Wrapup: Why the government is unhappy with Hindustan Zinc

Before we get to today's story, here's a quick wrapup. On Monday we talked about e-pharmacies. On Tuesday we talked about forever chemicals. On Wednesday we talked about transfer pricing. On Thursday we talked about Section 230 and finally we talked about the death of quick commerce

In this week's Finshots Markets, we explain why a decision by Hindustan Zinc, a former Public Sector Enterprise, to buy mines in Africa is annoying the Indian government

The Story

If ever there was a posterchild of divestment, it’s Hindustan Zinc.

The metals and mining company began life as a public sector entity in 1966 but it didn’t do too well under government leadership. It racked up losses over the years. And by August 2000, the NDA government decided that the government didn’t really need to be in this sort of business. So they set the wheels in motion and within a couple of years, sold 26% of their shares to Sterlite Industries (owned by Vedanta). By November 2003, the government sold another 19% of their stake. And netted around ₹770 crores.

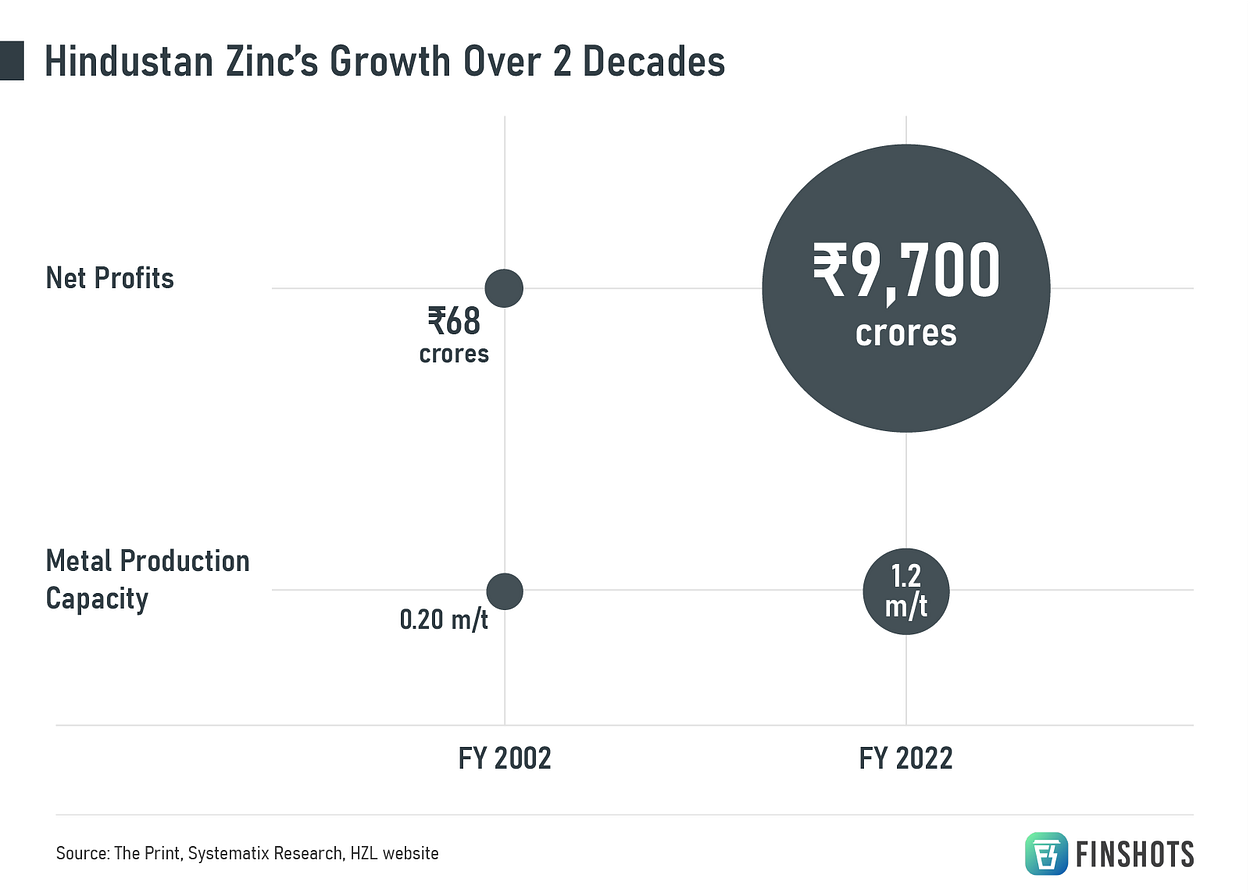

Since then, Hindustan Zinc’s rise has been swift. It’s now the second-largest miner of zinc-lead in the world. It has even broken into the top 10 list of the world’s biggest silver producers. The net profits ballooned from ₹68 crores in FY 2002 to ₹9,700 crores in FY 2022. And its metal production capacity soared from 0.20 million tonnes to over 1.2 million tonnes during the same period.

Now we won’t get into a blow-by-blow account of how it all transpired. That’s a story for another day. But let’s just say that the decision to sell the majority stake to a private entity meant that profits took centre stage. The know-how to run a metals and mining business came in. And the exploration tech for mines improved. Internal power plants were set up to reduce costs. Also, the demand for zinc flourished thanks to a boom in China. Especially since zinc finds heavy use in the construction and automobile industry — to prevent iron and steel from rusting.

And this brings us to today.

See, the government of India still holds a 29.5% stake in Hindustan Zinc. And it wants to sell it now. It wants to divest its holdings and get out of the business completely. But it’s not happy with what Hindustan Zinc has been up to.

Let us explain.

It all starts with Vedanta, the company which owns 65% of Hindustan Zinc. This was the entity the government sold the stake to two decades ago. The thing is, Vedanta is trying to offload some of its mines in Africa. Why, you ask?

Debt!

See, Vedanta has a boatload of debt — $7.7 billion of it (after adjusting for whatever cash it also holds). And ratings agencies aren’t happy. S&P Global Ratings raised questions about how financially healthy the company was. And said that Vedanta really didn’t have any other option but to sell its zinc assets in Africa to raise cash. If not, S&P would have to downgrade Vedanta’s debt rating. And that’ll affect the rate at which it can borrow money in the future.

Vedanta knew there was no way out. So instead of selling these precious mines to some outsider, it thought it best to keep it within the family.

Enter Hindustan Zinc — Vedanta’s Indian subsidiary that plans to front the money and buy out these mines.

And on the face of it, it’s a sweet deal. Vedanta gets the cash. And Hindustan Zinc will suddenly have full access to massive zinc resources in South Africa — the Black Mountain Mine and Gamsburg Mine. Put together, the zinc reserves and resources (R&R) will amount to a massive 35 million tonnes. With mining activity expected to increase exponentially over the next few years, it’ll catapult Hindustan Zinc to the top of the charts. It’ll become the largest zinc mining company in the world.

That’s a pretty big deal for a company that was a government entity just about 25 years ago, no?

With this level of scale, it’ll also drop the cost of production by at least 20%.

But…the problem is that the mines aren’t cheap. They’re going to cost nearly $3 billion. That’s cash that Hindustan Zinc does not have. It only has around $2 billion in hand. So it’ll need to borrow money. And suddenly it’ll go from being a cash-rich company to one in debt.

Investors don’t like it when debt shoots up. Even if it’s for the long-term good of the company.

Then there’s the big question mark over the valuation of this acquisition — Is it too expensive?

As per the folks at Systematix Research, if you value Hindustan Zinc based on R&R/ton metric, you’ll see that it trades at around $633/t. On the other hand, it’s paying $851/t for Vedanta’s Zinc International assets. That’s a 35% premium.

Sure, you could argue that a control premium pops up in deals like these. Which is simply an amount that’s paid in addition to the fair value of shares. A company making an acquisition is willing to shell out this something extra because they’re getting a controlling seat at the table. They can dictate how to run day-to-day operations and even control strategy.

But investors don’t like expensive acquisitions either.

When the announcement was made in January, they quickly rushed for the exits. The stock dropped by 10%. And that means the valuation for Hindustan Zinc falls too.

The end result for the Indian government?

When they’re ready to sell some shares as part of the divestment programme, they’ll get a lower price. They won’t be able to squeeze everything out of it. And no one likes to make less money, right?

In fact, before the news about the deal broke, the government could have netted a massive ₹46,000 crores by selling its stake of 29.5%. But now, after the fall in stock price, it might get only ₹39,000 crores. That’s quite a big difference at the end of the day when it’s trying hard to meet its divestment target for this financial year.

The government is feeling so much angst that it’s even considering legal options. It wants to do everything it can to block the deal. It’s saying, “Look, we’re concerned about the valuation. It seems like a bit much. And you’re spending so much which is insane If you want the assets, you’ll need to think of another way out. A cashless method.”

But will Hindustan Zinc and Vedanta have to listen to the government?

They have to. See, Hindustan Zinc is buying the mines off of Vedanta. It’s a related-party transaction. That means, Hindustan Zinc needs the approval of a majority of its smaller shareholders too. It’s a rule in place just to prevent nefarious plans that a promoter might have to siphon away resources. It’s to protect the small shareholder. And in this case, that role is played by the government of India.

So yeah, that’s the only way out now. Please the government and maybe, the mines will come into Hindustan Zinc’s fold. And Vedanta can retire some of its debt.

We’ll have to see what happens now.

Until then…

Don't forget to share this article on WhatsApp, LinkedIn and Twitter

Weekly Quiz

Want your own exclusive Finshots merch? All you need to do is answer 5 easy questions in our weekly quiz!

Here's how it works:

➡️ Every Monday to Friday, we'll send you a new story on business and finance. Just like we always do.

➡️ Make sure you keep up with the daily stories. Because at the end of each week, we'll compile one question from each of these stories and create a quiz.

➡️ All you have to do is fill out a Google form, answer the questions correctly and you stand a chance to win some amazing prizes (Imagine how cool it would be to have your own Finshots hoodie!)

So don’t forget to keep an eye out for our weekly wrapup every Saturday. And you might be the lucky winner of awesome Finshots merch.

See you next Saturday for Quiz #1!

Team Finshots ❤️