The SBI Funds Management IPO

In today’s Finshots, we break down the SBI Funds Management IPO, which is open for subscription from today (July 14th) until July 16th.

But here’s a quick disclaimer before we begin. Please don’t treat any part of this story as investment advice, and as always, make investment decisions only after conducting your own due diligence.

Also, we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 18th July at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 19th July at 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.

👉🏽 Click here to register while seats last.

Now onto today’s story.

The Story

Millions of Indians today own SBI Mutual Fund schemes. Some through SIPs. Others through a lump sum they parked years ago and half-forgot about. And many more through the retirement and institutional money that SBI Funds Management quietly manages behind the scenes.

But here’s a funny thing. While you’ve been investing through SBI Mutual Fund all these years, you’ve never actually been able to invest in the company managing those investments.

Soon, that’s about to change.

SBI Funds Management, the company that runs India’s largest mutual fund, is finally heading to the markets.

And it’s no small fish. Roughly one in every six rupees, or 15.3% of the market share in Indian mutual funds, is held by this single company. That’s more than HDFC, ICICI, or anyone else. On paper, it’s about as good a business as you’ll find: 70% profit margins, the lowest costs in the industry, and 16 million SIPs quietly topping it up every month.

What makes it even more interesting is that SBI isn’t raising a single rupee from this IPO.

There are no fresh shares here. Instead, the company’s two owners, State Bank of India (SBI) and a French asset manager called Amundi, are selling a chunk of their existing stake. SBI, which owns about 62% of the company today, is offloading the bulk of it. Amundi is selling the rest.

Now, this isn’t a red flag. A lot of excellent businesses list this way, especially ones that don’t actually need money to grow. And SBI Funds Management is exactly that kind of business.

But it does change the question you should ask. With no growth story riding on your money, you’re simply buying the business as it stands today. So only two things matter: how good is it, and is the price fair?

Let’s take those one at a time.

First, the business.

Running a mutual fund is one of the most profitable operations in finance. There’s no inventory. No factories. No meaningful debt. You gather people’s money into schemes, charge a small annual fee, and let compounding do the heavy lifting.

The magic is in the fixed costs. Whether SBI manages ₹1 lakh crore or ₹12 lakh crore, it pays roughly the same to fund managers, the same to research teams, and the same for compliance. So as the pile grows, those costs spread thinner and profits balloon.

And SBI’s pile is the biggest in the country. About ₹12.5 lakh crore across its schemes, which is where that “one in six rupees” comes from. That scale means its operating costs are just 0.08% of assets — the lowest among India’s ten biggest fund houses, with everyone else at 0.10% to 0.25%.

Put it together, and the numbers look almost too clean. Last year, SBI Funds Management earned ₹4,389 crore in revenue and kept ₹3,067 crore as profit — a margin of roughly 70%. A couple of years ago that profit was ₹2,073 crore. So you can see how the numbers have climbed largely by sitting still and letting India’s SIP boom flow in.

But every beautiful business has a catch. And this one has two.

The first: the world is drifting towards cheaper funds.

For years, the heart of SBI’s business has been actively managed funds. They’re the ones where a fund manager and their team pick stocks, try to beat the market, and charge you a fee of anywhere between 0.75% and 2.43% a year.

But more and more Indians are moving money into passive funds. For example, index funds and ETFs that don’t try to beat the market. They simply mirror it. So you don’t need a star fund manager or a research army. And most importantly these come with far lower fees. For context, some passive funds charge as little as 0.04% a year.

For investors, this is great news. But for SBI Funds, it’s complicated.

Because SBI is also India’s largest passive manager, with nearly 28% of that market, it’s not being left behind. But that’s the problem. Every rupee that moves from an active fund charging 2% to a passive one charging 0.04% now earns SBI a fraction of what it used to.

Passives already make up about a third of SBI’s mutual fund assets. And as that share grows, the average fee on every rupee it manages keeps going down. The trade-off is more money but thinner margins.

The second catch is that the regulator wants your fees lower too.

From April 2026, SEBI rolled out new mutual fund rules with a simple idea: bring costs down for ordinary investors. That’s great news if you’re investing. Less great if you’re the company whose entire revenue is that fee. SBI has openly admitted the rules will squeeze its yields and force it to, in its own words, fundamentally restructure its cost base.

So step back, and you see the real tension. SBI Funds Management is a magnificent cash machine. But its price per unit is slowly being driven down by its own customers drifting to cheaper products and by a regulator nudging fees lower.

But none of this is fatal. India’s mutual fund industry is still young, still growing fast, and SBI is better placed than almost anyone to ride that wave. The sheer volume of new money pouring in can paper over shrinking margins for a long time.

But it does mean the business isn’t quite the effortless money-printer it first appears to be, which brings us to the last, trickiest part.

The price.

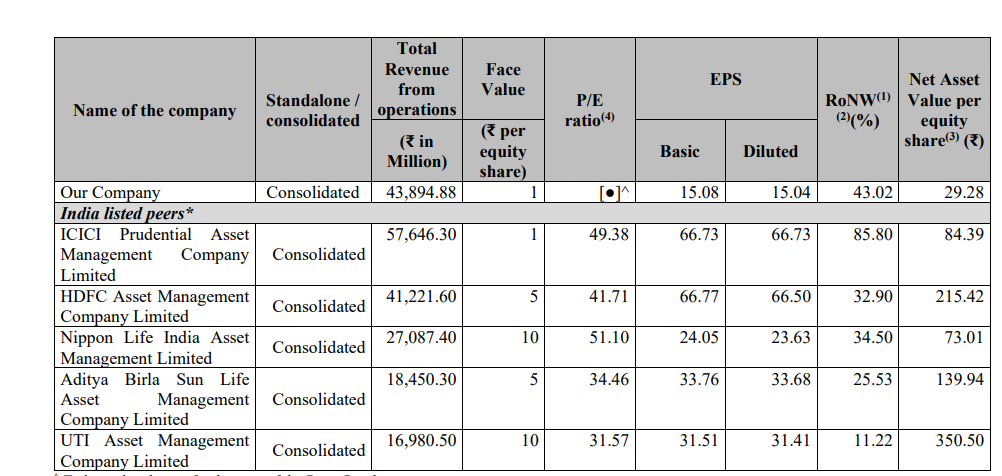

SBI has priced its shares between ₹545 and ₹574. At the upper band, that puts a value of about ₹1.17 lakh crore on the whole company. That is more than any asset manager in India has ever been worth.

And at ₹574, you’re paying about ₹36 to ₹38 per ₹1 of profit it made last year. And compared to its listed rivals, that’s not expensive at all. HDFC’s fund arm trades at around ₹42, ICICI’s at ₹49, and Nippon’s at ₹51. Only the smaller players like Aditya Birla and UTI are cheaper, at about ₹34 and ₹32 respectively.

In other words, the biggest, most profitable fund house in the country is asking for a fairly moderate price.

But don’t mistake “reasonable” for “risk-free”.

Remember the two catches. That premium is really the market paying up for SBI’s exceptional profit margins. And those are exactly the margins that passives and the new fee rules are slowly pressing on. So you’d be paying a leader’s price for those profits, right as the squeeze on them begins.

So here’s a simpler way to think about it. Betting on this IPO isn’t really a bet on SBI’s fund managers. It’s a bet on you, your neighbour, and the millions of Indians who now start an SIP the way the previous generation opened a fixed deposit.

Every new SIP adds a little water to the tide.

But here’s one final thought. This IPO isn’t about whether Indians will invest more. That, as we already know, is already happening. Rather, it might be about whether scale can keep winning when fees keep shrinking.

Until next time…

Liked this story? Share it with someone who's curious how one of India's biggest mutual fund companies makes money, over WhatsApp, LinkedIn and X.