s economy?”

To understand that, let’s first see how buying gold affects the economy in the first place.

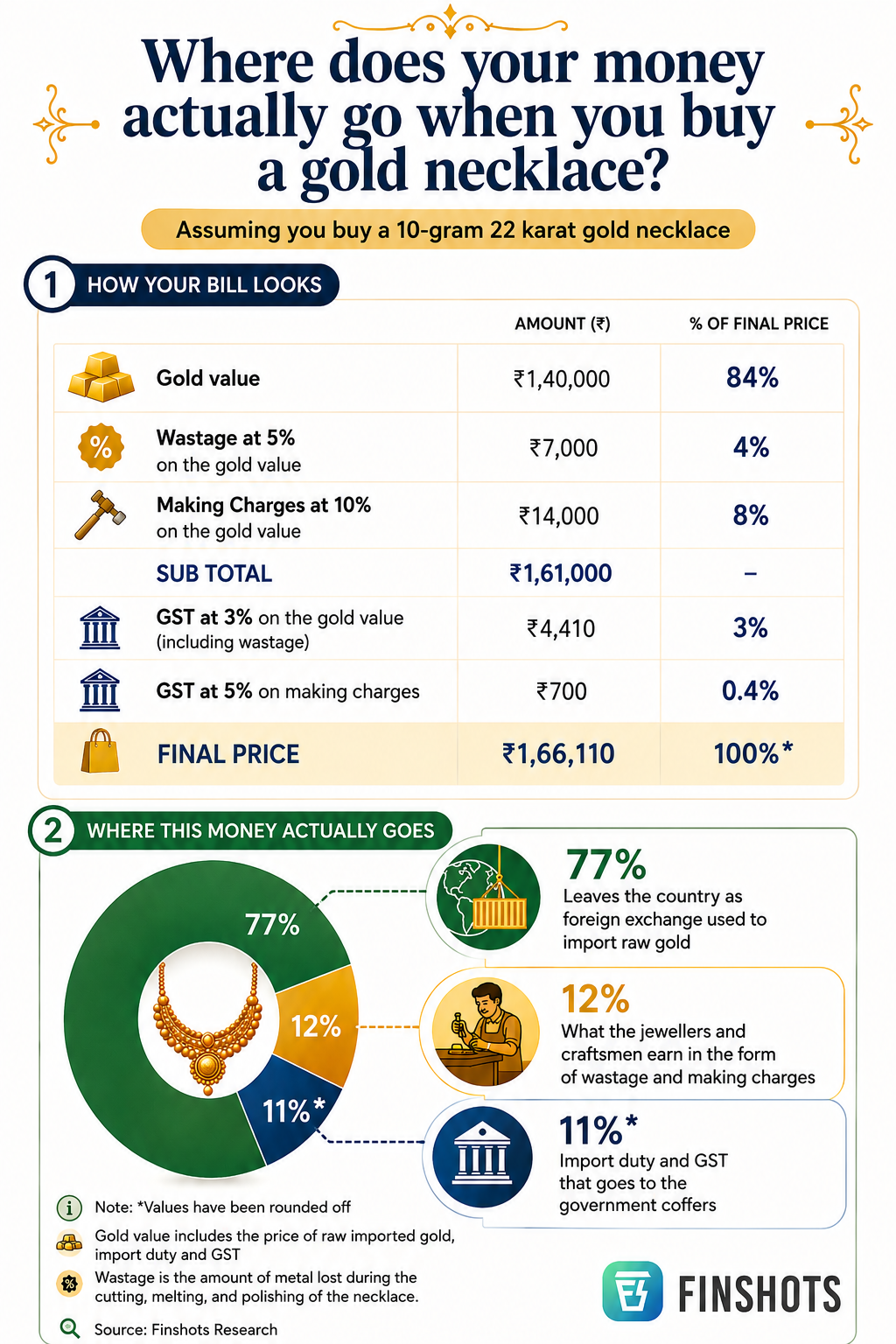

Say you buy a 10-gram, 22-karat gold chain today. Around 84% of the price you pay is simply the value of the gold itself. Out of that, the government only earns import duty and GST on the raw gold being imported. Together, that works out to roughly 7% of the final price you pay for the chain.

So most of your money doesn’t really stay in the economy. It leaves the country as foreign exchange used to import raw gold.

Once the raw gold is imported and refined, the domestic refiner charges about a 1% margin before selling it to the jeweller. And at every stage where the gold changes hands, the government also earns 3% GST.

Finally, when you buy the chain, roughly 12% of the final price gets split between the karigars (craftsmen) who make the jewellery and the jeweller’s profit margin, both of which are pretty thin.

And when you put all of this together, the gold industry contributes only about 1.3% to India’s GDP. The figure rises to around 7% only when you include the entire gems and jewellery sector. But a large part of that comes from exports and diamond processing, not from Indians buying gold jewellery domestically.

Yet, to generate this relatively small impact on GDP, India imports 700–800 tonnes of gold every year, worth nearly ₹6 lakh crore.

And most of that gold is not really productive for the economy because people mostly buy it either as an investment or to wear as jewellery.

Sure, you can take a gold loan against it during difficult times, which does help banks earn income. But even that depends on imported gold. And all these imports put pressure on India’s foreign exchange reserves and widen the current account deficit (the amount by which a country’s total imports exceed its exports).

In fact, India’s current account deficit rose to $13.2 billion, or 1.3% of GDP, in Q3 FY26, compared to $11.5 billion in the previous quarter. While there’s no exact figure showing how much gold contributed to this number, gold imports alone account for about 2.1% of India’s nominal GDP in the merchandise trade deficit (deficit that occurs when a country’s physical goods imports exceed its exports).

So yeah, the only real way to reduce this pressure is to depend less on imported gold.

And for that, there are only two options. One, rely more on recycled gold, which can save $95 million (₹893 crore) per tonne in imports. And two, simply buy less gold or don’t buy it at all.

The government has already tried the first option.

You probably know about Sovereign Gold Bonds (SGBs). The idea was simple. Instead of buying physical gold, people could invest in bonds linked to the price of gold. These bonds were denominated in grams of gold, paid annual interest, and also gave investors the benefit of any rise in gold prices when the bond matured. The government hoped this would reduce gold imports because people could invest in gold without actually buying the metal itself.

But as you know, it worked only to a limited extent. In fact, it ended up increasing costs for the government, which eventually stopped issuing these bonds quietly.

The government also tried Gold Monetisation Schemes in the past. Under these schemes, people could deposit idle gold lying at home with banks and earn interest on it. The banks would then melt that gold and recycle it to jewellers, who could use it as raw material instead of buying freshly imported gold.

If you wanted your gold back later, you would get back the same quantity of gold you deposited, but usually in the form of bars or coins, not your original jewellery.

And that’s exactly where the problem lies.

Even though Indian households are estimated to hold nearly 25,000 tonnes of gold, much of it carries huge sentimental value. These are family heirlooms, wedding gifts, or jewellery passed down generations.

And parting with that gold and letting it be melted away isn’t something most people would do, right?

Even if you leave household gold aside, there’s another place where a huge amount of gold is locked away — Indian temples.

Devotees often donate gold or adorn deities with gold jewellery and ornaments. And estimates suggest that Indian temples collectively hold between 2,500 and 4,000 tonnes of gold in the form of jewellery, coins, bars, and ornaments.

To put that into perspective, even the lower estimate is more than half the gold held at the United States Bullion Depository at Fort Knox.

Now, the RBI did try to convince some of India’s richest temples to disclose the value of their gold holdings. The idea was to understand how much gold could potentially be monetised if temples participated in Gold Monetisation Schemes, and how much India could reduce gold imports as a result.

But that’s a sensitive issue, and most temples were understandably not comfortable with it.

Which is why only a few like the Tirumala Tirupati Venkateswara Temple, one of the richest temples in the country, voluntarily participated in the scheme. As of 2024, the total gold it has deposited under such schemes stood at around 11,329 kg, which at today’s prices is worth roughly ₹17,100 crore.

So, with limited success from gold monetisation and similar schemes, the only other option left for the government is to encourage people to buy less gold or avoid buying it altogether for some time, just like the Prime Minister suggested — even if it means lower sales for jewellers and less work for the lakhs of artisans involved in making jewellery across the country.

But in India, having a wedding at home and not buying gold is a tough idea for most people to accept.

Whether people actually listen to the Prime Minister’s request in the interest of the nation is something that will be very interesting to see.

Until then…

Update: After publishing this story, the import duty on gold was hiked from the earlier 6% to 15% to discourage gold imports. But as we’ve explained here, higher import duties can also encourage gold smuggling. So, do you think the new hike will actually work?

If this story helped you understand the economics of postponing gold purchases, consider sharing it with your friends, family, or even strangers on WhatsApp, LinkedIn, and X.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

Message to all the Breadwinners

You work hard, you provide, and make sacrifices so your family can live comfortably. But imagine when you're not around. Would your family be okay financially? That’s the peace of mind term insurance brings. If you want to learn more, book a FREE consultation with a Ditto advisor today.