Do PSU stocks really rally because of elections?

In today’s Finshots, we explore whether PSU stocks rally because of elections or because of policy, reforms, and market expectations.

But here's a quick sidenote before we begin.

We’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 25th April at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 26th April at 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.

👉🏽 Click here to register while seats last.

Now on to today’s story.

The Story

Every election season, a familiar theory makes the rounds in Indian markets: buy PSU (Public Sector Undertaking) stocks because governments spend more, announce bigger projects, and prefer visible economic momentum when votes are around the corner.

And the logic feels almost too neat to question, right?

After all, public sector undertakings sit at the centre of infrastructure, defence, railways, banking, oil, power, insurance, utilities, and more. So, if the government wants to push growth, many of these entities are natural vehicles through which that push is delivered.

That is why PSU stocks are often perceived as a direct play on the political climate. When elections approach, investors begin assuming that roads will be built faster, railway budgets will rise, defence orders will increase, and disinvestment stories may return. And since these companies are tied so closely to state policy, many believe they must naturally outperform during election cycles.

But history tells a more nuanced story.

Sure, PSU stocks do react to elections. Sometimes painfully, and sometimes euphorically. However, they do not move simply because a government wins. To understand this better, let us take a step back and look at how Indian markets usually behave around elections.

First things first. Markets dislike uncertainty more than almost anything else. And elections are a perfect recipe for that. They create uncertainty by forcing you and me to think about multiple outcomes at once:

Will the incumbent return? Will a coalition emerge? Will welfare spending rise? Will fiscal discipline weaken? Will privatization accelerate or slow down?

All these questions matter because stock prices reflect future expectations, and not present headlines.

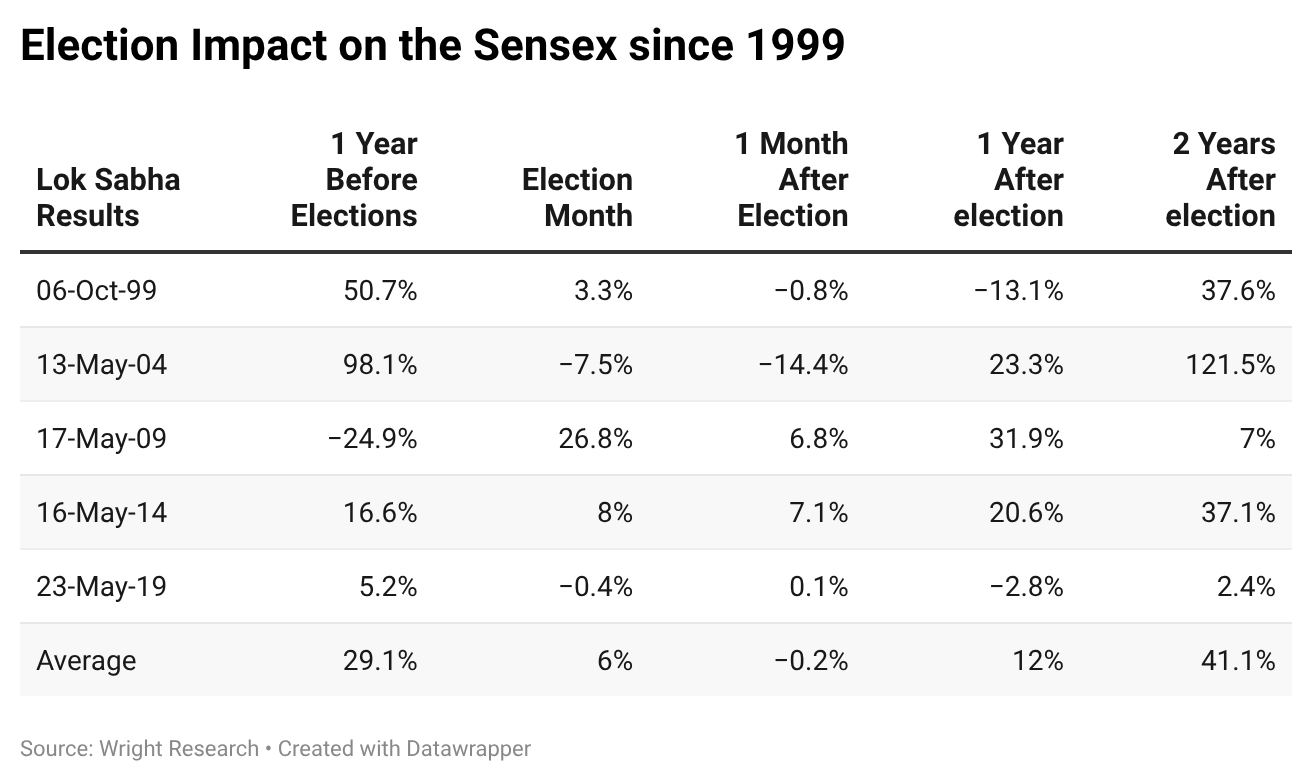

And historically, Indian markets have often performed well in the run-up to elections. In fact, they’ve shown average gains of roughly 29% in the twelve months leading up to general elections, with positive momentum often building even in the weeks just before polling.

But averages can be misleading because the path is rarely smooth. Election periods often produce some of the sharpest bouts of volatility in the market. And this is where PSU stocks become particularly interesting.

Unlike export-heavy IT firms or pharma companies, PSUs are deeply tied to domestic policy decisions. So when the government changes anything, these companies often feel it first. For instance, if the government prioritises railway capex, railway-linked PSUs can benefit. If defence indigenisation accelerates, defence PSUs may see stronger order books. If PSU banks receive recapitalisation support or benefit from state-led lending cycles, their earnings outlook changes.

So yes, elections do matter in this context. But because they can reshape the policy environment in which these businesses operate.

Take 2004, one of the most dramatic examples in Indian market history.

Markets had largely expected continuity. Instead, the Congress-led UPA coalition came to power with support from the Left. Investors feared slower reforms, resistance to privatization, and a less market-friendly policy direction. The reaction was immediate and brutal, with the Sensex plunging more than 14% in a single day. Many investors still cite this as proof that coalition governments are bad for markets.

However, that misses what happened next. Once fears eased and it became clear that the new government would still pursue growth and maintain economic stability, markets recovered strongly in the months that followed. And two years later, in 2006, the same index returned over 120%.

In this case, what changed was not just the election result. It was confidence around the policies the Left-aligned coalition would introduce.

Now let’s consider 2009.

The UPA returned with a stronger-than-expected mandate. And this removed much of the uncertainty surrounding coalition constraints and gave markets confidence that decision-making could continue with fewer obstacles. The Nifty surged over 15% on the result day, triggering upper circuits.

Once again, the market was not celebrating politics for its own sake. It was rewarding clarity, continuity, and the prospect of stable governance with the incumbent.

Then came 2014, which became especially important for PSU stocks & investors.

The BJP under Narendra Modi won a full majority. And the markets interpreted this as the start of a more ‘decisive’ policy era focused on infrastructure, manufacturing, state capacity, and, most importantly, execution.

That optimism did not emerge in a vacuum. BJP’s campaign itself was heavily built around economic revival after years of stalled projects, slowing growth, and corruption scandals.

Investors heard repeated themes such as better roads and ports, cleaner governance, more manufacturing, more jobs, reliable electricity, financial inclusion, and a government that would move projects from announcement to completion. In simple terms, markets believed India was moving from an era of drift to an era of delivery. And if that were to happen, PSUs were naturally positioned to benefit first.

So, defence PSUs such as HAL and BEL began benefiting from indigenisation narratives, domestic procurement pipelines, and later export ambitions. Railway-linked companies benefited from a multi-year capex cycle focused on electrification, track upgrades, station redevelopment, and freight efficiency. PSU banks eventually benefited from balance sheet cleanups, recapitalisation, and credit growth.

But it would be incorrect to say that all of this happened because of the election alone.

The election may have changed sentiment. But the real gains came later through budgets, reforms, healthier earnings, and investors assigning higher valuations to businesses they had long ignored.

And that is an important difference.

Take 2019, to understand this better. The BJP returned to power decisively, but the immediate market response was far more modest than in 2014. And why was that the case?

Because much of the narrative had already been priced in beforehand. Since it was the incumbent, investors already expected stable policy. As a result, the election itself did not create the same magnitude of upside or downside.

This teaches another important lesson: even a positive result may not drive markets much if expectations have already been factored in prices.

Then came 2024, perhaps the clearest example of why PSU-election folklore can be dangerous.

Exit polls had encouraged expectations of an overwhelming mandate. Instead, the ruling party fell short of a solo majority and required coalition support. As a result, markets sold off sharply, while several popular defence and railway PSU names corrected hard as investors suddenly questioned whether capital expenditure would slow.

Yet once markets understood that major policies were still broadly intact, panic eased, and prices stabilised.

Again, the lesson was clear. PSU stocks were not reacting to the dance of democracy itself. They were reacting to what investors believed the result meant for future spending and reforms.

This also explains why PSU performance around elections is never homogeneous.

Some PSU sectors are driven by budgetary support. Others by commodity cycles. Others by interest rates.

For example, a power utility may respond differently from a defence manufacturer. A PSU bank may respond differently from an oil producer. So, lumping all PSUs into one election basket can therefore be misleading.

So how can one make sense of all this, you ask? Well, there’s another factor investors often overlook: valuations.

For years, PSU stocks traded at steep discounts because markets saw them as inefficient, over-regulated, politically influenced, and poor allocators of capital. But in recent years, many of these names have recovered significantly. Some now trade on expectations of continued earnings growth, strong dividends, strategic relevance, or sustained capex support.

That means future returns may become harder to earn if expectations are already high.

A good election outcome may help sentiment. But if valuations are stretched and earnings disappoint, the stock can still underperform. Likewise, a temporary post-election selloff may create opportunities in fundamentally strong businesses with long growth runways.

This is why election investing often looks easier in theory than in practice.

Retail investors tend to focus on the headline event of “who won”. However, it’s important to also focus on second-order questions specific to policies and individual sectors or companies. These include:

- What is the administration's stance on capital expenditure (capex) and infrastructure?

- Will the new regime introduce stricter regulations for specific industries?

- Will there be continued support for domestic manufacturing and indigenization?

- Is there a clear economic blueprint for structural reforms?

- How will the government's agenda affect FII sentiment?

- Can the government effectively manage inflation and the fiscal deficit?

And this second layer usually matters more over time.

Which brings us back to the big question- do PSU stocks really rally around elections?

Well, sometimes they do. Sometimes they fall. And sometimes they do both within weeks.

But the better answer is that PSU stocks rally when elections increase confidence in future policies, and they struggle when results create uncertainty or challenge expectations that were already priced in. In that sense, elections are catalysts, not guarantees.

And for most long-term investors, the bigger lesson is not about timing the result-day moves. It is that wealth that is usually built through a focus on the fair value of a stock as well as disciplined asset allocation rather than getting carried away by political speculation.

Either way, what has consistently proven to win over the long term is owning a diversified portfolio bought at reasonable prices, aligned with your risk appetite, time horizon, and financial goals.

Because portfolios built on diversification, quality, patience, and sensible risk management tend to outlast all of them.

Until then…

If you liked this story, feel free to share it with your friends. family or even strangers on WhatsApp, LinkedIn, or X.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

A leading insurer is revising its health insurance premiums!

Policies issued after April 28th, 2026 (midnight) will reflect the updated premiums.

If you've already generated a quote, the premium may change once the revision comes into effect.

So, book a free call with Ditto to understand your options.