Why are companies rushing for buybacks before October?

In today’s Finshots, we talk about the new tax rules affecting buybacks and explain why it has led many Indian companies to wrap up their business before October 1st.

The Story

Buybacks are rather straightforward. Companies with shares listed on the stock market can buy them back from investors like you and me, if we hold these shares. In exchange for the shares, investors will receive cash, often at a price higher than the market price.

In effect, the company gets the shares back and a few investors get rich.

It’s simple, no?

But things start to get a bit complicated when we try to learn how buybacks are taxed.

In fact, it’s been a big discussion point of late. About 16 companies have announced buyback plans following the Budget 2024 announcements. And they’re doing this because there’s a small change in the tax rules.

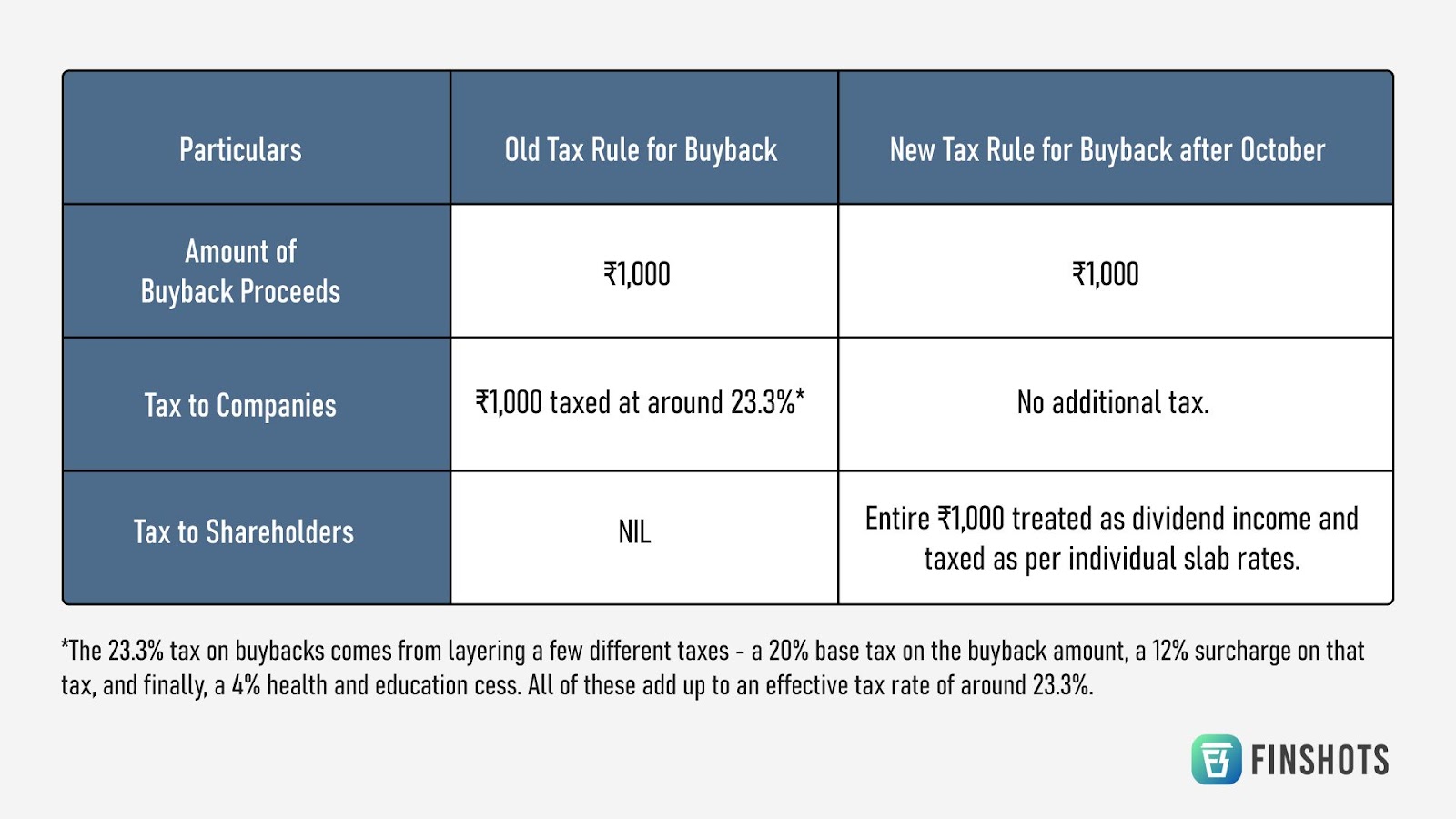

Right now, companies pay a 20% tax when they buy back their shares. But come October 1st, this tax has to be borne by shareholders or the investors and not the company. In fact, the entire proceeds received from buyback will be treated as a dividend income.

Here’s an example to make this simpler.

So, what’s the big issue here, you ask?

Well, nothing major. But there is a key consideration here. See, companies can look for a buyback for many reasons. However there are two big reasons in most cases –

- companies with excess cash can spend it to buy their shares back

- they can reward existing shareholders for their trust in the company. After all, they are the ones who’ve held company shares and given a vote of confidence by investing in it, no?

But when the tax burden is shifted to shareholders from October, it would effectively reduce the returns shareholders earn from buybacks. And that could explain why companies are keen to complete their buybacks before the new tax rule takes effect.

But wait, Finshots – If companies won’t have to pay taxes on buybacks after October, why are they being nice and announcing them now? Can’t they wait until October?

They sure can, but they don’t want to.

Because here’s the thing. The top shareholders in a company, think promoters, institutional investors and high net worth individuals, can opt for a buyback. Promoters are usually the founders or major stakeholders who play a key role in running the company. These top shareholders often fall in the tax slabs where taxes are the highest. And that changes a lot.

Here’s an example again.

So you can see how the new buyback rules change the final tax liability in two scenarios. If a high-tax bracket shareholder receives the proceeds, the total tax liability is ₹359. But for a low-tax bracket shareholder, the liability is ₹156 under the new rules.

And this amendment has a significant impact on investors and shareholders. For those in the high tax bracket, the liability jumps from ₹0 to ₹359, while for those in the low bracket, it increases from ₹0 to ₹156. Sure, the investor’s liability rises in both cases. But for promoters or top shareholders, it makes more sense for the company to pay ₹233 before October, rather than them paying ₹359 after October.

So yeah, in order to avoid higher taxes for their most valued shareholders including promoters and top shareholders, and bring in more shareholder value when they can, companies are trying all they can to complete their buybacks before October.

Also, this doesn’t necessarily mean that buybacks will lose their charm after October. Because the new tax amendment in the Budget actually offers a bit of relief for investors. It says that the cost of acquiring shares (the amount an investor initially pays to purchase them) in a buyback can be treated as a capital loss, which you can offset against any capital gains, and even carry forward for up to eight years.

Let’s say, for instance, you’re participating in a buyback and you’d bought those shares for ₹1,00,000. This cost would be considered a loss. You can then adjust it against your other capital gains to lower your taxable income. For example, if you have a capital gain of ₹80,000 in the same year, you won’t pay any tax on that gain since it’s offset by the ₹1,00,000 capital loss from the buyback. Plus, the remaining ₹20,000 loss can be carried forward and used to offset future gains for up to eight years until it’s fully utilised.

This flexibility in handling capital losses could make buybacks still quite appealing, despite the new tax rules.

And hey, this new rule would also encourage companies pursuing buybacks only when they feel that their shares are genuinely undervalued. Because when a company’s shares are undervalued, a buyback can boost their value. By buying back shares, the company shrinks the total number of shares in the market, and in turn the remaining shares suddenly turn more valuable. It’s basic economics. When the supply of something drops, the price tends to go up. As simple as that!

And the bottom line here is that companies will look at buybacks as a strategic move to invest in their own undervalued shares, ensuring that they’re making a genuine investment rather than just seeking tax benefits.

So yeah, that’s why companies are excited to roll out their buybacks before October. We’ll have to wait and watch how the buyback party goes on after that and how excited the shareholders will be to attend them.

Until then…

Don't forget to share this story on WhatsApp, LinkedIn and X.

Correction: An earlier version of this story incorrectly stated that the change in buyback tax rules benefits investors in the 15% income tax bracket and penalises those in the topmost income tax bracket. We’ve now updated the table and example to accurately reflect the impact. We regret the oversight.

📢 Ready to simplify business and finance even further? Dive into Finshots TV, our YouTube channel, where we break down the latest in business and finance into easy-to-understand videos — just like our newsletter, but with visuals! Don’t miss out. Click 👉🏽 here to hit that subscribe button and join the Finshots community today!

🚨Term Life Insurance Prices are About to INCREASE!

A prominent insurer is set to raise their term insurance rates in the next few weeks. This means if you don’t secure a term plan now, your premiums could significantly go up!

Here’s why this matters: When you purchase a term life insurance policy, you pay a premium or a small fee each year to protect against financial risks. In the unfortunate event of your passing, the insurance company pays out a substantial sum to your family or loved ones.

The best part? By buying early, you can lock in your premiums, ensuring they're not affected by any future rate hikes.

If you've been considering a term plan, now is the perfect time to act. To assist you in the process, our advisory team at Ditto is here to help. Click on the link here to book a FREE call with our IRDAI-certified advisors.