The great Indian bank locker shortage

In today’s Finshots, we tell you everything you need to know about India’s quietly brewing bank locker crisis.

Before we begin, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. We strip stories off the jargon and deliver crisp financial insights straight to your inbox. Just one mail every morning. Promise!

If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

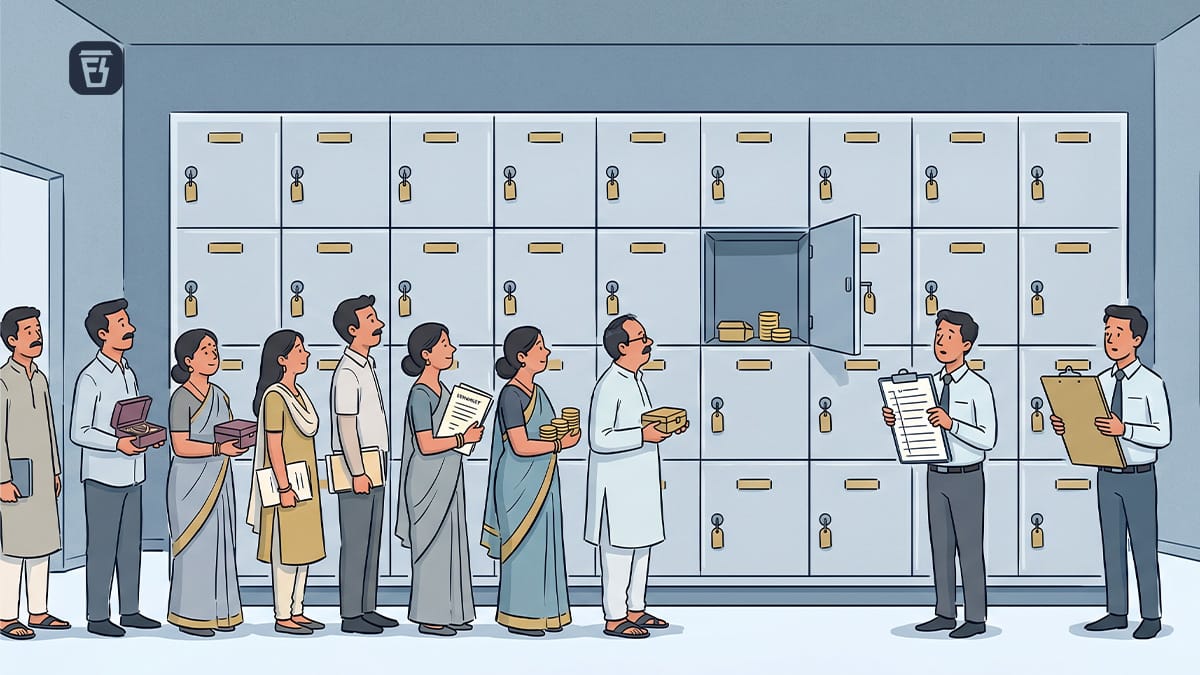

A while ago I walked into a bank branch to enquire about getting a safe deposit locker. The branch manager told me there weren’t any available and promised to call once a locker opened up.

It’s been three years and radio silence. I won’t name the bank, but let’s just say it’s one of India’s largest public sector banks.

But after recently reading about the widening demand-supply gap for bank lockers in India, I realised it probably wasn’t the bank’s fault.

Let me explain.

Today, there are only about 60 lakh bank lockers available across all public and private banks in India. But by 2030, affluent Indians alone could require nearly 6 crore lockers. That’s ten times the current supply.

And remember, that’s just affluent Indians. The actual demand could be much higher when you consider that Indian households collectively own over 25,000 tonnes of gold, which is roughly equivalent to nearly half of India’s nominal GDP or about 11% of the world’s total gold reserves.

Besides, lockers aren’t just for gold and jewellery. People use them to store wills, property deeds, savings certificates, and other important documents that feel too risky to keep at home because of theft, fire, natural calamities, or other unforeseen events. Sure, things can go wrong at banks too, but multiple layers of security make lockers a safer option for most people.

And demand is only growing. India typically adds around 33,000 millionaires every year. But in 2025 alone, that number jumped to 71,000. More wealthy individuals usually mean more valuables to protect and, naturally, a greater need for secure storage.

Which brings us to the obvious question. If demand is soaring, why aren’t banks simply adding more lockers?

After all, locker rentals generate a steady stream of recurring income for banks, right?

Well, despite this huge demand looking like an opportunity for banks to install more lockers and cash in, bank lockers are actually a terrible business.

Just think about what a locker earns a bank. Annual rent can range anywhere from ₹1,000 to ₹30,000 depending on the size and city. But those few thousand rupees hardly justify the costs banks incur.

For starters, lockers occupy valuable branch space in cities like Mumbai, Bengaluru, and Delhi, where commercial real estate costs a fortune. Then there’s the dedicated vault room, security systems, insurance, compliance costs, and trained staff who must be physically present every time a customer accesses a locker because the bank holds one key and the customer holds the other. The math simply doesn’t add up.

In fact, banks could use that same space for activities that generate far more money. For instance, a loan officer sitting there and selling loans could potentially bring in lakhs of rupees in interest income.

And it’s not like banks didn’t try to make lockers profitable. Many bundled them with other products, often requiring customers to open a fixed deposit worth five to ten years of locker rent as a “security deposit”. In a way, it was a clever way to extract additional profit from locker demand.

But the RBI eventually stepped in and capped the mandatory term deposit at just three years’ rent. And just like that, one of the few revenue levers banks had was gone.

Then came another blow. Until recently, if valuables went missing from your locker because of theft, fire, or employee fraud, banks could simply shrug their shoulders and tell you that a locker was essentially a landlord-tenant arrangement. The bank merely provided the space. It wasn’t the custodian of whatever you chose to keep inside.

And to be fair, there’s some logic to that. Banks don’t ask what you’re storing in your locker. Only the locker holder knows what’s inside.

But customers weren’t convinced. Public outrage, coupled with court rulings, eventually pushed the RBI to step in.

Which is why today, banks are liable for losses of up to 100 times the annual locker rent. So if your locker rent is ₹2,000 a year, the bank could be required to compensate you up to ₹2 lakh for contents it has never seen, valued, or separately insured. And if the actual contents are worth much less than the compensation paid, that’s a significant loss for the bank.

The end result is a classic regulatory trap. Every consumer-friendly rule, well-intentioned as it may be, makes the locker business less attractive for banks to expand.

And then there’s another problem most people don’t think about. A surprising number of lockers are technically occupied but functionally unusable. If a locker holder dies without naming a nominee, migrates, or simply stops operating the locker, banks often cannot break it open and reissue it for years. In some cases, the process can drag on for as long as seven years.

These “ghost lockers” still count as occupied in the system, but they’re unavailable to the thousands of people stuck on waiting lists hoping to get one.

All of this put together creates a massive opportunity waiting to be tapped. And funnily enough, while bank lockers aren’t particularly profitable for banks, they could be a lucrative business for private companies and startups.

Take Aurm, for instance. The startup recently raised ₹42 crore to build a round-the-clock locker services business that operates alongside traditional banks. Their idea is to simply offer lockers closer to customers such as in residential complexes, corporate campuses, and even bank branches.

That changes the economics entirely. Because unlike banks, they don’t need to acquire expensive branch real estate in prime locations. They could, say, partner with builders while real estate projects are still being developed and make secure vaults part of the community itself as an added safety feature. And because lockers are their core business, they don’t face the same dilemma banks do about whether that space could be used more profitably elsewhere.

Another thing is that these are fully automated lockers that use biometrics, facial recognition, or PIN-based access, and 24/7 surveillance. So no staff member needs to be physically present every time a customer wants to access their locker. That dramatically lowers operating costs while also allowing companies to charge a premium for round-the-clock convenience — something banks would struggle to do because customers generally expect locker rents to remain affordable.

And while all this certainly looks promising, it also makes you wonder, “What happens if a private vault operator shuts down or goes bankrupt?”

Sure, customers may be required to separately insure their valuables, but private vault companies currently don’t have an equivalent of RBI oversight or deposit insurance-backed protections that banks enjoy.

Interestingly, banks seem to be taking notes already. Last month, Axis Bank launched India’s first digital locker branch in Delhi featuring facial recognition and automated locker delivery to private access lounges. The idea is similar to private vault operators. Remove the human element, automate access, and let technology do what a branch officer once did.

The only caveat is that these solutions, for now, only serve a fairly selective section of the population, mainly urban, affluent, and tech-comfortable Indians.

So yeah, the gap in India’s safe locker market still remains. And until that changes, I probably shouldn’t expect a call from my bank anytime soon.

If this story helped you understand the Indian bank locker crisis in depth, consider sharing it with friends, family, or even strangers who may be wondering why their bank isn’t able to offer them a locker. You can share it via WhatsApp, LinkedIn, or X.

🚨 ATTENTION: FINSHOTS FAMILY

This weekend, we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 27th June at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 28th June at 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.