Finshots Cracks Crypto #2: What's Money?! From Barter to Bitcoin🤯

In the first part of Finshots Cracks Crypto, we went over the basics of blockchain and Bitcoin.

Now it’s time to take a step back. In this second story, we tell you about the evolution of money itself. From barter systems and gold to paper money, we’ll see how societies have redefined value and trust over centuries. And where Bitcoin fits into this fascinating journey.

Ready to roll?

The Story

I was a kid when I first realised that money was more than coins or paper—it was an idea, a construct.

So it was the late 90s, and ATMs had just begun to pop up across India. For a kid like me, though, money was only as real as the crumpled notes in my mom’s purse. That illusion shattered one day at a park when I wanted an ice cream. My mom checked her wallet and came up empty. But then she pulled out a plastic card and said, “I’ve got your back.” We walked to an ATM, and what I saw next was pure magic…a machine that spat out cash just because my mom punched in a few numbers. "Is there a secret tunnel to the bank?", my mind raced. She smiled and explained the basics.

But the questions wouldn’t stop swirling in my head: “How does this money thing really work? If it’s so easy to get money, why do we not have more of it? And why can’t everyone have as much as they want?” My mom, amused by my curiosity, told me, “Keep those questions alive, and one day you’ll understand.” Then she dropped a word that stuck with me: “inflation” (or “mehengai” as she called it). It was her way of saying, “There’s more to this money game than meets the eye.”

So I kept digging. With every question, every new fact, the rabbit hole of money’s mysteries grew deeper. It wasn’t just coins, notes, or ATMs anymore. It was about history, human behaviour, and how societies agreed to trust abstract ideas that held the world together.

In high school, our economics teacher told us about a fascinating experiment with primates and their introduction to the concept of money. So, chimpanzees, in various studies, were taught to use specific stones as a currency to trade for bananas. And what happened next? They quickly learned to game the system. Some invented “armed robbery”, stealing stones from weaker chimps to secure their bananas. Others figured out that they could exchange favours, including sexual ones, for stones. It was both amusing and unsettling to see how quickly they mimicked human behaviour, using money as a tool for power and exchange.

The point here?

Money isn’t just coins or bills but an abstract form of communication, a way for humans to agree on and exchange value. Think of it as the glue that holds civilisations together. And that’s probably why money is fundamentally a social construct — because it relies on shared trust. At its most basic level, money helps us exchange things we agree have equal worth, creating the social bonds that make trade, cooperation, and even societies possible.

So it’s no surprise that when I think about Bitcoin today, I’m amazed at how far we’ve come in redefining money.

But to understand its significance, we need to rewind to where it all began. To the very roots of value, trust and exchange. Let’s jump in…

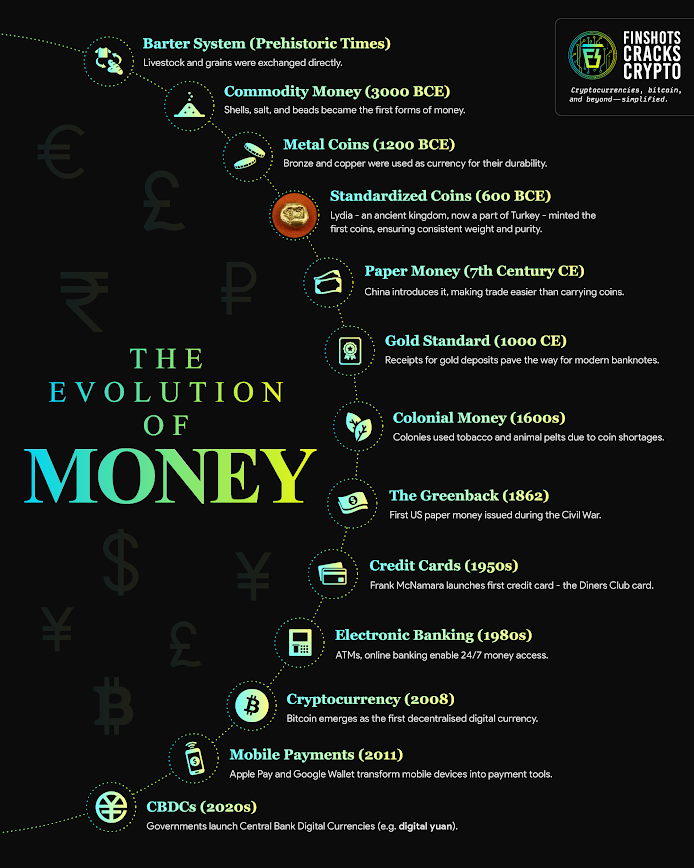

Barter

Now money, in its earliest form, was about survival. Imagine a time when barter was the way to trade. Apples for fish, wheat for milk. On paper, it sounds simple, but it had a glaring flaw. Economists call it the "double coincidence of wants”—you had to want exactly what the other person was offering, and vice versa. If a farmer wants fish, but the fisherman doesn’t need wheat, the trade collapses right there. And even when the trade worked, goods like cows or sacks of grain were bulky, perishable, and often indivisible. What if you only needed half a cow? Tricky, no? All this made barter messy and limited trade to local exchanges.

So humanity moved on to...

Collectibles

Shells, beads, feathers and even stones. And it was here when money became an abstraction for the first time. How? It wasn’t about something you could eat or directly use, but about something people agreed had value. In that sense, this was revolutionary, the first major technological leap in the story of money.

These collectibles were durable, divisible and portable, making trade easier than ever before. But there was a catch: abundance. If anyone could find or make more of these items, their value would just collapse. They couldn’t hold value over time. Plus, it was also difficult to trade outside of established communities because each of them had a different collectible of their own which they termed as money.

So, the search for something scarcer and uniform led humanity to...

Gold

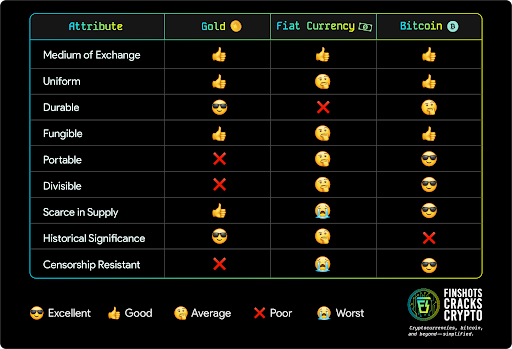

And you’ve to hold on to your seats, because this is one of the most popular abstractions that money saw at a larger level – to use precious metals to express value.

Gold checked all the boxes. Shiny and durable, easy to divide and transport (at least when compared to a rock), and most importantly, scarce. Its universal use as jewellery added intrinsic value, and its adoption by powerful rulers through taxation gave it legitimacy. Gold became the first universally accepted form of money, enabling trade across nations and creating unprecedented wealth.

So yeah, two big revolutions for money. And then nothing happens for hundreds of years.

But as trade and globalisation grew, societies realised that gold wasn’t perfect. Imagine trying to carry enough gold coins to buy a ship. Impractical, yes?

So humankind came up with a brilliant idea then – if we can deposit this gold with someone trustworthy, they can give us a promise note saying we have this gold in this trustworthy vault. We can then trade this paper instead of gold!!! It would solve a ton of our problems.

And that idea led to the invention of – you guessed it...

Paper Money

Paper money was a BIG deal.

You think people are freaking out about cryptocurrencies today? Think how much they must have been terrified about paper money!

It was unfathomable for many because well, the paper didn’t have any value. It was nothing that they had imagined as money before. And it took hundreds of years before paper money became globally acceptable.

Now, initially, paper notes were backed by gold reserves. You could exchange them for a fixed amount of gold.

So each note was essentially a promise that it could be exchanged for a specific amount of gold stored in central bank vaults. This system gave people trust in paper money, as it was directly tied to something tangible and scarce. Central banks would print money only equivalent to the gold they held, ensuring stability. This principle was officially established during the Bretton Woods Agreement in 1944, which pegged global currencies to the US dollar, itself tied to gold.

Thus it created a system where the trust in paper money was intrinsically linked to the gold reserves backing it. But this wasn’t just an economic strategy; it was a psychological one. The connection to gold made people believe in the value of the notes, anchoring the abstract concept of money to something real.

However, the abandonment of the gold standard marked a seismic shift in the story of money. It led us to what we today call...

Fiat Money

You see, in 1971, under US President Richard Nixon, the US decoupled the dollar from gold entirely. This decision, driven by rising deficits from the Vietnam War and domestic spending, was meant to stabilise the economy but had far-reaching consequences.

Governments could now print money freely. And this eroded the natural checks that gold once imposed. The shift fundamentally altered the dynamics of money, transforming it into a tool of policy rather than a store of value, and set the stage for the financial instabilities like soaring inflation, mounting national debts and inequities we grapple with today.

The removal of the gold standard was a turning point in monetary history. It was then when the US dollar emerged as the world’s reserve currency, largely because of America’s post-World War II economic dominance. And even when the US unilaterally ended this system in 1971, the dollar’s dominance remained.

Why? Trust. Despite its flaws, the dollar was backed by the strength of the US economy. It became a new kind of social contract.

And then, as the financial system grew, so did the layers of money as a form of abstraction.

Just that way a few decades ago, we saw a new form of money in the form of plastic cards. In fact, the first cards such as the US Diners Club cards were actually paper or cardboard, which were a form of traveller’s cheques. And in case you aren’t familiar with that term, a traveller’s cheque is a type of pre-printed paper currency that you can use instead of cash while travelling. It’s safer than carrying a lot of cash because if you lose it or it gets stolen, you can get a replacement.

And as we progressed, with credit cards, digital banking and now UPI payments, money became more intangible. Most of the money in the world today exists only as numbers on a screen. It’s a breakthrough and it keeps you in wonder.

Yet, for all its innovation, this system is riddled with huge problems.

That’s because banks don’t operate on a one-to-one reserve system. Instead, they practice something called fractional-reserve banking or a system where they lend out more money than they actually hold.

For instance, if you deposit ₹100, the bank might keep only ₹10 in reserve and lend out the remaining ₹90. And it doesn’t stop there. Banks also borrow from one another, creating a web of interbank lending that fuels even more debt. This domino effect means that if too many people try to withdraw their money at once, it could trigger a scenario known as “a bank run” and the system can collapse.

And let me tell you that history is littered with such examples, from the Great Depression in the US to more recent crises in countries like Greece, where citizens lined up at ATMs only to find their accounts frozen or empty. It’s a stark reminder that the money you see on your screen might not actually exist when you need it the most.

So yeah, to say the least, it’s a fragile system prone to collapse. And apart from banks, we have governments manipulate interest rates and print money to solve short-term crises, often at the expense of long-term stability.

The result?

A system that's riddled with problems: centralised control, inflation and inequality.

Enter Bitcoin!

In 2008, an idea called Bitcoin was born and a year later, in 2009, the first bitcoin transaction happened (something called a genesis block on the network). And that’s when the revolutionary journey truly began. It wasn’t just about creating digital money but a complete reinvention of the concept of money itself.

It’s entirely abstract. Forget the shiny gold coins that represent it with a “B” you see in pictures. Bitcoin is formless and shapeless or rather, just mathematical code. You can even hide it in a painting or write it down on paper. This makes it very different and special. And this abstraction is what makes it revolutionary.

No governments. No banks. No middlemen. Just pure code.

So obviously, when I first heard about Bitcoin, I couldn’t wrap my head around it. It was nothing like the money I knew. And so I started comparing it to the characteristics of traditional money and here’s how it went…

Like gold, bitcoin is scarce — only 21 million will ever exist. It’s durable too to an extent as it’s going to be around as long as we have the internet and a decentralised, incentivised network to back it. It’s more portable and divisible than any other form of money we’ve known. But unlike gold, its value isn’t physical. It’s in its network. Every transaction strengthens its dominance and adoption.

And the game-changer? No one can freeze or seize your bitcoin if you hold the private keys yourself. That’s because it’s not controlled by any single authority. Instead, it’s powered by a network of users and computers working together to keep things running smoothly.

So here’s the thumb rule, and the only rule with Bitcoin ownership: Your private keys, your bitcoin!!

(Private keys are like secret passwords that let you access and control your bitcoin. They’re long strings of numbers and letters—usually 64 characters—that keep your bitcoin safe. Without them, no one, not even you, can access your bitcoin.)

This makes it a big deal for financial freedom, especially in authoritarian regimes or during economic crises.

To understand this, let’s think about how money evolved. For centuries, and especially with the invention of modern money, hierarchical institutions like rulers, banks, governments, and other gatekeepers decided how money was used. They held the keys to your actions. Want to send some funds overseas? You’ll need a bank’s approval to accept or deny that request.

Then came the internet, which brought us apps and online services. But even these platforms have gatekeepers.

Bitcoin changed that. Because Bitcoin isn’t a platform, it’s a protocol. You see, platforms need middlemen to work. But protocols like Bitcoin let people deal with each other directly (peer-to-peer interactions). Thus it eliminates the need for gatekeepers.

Bitcoin’s creator, who used the name Satoshi Nakamoto, remains a mystery. But that’s part of its genius. It’s more of a feature than a bug. Why? Well, you can see all of Bitcoin transactions, thanks to its transparent system. But you’ll never know who made those transactions. Because Bitcoin is pseudonymous—that is, its addresses don’t reveal personal identities, unlike bank accounts.

So yeah, Bitcoin is different. Because protocols don’t need sign-ups or permissions. Just code and math.

When you buy bitcoin, you’re getting access to digital units stored on a decentralised ledger, secured by a public and private key system. Move it off a crypto exchange to a cold wallet (a device or a paper) or even write down your private key, and it’s all under your control.

It’s a system where nodes and participants work together under the same consensus rules. Every participant is equal. No one person or entity controls it.

So essentially, Bitcoin is the first widely adopted, network-centric, protocol-based form of money. Think of it like a universal language for money, opening up endless possibilities. Gold is durable but hard to carry. Paper money is easy to carry but not rare. Fiat money struggles with trust and censorship. Bitcoin scores high across the board.

Its major weakness? It’s young. But with each transaction, it gains legitimacy. All these years, it has survived countless attacks from hackers and governments, yet it goes on to shine brighter with every blow. It’s what they call antifragile—it thrives under pressure.

Sure, we could argue that it is a bubble or too volatile to be money. Maybe. But remember, money has always gone through chaotic changes before becoming stable as you just saw earlier. And volatility could also be a feature of its early stage of adoption, yeah? As more people and institutions adopt this technology, who knows, its price might just stabilise.

So Bitcoin is a simple line of code, but it holds the potential to change how we think about trust, value, and freedom.

Yes, it terrifies a lot. A transformation this fundamental always does.

But as the expression in the US goes, “Possession is nine-tenths of the law”. Well, in bitcoin possession is tenth-tenths of the law. There is no debt. No fake money.

In Bitcoin, possession of private keys is the ultimate proof of ownership, unlike traditional systems where intermediaries often control access to your funds.

If you hold your private keys, your bitcoin is yours. If you don’t, it’s not.

Internet changed many industries with just a few lines of Python code. That’s possibly what’s happening to money with the invention of Bitcoin and cryptocurrencies.

It’s one mathematical formula (and the only currency with a mathematical formula) that’s changing industries, nations, and how we think about value. And it may very well be years or decades from now that the world understands and accepts this.

We’ll end this long story on that note.

And in the next one, we’ll explore how Bitcoin goes beyond money—challenging economic systems and even sparking questions about its role in a world run by AI. Stay tuned!

Until next time…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

📢Finshots has a new WhatsApp Channel! If you want the sharpest analysis of all financial news without the jargon, Finshots is the place to be! Click here to join.

Only 17% of millennials have a term plan❗

Here's why getting a term plan early can do wonders for you & your family:

✅Protection: Simply put, term insurance is where you pay a small amount of money in exchange for a large amount of protection. This protection usually kicks in in the event the policyholder passes away.

But not just that, if you ever develop a critical illness (eg. cancer) and have to quit your job, a term plan can give you a lump sum amount to make up for the lost income.

✅Secure Your Parents: As your parents near retirement, they may start to rely on your income. And so, a term plan will give you peace knowing that they'll be financially supported even in your absence.

✅Low Premiums Forever: A term plan of 1CR cover will cost you much lower premiums at 25 years than at 35. You can even get a 1CR cover for as little as 10K a year if you are young and healthy. Plus, once these premiums are locked in, they remain the same throughout the term!

So don’t delay it! As they say, “The best time to buy term insurance was yesterday; the next best time is today.”

Click here to book a FREE call with Ditto Insurance's certified advisors and get your personalised term insurance guidance.