Who pays for climate change?

In today’s Finshots, we explain reparations — one of the most important items to feature on the agenda at the United Nations Climate Change Conference.

The Story

In 1991, the tiny island nation of Vanuatu raised an important question — who pays for climate change?

While everyone else at the time still kept debating about the true cause of climate change, this country could see the writing on the wall. They could see the water levels rise across the Pacific ocean. They could see their livelihood withering away slowly. And they could see that it wasn’t their fault at all. After all, they contributed just 0.0016% of the world’s greenhouse gas emissions. It was an issue precipitated by all the rich countries that guzzle fossil fuels.

So on behalf of multiple similar island nations across the world, Vanuatu wanted answers.

And now, 30 years later, it looks like the rich countries are finally willing to admit responsibility.

How? you ask.

See, this time every year, world leaders gather to discuss climate change. It’s the most important climate networking event and it’s called the COP or the Conference of Parties.

Sidebar: The COP27 is happening in Sharm-El-Sheikh this year. The location is quite fitting since the Egyptian coast houses one of the most beautiful coral reefs in the world. As climate change has warmed ocean waters, these biodiversity hotspots have been facing an existential crisis.

And for the first time ever, one of the official items on COP27’s agenda is ‘loss and damage’ financing or reparations.

What does this mean?

Well, the rich countries are putting their hands up and saying, “Yes, we’re liable (in a way) for the emissions over decades. We know the harm it’s done to many countries that may not have had a role to play in this. And we will figure out how to pay for damages.”

Just look at the data between 1751 and 2017 — a whopping 47% of the CO2 emissions came from the US, EU and the UK. Africa and South America put together only accounted for 6%!

And acknowledging this injustice in COP27 is a big deal because each time talks of compensation have cropped up in the past, rich countries have found ways to stonewall it. They’ve brushed it off.

But finally, they’re willing to acknowledge it.

However, there is a problem.

The idea of reparation is great in principle. But in reality, it poses a few challenges. While you could try and extract some form of compensation for the historical wrongs committed by a small group of nations, it also begs the question — how do you decide who pays and how much?

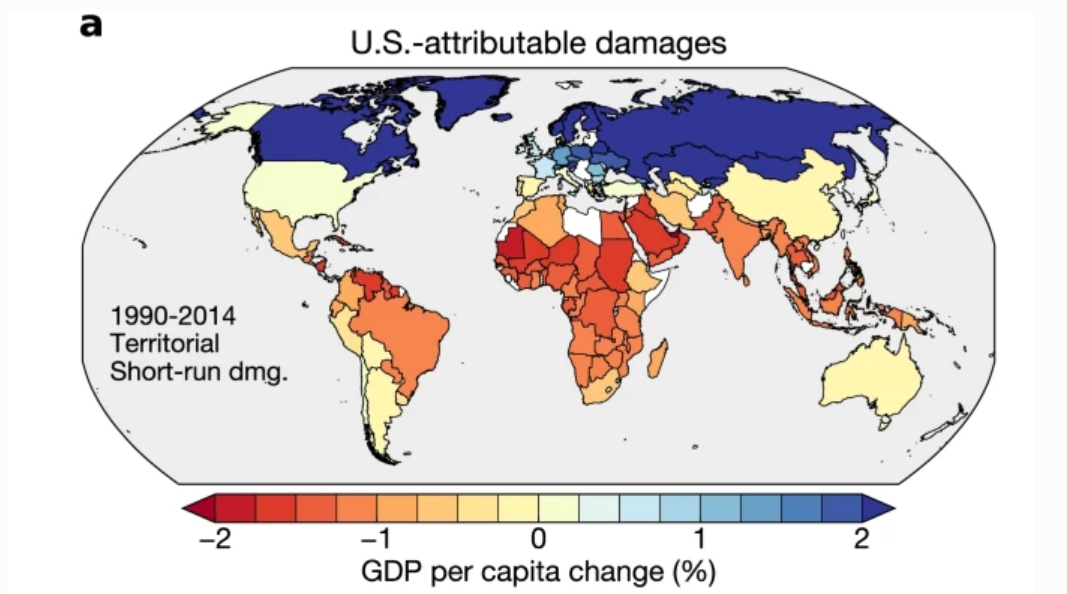

The easiest way to do this is to perhaps look at the available literature. And one piece of insight comes from researchers working out of Dartmouth College. They looked at data from 143 countries, analyzed greenhouse gas emissions, evaluated country-to-country interactions and pored over a large database containing 11 trillion values(!) and found some very interesting things.

Take the US for instance. Its emissions hurt its neighbour Mexico and the country lost $79 billion of its GDP between 1990 and 2014.

How?

Well, warmer weather can hurt agricultural yields if the crops aren’t attuned to the fluctuations in temperatures. It can also cause heat-related stress, impact worker productivity, and hinder industrial activity. It can be a real drag on the economic output.

So you could argue that the US owes Mexico $79 billion in climate change reparations.

But, here's the flip side.

You see, emissions from the US have also helped a few countries. Such as Canada which has seen a bump up in its economic output due to the warmer climate. People are more productive when it isn’t freezing out there.

So, if we assume there’s a “reparation” fund, does it mean the US will get a ‘discount’ on what it owes other vulnerable countries? Or could the onus fall on Canada to pay not just for its own emissions but also set aside the gains ($246 billion) from US emissions?

It’s complicated.

Source: Springer

And then there’s the matter of India.

You see, India is estimated to have lost $255 billion due to emissions from the US.

But here’s the thing…as we’ve stepped up development initiatives across the country, we have become one of the top 5 global emitters. And many countries have suffered because of this. In fact, the total losses exceed $500 billion.

So does that mean India is also going to have to cough up reparations of some sort?

We don’t know.

Because if we actually break down the emissions on a per capita basis, we can’t really label India as a big polluter. While the global average is 6.3 tonnes of CO2 equivalent (tCO2e), India’s is only 2.4 tCO2e.

So maybe that should count for something?

And then there’s the matter of timelines.

The study is restricted to a brief period in human history — 1990 to 2014. But if we rewind the clock, you’ll see that India’s contribution to climate change may not amount to a lot. And if you go back a few centuries you’ll see even bigger issues cropping up. Think about the colonial enterprise.

As Dorothy Guerrero, head of policy at Global Justice Now says, “Back in 2008, I visited Uttar Pradesh in India and we had this meeting with forest workers. And they said that many of the forests in Uttar Pradesh were cut to provide the wood for the trains in Britain.”

Or look at the Western Himalayas. In the 1800s, the British chopped down large swathes of oak and deodar forests. They replaced the wildfire-resistant forests with pine plantations to meet their need for resin. But the problem? Almost every summer, the dry pine needles lead to massive wildfires in the Indian Himalayas. It destroys the environment and avian habitat.

So, how do you account for all that damage from the past?

Well, it’s hard. And it’s foolhardy to think that the talk about reparations is final. In fact, the official agenda at COP is only restricted to recognising the need for reparations. The meaty discussion surrounding the actual financials will probably have to wait.

Unfortunately, for countries like Vanuatu, it can’t come sooner — the island nation suffers losses to the tune of $48 million per year (~7% of its GDP) due to the adverse effects of climate change.

And as we wrote last year,

46 of the least-developed countries in the world don’t have enough money to protect themselves against the impact of climate change. Between 2014–18, they only received US$5.9 billion. When in fact they need at least US$40 billion a year to adapt to climate change.

The world needs that money. Fast.

Will it get it?

We don’t know.

Until then…

Don't forget to share this article on WhatsApp, LinkedIn and Twitter

Ditto Insights: Should you buy insurance + pension products?

There are numerous investment products that claim to safeguard your golden years and provide the best retirement solution.

But what if you could get stable returns alongside life protection- all in one product? Enter: insurance-cum-pension plans.

The premise is simple- get both life insurance and investment benefits wrapped in one product. They usually work in two phases: accumulation and pension.

Accumulation occurs when you pay a premium and contribute to an investment, while a pension is initiated when you begin receiving a steady stream of income from the sum accumulated. But should you invest in these policies?

Well, here are some factors you should know before buying into one:

1) Life cover: The insurance payout of this type of product is usually much lower than a regular term insurance plan. So it doesn’t really protect your life if something happens.

2) Additional charges: When you subscribe to such plans, the insurer levies various charges. Think- administrative charges, mortality charges etc. When these charges are added together, they can hamper your returns, so it’s always better to park your money in better financial instruments.

Ditto’s Advice: Ideally, consider keeping your insurance and investments separate so you can maximise the benefits. And hey, if you require personalised consultation on the best term insurance plans, reach out to our advisors at Ditto.

1. Go to Ditto’s website — Link here

2. Click on “Book a FREE call”

3. Select Term Insurance

4. Choose the date & time as per your convenience and RELAX!

And our advisors will take it from there!