The Zepto IPO explained

In today’s Finshots, we go through Zepto’s IPO filing to understand the business and make sense of what the company is really worth.

But before we dive in, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

Now onto today’s story.

The Story

A few years ago, if someone had told you that one of India's most valuable retail networks would consist of thousands of tiny warehouses hidden inside residential neighbourhoods, most people would've laughed.

Store count, shelf space, and foot traffic traditionally measured retail success in India. The winners were the companies that could build sprawling supermarkets, secure prime real estate, and persuade customers to make the trip.

Zepto flipped that model on its head.

Instead of operating massive retail outlets, it built a network of "dark stores" that most consumers never see and promised to deliver pretty much anything you wanted in ten minutes.

Three years later, this bet has turned Zepto into one of India's largest quick-commerce companies. Revenue from operations has exploded from ₹4,454 crore in FY24 to ₹22,624 crore in FY26. And the company now operates 1,139 dark stores across 66 cities, serves nearly 4.8 crore annual transacting users, and processes more than 23 lakh orders every single day.

On the surface, that sounds like the perfect startup success story. Except for one small problem.

The company lost ₹5,905 crore in FY26.

And that is precisely what makes the upcoming ₹8,000+ crore IPO so interesting.

You see, back in the day, IPOs were relatively simple to evaluate. A company generated profits, investors estimated future earnings, and a valuation emerged from that exercise.

However, Zepto doesn't fit into that framework. It has already achieved extraordinary scale, but profitability remains somewhere in the future. That forces investors to answer a far more difficult question: how do you value a business that is growing rapidly but still losing thousands of crores every year?

At first glance, the numbers are certainly unsettling.

Revenue more than doubled in FY26, but losses also widened from roughly ₹4,700 crore in FY25 to ₹5,905 crore in FY26. Free cash flow & operating cash flow, too, remained in the red.

At the same time, the company continues to spend aggressively on warehousing, delivery infrastructure, marketing, technology, and expansion into new cities.

Viewed through that lens, the business appears to be trapped in a cycle where growth simply creates larger losses.

But the reality is more nuanced because the economics is improving slightly.

As order volumes increase, fixed costs such as rent, inventory, and delivery infrastructure get spread across more transactions, making each order more profitable than the last. This is exactly what investors are seeing in Zepto's numbers today.

For context, the company's adjusted EBITDA loss (operating loss) per order improved from ₹136 to ₹79 in a single year. Cost per order declined from ₹185 to ₹151. And gross margins expanded from 12.8% to 18.6%.

Even operating cash burn improved despite revenue more than doubling.

A major reason for this improvement is something most people don't associate with a grocery delivery company: advertising.

Zepto's advertising revenue (think wheel of fortune, scratch cards, coupons, etc.) has exploded by a staggering 33 times from FY24 to more than ₹1,635 crore in FY26. The platform now works with 2,468 brand partners that pay for better visibility, sponsored listings, and access to customer insights.

This is important because it suggests Zepto's path to profitability may not come solely from delivering groceries more efficiently. It may come from monetising the attention of millions of customers who already use the platform every month.

Of course, none of this would matter if quick commerce were a niche market.

But that's the remarkable thing. It isn't.

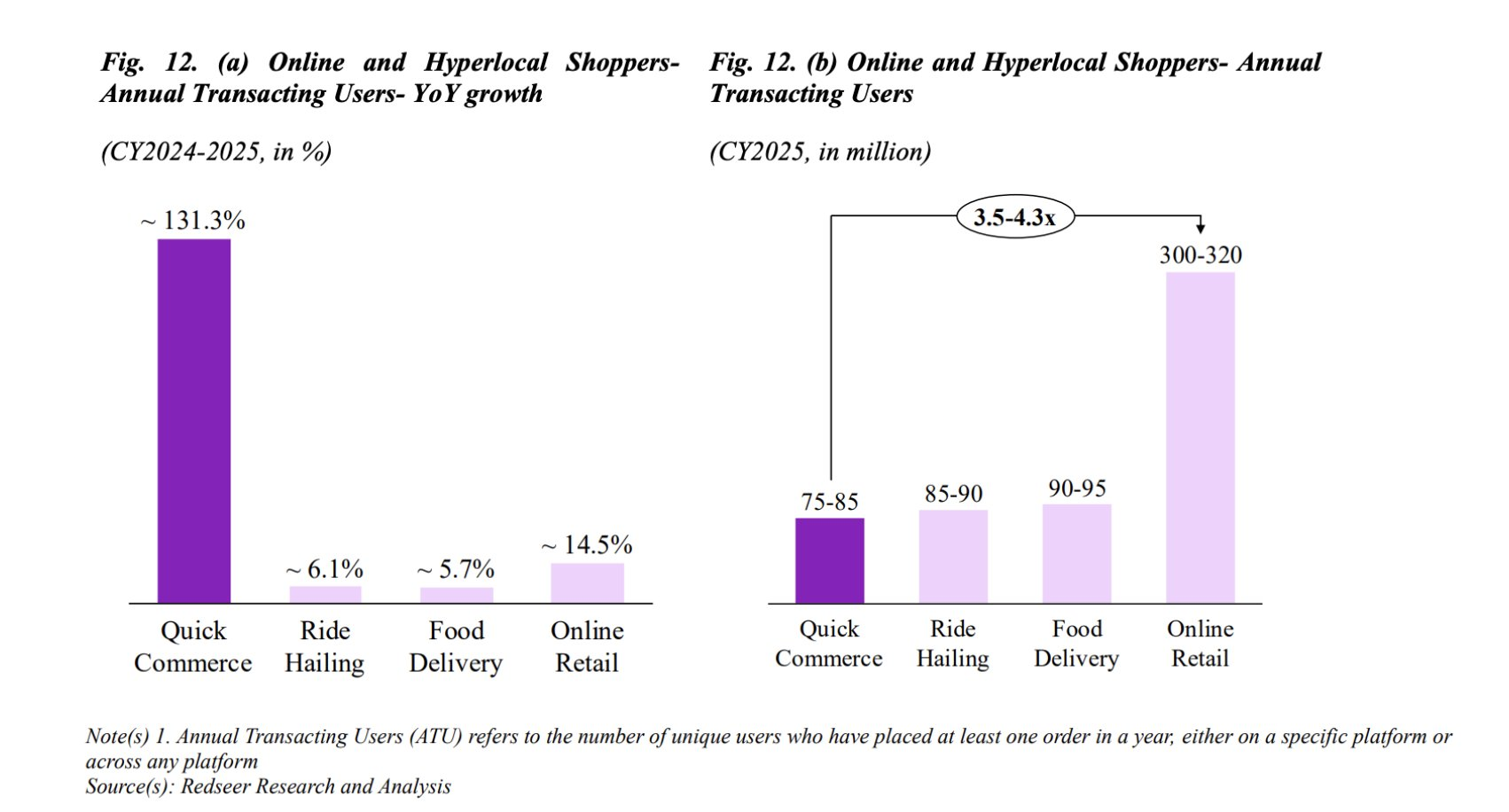

Quick commerce was the fastest-growing major consumer internet category in India between 2024 and 2025. Annual transacting users grew by roughly 131%, far outpacing ride hailing (6%), food delivery (6%), and even broader online retail (15%).

What's even more surprising is the scale it has already achieved. Around 75-85 million Indians used quick-commerce platforms in 2025. That's already approaching the user base of ride-hailing and food-delivery apps, despite the industry being far younger.

In other words, investors aren't just betting on Zepto. They're betting that quick commerce could become one of India's dominant retail habits over the next decade.

And that helps explain why companies continue pouring money into the sector despite the losses. If the market eventually grows to even a fraction of India's 300+ million online shoppers, today's losses may look very different in hindsight.

But if the industry growth story looks compelling, Zepto's financial statements tell a much more complicated story.

Despite revenue growing fivefold in two years, Zepto burned over ₹4,300 crore in free cash flow, and carries more than ₹2,717 crore in lease liabilities tied to its dark-store network. The company may not have bank debt, but its growth still requires significant capital.

And that creates a dilemma.

However, if they continue to improve their unit economics long enough, Zepto could eventually achieve something that many critics once considered impossible: a profitable quick-commerce business.

But investors are being asked to believe that outcome before it has actually materialised.

That's where the scepticism begins.

While unit economics are improving, the industry itself remains brutally competitive.

Unlike traditional retail businesses, quick-commerce platforms have very few natural barriers to entry. Customers can switch between apps within seconds. Merchants can sell across multiple platforms. Delivery partners can work for whichever company offers the best incentives.

And Zepto isn't operating in a vacuum.

Blinkit has the backing of Eternal. Instamart sits within Swiggy's ecosystem. Amazon and Flipkart have entered the category. Every major player is chasing the same urban customers, the same neighbourhoods, and often the same baskets of groceries.

The danger, therefore, is that profitability remains perpetually just over the horizon.

A company may improve its economics only to find itself forced to spend aggressively again when a competitor cuts prices, increases incentives, or expands into new markets.

This tension becomes particularly evident when we consider how Zepto plans to use the IPO proceeds.

Investors generally like IPOs in which fresh capital is used to build new products, enter new markets, or fund growth opportunities. Zepto certainly plans to do some of that. Roughly ₹1,629 crore has been earmarked for opening nearly 1,900 additional dark stores.

But another ₹1,735 crore is intended for lease rentals associated with existing dark stores. In other words, part of the IPO proceeds will effectively help fund infrastructure that is already operating today.

That isn't necessarily a bad thing, but it does highlight how capital-intensive this business model remains. Even at a massive scale, the company still requires significant amounts of external capital to sustain and expand its network.

Then there is the issue that tends to attract the most attention during any IPO: existing shareholders selling shares.

Several early investors are partially exiting through the Offer For Sale component. The company itself will not receive any proceeds from these transactions. Instead, the money goes directly to shareholders who invested years ago.

But it does create an inevitable question for public-market investors.

If some of the earliest and most informed investors are taking money off the table, how much confidence should new investors have in the valuation being offered?

And that's what makes valuation difficult. Zepto has negative earnings, negative free cash flow, and no traditional valuation anchors. Investors are effectively valuing a future version of the company, one where order density, advertising revenue, and scale eventually translate into sustainable profits.

The optimistic view is straightforward. Every major efficiency metric is moving in the right direction. Advertising revenue has grown from just ₹49 crore in FY24 to more than ₹1,635 crore in FY26, creating a high-margin revenue stream that barely existed a few years ago. Order density continues to improve. Costs per order continue to decline. If those trends persist, today's losses may simply be the cost of building a dominant retail network before competitors do.

The pessimistic view is equally compelling. After generating more than ₹22,000 crore in revenue, the company still incurred a loss of nearly ₹6,000 crore. Competition remains fierce. Customer loyalty remains fragile. And profitability remains theoretical rather than proven.

Ultimately, the Zepto IPO is not really about groceries, delivery riders, or dark stores. It is about whether investors believe scale can eventually solve the profitability problem that has haunted consumer internet businesses for years.

If they are right, Zepto could become one of the defining retail companies of the next decade.

If they are wrong, it will become another reminder that growing quickly and creating value are not always the same thing.

And that is the question investors will be asked to answer when the company finally goes public.

If you liked this story on the Zepto IPO, feel free to share this with your friends, family or even strangers on WhatsApp, LinkedIn or X.

🚨 ATTENTION: FINSHOTS FAMILY

This week we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Friday (tomorrow), 12th June at 6:30 PM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Saturday, 13th June at 10:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.