What’s cooking with Gold ETFs in India?

In today’s Finshots, we explain why Indians are chasing gold exchange traded funds.

But before we begin, here’s a question: Have you ever read Finshots and thought, ‘Wow, someone actually made all this complicated stuff make sense?’

Well, that someone could now be you.

WE’RE HIRING!

If you love breaking down complex ideas, crafting stories that stick, or know your way around marketing, we want to talk! We’re hiring writers, SEO specialists, video editors, and more! Our team made Finshots what it is today. And now, we need more curious minds to help us keep pushing boundaries and creating things people love! Interested? Head over to our Careers page.

Now, on to today’s story.

The Story

You got your salary recently and are looking to invest part of it to earn good returns. The stock market however feels a little too risky right now. So, you turn to gold. It’s shiny, it’s stable and it’s been a symbol of wealth for centuries. And you soon realise there are just so many ways to invest in gold. Physical gold, Sovereign Gold Bonds (SGBs), gold funds… and then there are Gold ETFs.

ETFs, you ask?

Imagine owning gold without needing a vault at home. Gold ETFs (Exchange Traded Funds) make it possible by slicing gold bars into tiny digital units that you can buy and sell like shares on stock exchanges. Each unit represents a fraction of a gram of gold, stored securely in your demat account. It’s hassle-free gold ownership — simple, convenient and accessible. Fund houses in India purchase physical gold (99.5% purity), store it in empanelled bullion vaults, and create ETFs by dividing it into units. These units’ prices trade on exchanges like BSE and NSE and move with market gold rates, making them a smart way to track the metal’s value. And you get to invest in these units just as you do for your mutual funds.

And Indians are loving it.

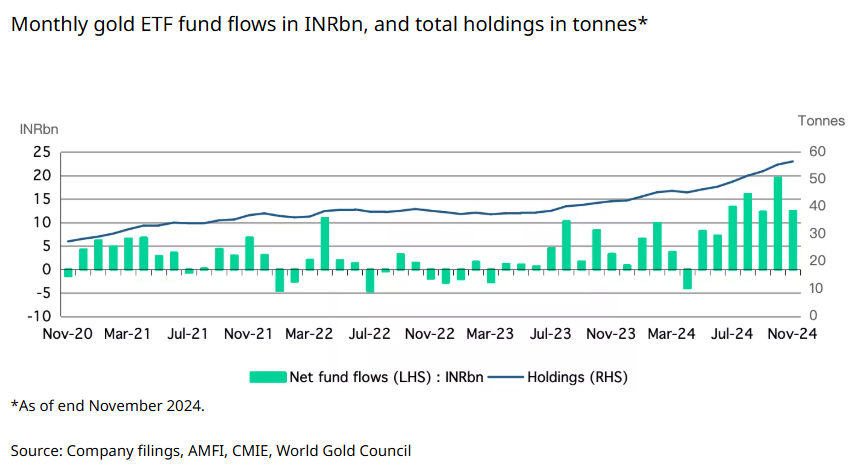

To put things in perspective, in just four years, the physical gold held by these funds has almost doubled from 27 tonnes to a whopping 55 tonnes by October 2024. And it’s not just the weight that’s grown, the money pouring into these ETFs has skyrocketed too.

Take the past 21 months, for instance. Domestic Gold ETFs attracted a whopping ₹12,450 crores in net inflows. To top it off, the period from November 2023 to November 2024 saw investments jump nearly fourfold from nearly ₹330 crores to ₹1,250 crores.

Trading volumes tell a similar story too. In 2024, Gold ETF volumes on Indian markets soared to about ₹26,500 crores, more than doubling from 2023.

This simply means that with gold delivering a solid 13 to 14% compounded annual returns (CAGR) in rupee terms over the last five years, even a ₹100 investment five years ago would have grown to around ₹185, making it a rewarding investment.

And this begs the question ― what’s driving this gilded migration?

For starters, the 2024 Union Budget introduced a tax-friendly nudge. It slashed the holding period from 36 months to just 12 months. This means that earlier, you had to hold onto your Gold ETFs for 3 years to qualify for long-term capital gains, which were taxed at slab rates based on your income. But now if you hold onto your Gold ETFs for over a year, your gains are taxed at a flat 12.5% instead of being tied to your income slab. This clarity and tax efficiency have made ETFs a friendlier investment option.

Add to this the scarcity of new SGB issues are channeling investors to explore alternatives. Meanwhile, multi-asset funds in India have ramped up their allocation to Gold ETFs, reaching ₹6,400 crores by November 2024.

And lastly, gold’s allure has also grown globally due to market uncertainties and expectations of lower interest rates.

So yeah, all those reasons seem to be driving India’s growing love for gold ETFs lately.

But does that make them all goody-goody?

Not entirely we’d say. Because gold ETFs have their own set of quirks.

One of their less-discussed challenges is liquidity. Imagine owning a rare, expensive book that a few collectors want to buy. But if you wanted to sell it quickly, you’d struggle without lowering the price. Similarly, some Gold ETFs don’t trade as often as popular stocks. So, selling large amounts quickly could impact your selling price in secondary markets (like the exchanges) or take longer to find buyers at your desired price. This is especially true for ETFs that aren’t widely held or as well-known in the market.

Then there’s tracking error — the gap between the ETF’s performance and gold prices. Imagine running a race with your friend timing you, but they’re always a second behind. Similarly, while Gold ETFs aim to match gold prices, they often fall short due to market inefficiencies or even delays in replicating the actual spot price of gold. For instance, if gold prices rise by 10% annually, but your ETF delivers only 9.5%, that 0.5% tracking error eats into your returns. Over five years, a ₹5,00,000 investment could grow to ₹7,71,500 instead of ₹8,05,000, losing over ₹30,000 to tracking error alone.

Speaking of costs, Gold ETFs also come with an expense ratio, brokerage fees and transaction costs. Sure, physical gold has its costs too — making charges and GST, for instance. And yes, costs associated with ETFs are usually cheaper than those of buying, storing or insuring physical gold. But then, those costs with physical gold are mostly one-time expenses. While ETF fees recur annually, quietly nibbling away at returns.

And let’s not forget, gold itself doesn’t generate income. Unlike stocks or bonds, it offers no dividends or interest (unless you’re investing in SGBs). Its value depends entirely on market perception and macroeconomic conditions. So, overloading your portfolio with Gold ETFs could mean missing out on potentially higher returns from equities or other asset classes.

So then, how do we solve this debate?

Well, think of gold ETFs as a tool — not a hero or villain – in your investment toolkit. Their value lies in how you use them. Jumping in blindly or over-allocating could expose you to risks. And dismissing them entirely means missing out on their unique benefits.

The key? Balance and strategy.

You see, gold has its cycles. It can shine bright for years but also lose its lustre in downturns, and we’ve seen this story in the past.

And that’s where diversification and allocation could help. So, pull out an excel sheet and take stock. What percentage of your investments is in gold overall? How much is in gold ETFs? And how does it all stack up against equities, bonds or other assets? If gold is tipping the scales, considering your risk tolerance and return expectations, it’s time to recalibrate. By doing this, you can decide how much you’ll allocate to gold each year — not too much, not too little, but just right.

Because while gold glitters, it’s the smart strategy that truly shines.

Until then…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

📢Finshots has a new WhatsApp Channel! If you want the sharpest analysis of all financial news without the jargon, Finshots is the place to be! Click here to join.