What happens when India runs out of urea

In today’s Finshots, we unpack how a distant geopolitical conflict could disrupt India’s fertiliser lifeline and what happens if the country runs short of urea.

But here's a quick sidenote before we begin. We’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 2nd May at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 3rd May 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.

👉🏽 Click here to register while seats last.

Now on to today’s story.

The Story

If there’s one thing that the current US-Iran war taught us, it is that the world grossly underestimates how much we are dependent on West Asia.

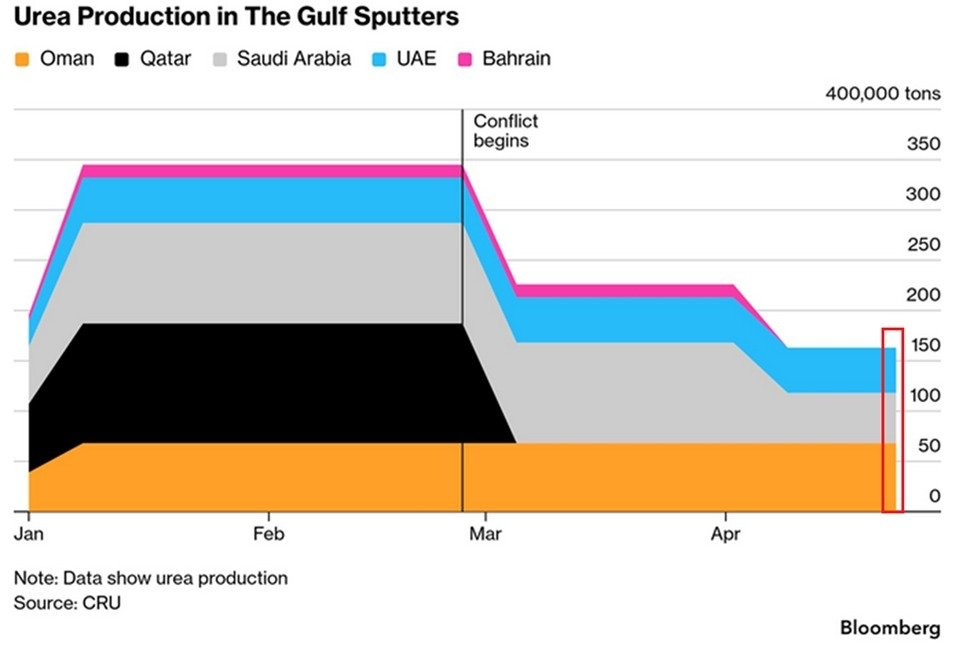

The ongoing conflict involving Iran has disrupted fertiliser flows from the Gulf, a region that accounts for nearly half of global urea trade.

You see, production there has dropped sharply, with weekly output falling by over 50% since the conflict began. On the surface, this may seem like just another commodity disruption. But urea is not just some input. It is the backbone of modern agriculture, used extensively in crops like rice, wheat, and corn. And when supply tightens, the impact does not stay confined to farms. It moves through the food system and eventually shows up in grocery bills.

And for India, the stakes are even higher.

The country consumes roughly 400 lakh tonnes of urea every year, but produces only about 300 lakh tonnes domestically. The remaining 25% comes from imports, a large share of which originates in the Gulf. At first glance, this may suggest partial dependence. But the reality runs deeper.

Because even India’s “domestic” urea is not entirely domestic.

Producing urea requires ammonia, and ammonia is made using natural gas. In fact, natural gas is both the fuel and the primary raw material in the process. Close to 80% of the cost of producing urea comes from gas prices alone. And here lies the hidden vulnerability. Around 86% of the natural gas used by India’s fertiliser plants is imported, much of it passing through the Strait of Hormuz, the same geopolitical chokepoint now under stress.

So even when India produces urea locally, it remains indirectly exposed to global disruptions.

That is only one side of the problem. The other lies in how urea is priced and consumed.

Farmers in India pay a fixed price of around ₹266 for a 45 kg bag of urea. The actual cost of producing or importing that bag ranges anywhere between ₹1,200 and ₹1,700. The difference is absorbed by the government through subsidies, which already run into lakhs of crores annually. This pricing structure has ensured affordability, but it has also created unintended consequences.

Because urea is significantly cheaper than other fertilisers, farmers tend to overuse nitrogen while underusing other nutrients like phosphorus and potassium. Ideally, crops require a balanced mix, often represented as an N:P:K ratio of 4:2:1. In practice, India’s ratio has drifted to around 10.9:4.1:1. Over time, this imbalance has degraded soil health and reduced fertiliser efficiency.

The numbers tell a striking story.

In 1980, one tonne of nitrogen fertiliser helped produce about 35 tonnes of foodgrain. Today, that figure has dropped to roughly 16 tonnes. Farmers are now using more fertiliser just to maintain the same output. In effect, the system is becoming less efficient even as consumption rises.

Attempts to address this through innovation have not yet delivered consistent results.

Nano-urea, for instance, was promoted as a breakthrough that could replace traditional urea with a much smaller liquid dose. But field trials have raised concerns. Some studies have reported yield declines of up to 20% in key crops like rice and wheat, along with a noticeable drop in protein content. That raises questions not just about productivity, but also about nutritional outcomes.

Meanwhile, global disruptions are making imports both scarcer and more expensive. And this puts India in a difficult position. On one hand, we need to secure enough urea to support agricultural output. On the other hand, rising prices increase the subsidy burden on the government. The result is a double squeeze, where both fiscal pressure and supply risk rise simultaneously.

To address this, the government is developing a new investment policy to expand domestic capacity.

The idea is not to directly fund fertiliser plants, but to create a stable framework with pricing guarantees for up to eight years. This reduces uncertainty for private players and encourages investment. A similar policy in 2012 helped add around 76 lakh tonnes of capacity, and the hope is to replicate that success to bridge a supply gap of nearly 100 lakh tonnes.

But even this approach has limitations.

Building new plants takes time, often several years. And unless the underlying dependence on imported gas is reduced, new capacity may still remain exposed to global price shocks. This is why alternative pathways are being explored.

One such option is coal gasification.

Instead of relying on imported natural gas, coal can be converted into synthesis gas or ‘syngas’, for short, which can then be used to produce ammonia and eventually urea. Given India’s abundant coal reserves, this offers a way to reduce import dependence. However, it comes with trade-offs in terms of efficiency and environmental impact.

Another longer-term solution lies in green urea.

This involves producing hydrogen using renewable energy and using it to manufacture ammonia. In theory, this could decouple fertiliser production from fossil fuels altogether. In practice, however, the technology is still expensive and not yet scalable for immediate needs.

Which brings us to a more fundamental question: Should India be doubling down on urea production at all?

While increasing supply may solve short-term shortages, it does not address the underlying issue of overuse. In fact, more availability at subsidised prices could worsen the imbalance in nutrient usage and further degrade soil health. The challenge, therefore, is not just about producing more urea, but about using it better.

In the short term, boosting domestic production is necessary. In a world where geopolitical tensions can disrupt supply overnight, reducing import dependence is a logical step. A well-designed policy can stabilise prices, protect farmers, and provide a buffer against external shocks.

But true resilience will require something more structural.

It will require better nutrient management, a shift toward balanced fertiliser use, and smarter subsidy design that does not encourage overconsumption of one input at the cost of others.

Because in the end, the risk is not just that India runs out of urea. It is that it becomes too dependent on it.

Until next time…

If you liked this story on the importance of urea, feel free to share this with your friends, family or even strangers on WhatsApp, LinkedIn or X.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.