The Cult.fit IPO Explained

In today’s Finshots, we break down the upcoming Cult.fit IPO filing to understand the business and make sense of what the company is really worth.

But before we dive in, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.

Now onto today’s story.

The Story

Back in 2016, a company called CureFit Healthcare was incorporated with an incredibly ambitious dream. The goal was not just to open a few gyms, but to build a deeply integrated health and wellness giant. They wanted to tackle everything from physical fitness and nutrition to core healthcare.

However, over the next decade, an interesting shift occurred. One single vertical began to grow so rapidly that it completely overshadowed every other segment. That vertical was the fitness services and active lifestyle products business, what we know as Cult.fit today.

It became so dominant that in April 2026, the company retired the old CureFit corporate identity entirely and rebranded itself as Cult.fit Limited. Today, every single piece of its ecosystem, including physical gyms, a mobile app, treadmills, activewear, and workout accessories, sits under the familiar Cult name, all branded with its distinctive Vitruvian Man logo.

On the surface, this aggressive brand consolidation has been a success. Cult.fit has successfully scaled to become India's largest organised fitness platform. The numbers are hard to ignore. The company currently operates 708 fitness centres across 77 cities, serving nearly 1 million paying members. At the same time, it has built a significant retail footprint, selling gym equipment and apparel to fitness enthusiasts across the country.

But fueling this kind of nationwide expansion requires a mountain of capital, which brings us to the big news.

As per Cult.fit's DRHP, the company is looking to raise ₹950 crore through a fresh issue of shares to fund its next leg of growth. Simultaneously, its early backers, including the founder, Mukesh Bansal, are using this moment to cash in on their bets, and are selling up to 17.8 crore shares through an Offer for Sale.

This brings us to the most critical question on every investor's mind: what exactly are public shareholders buying into?

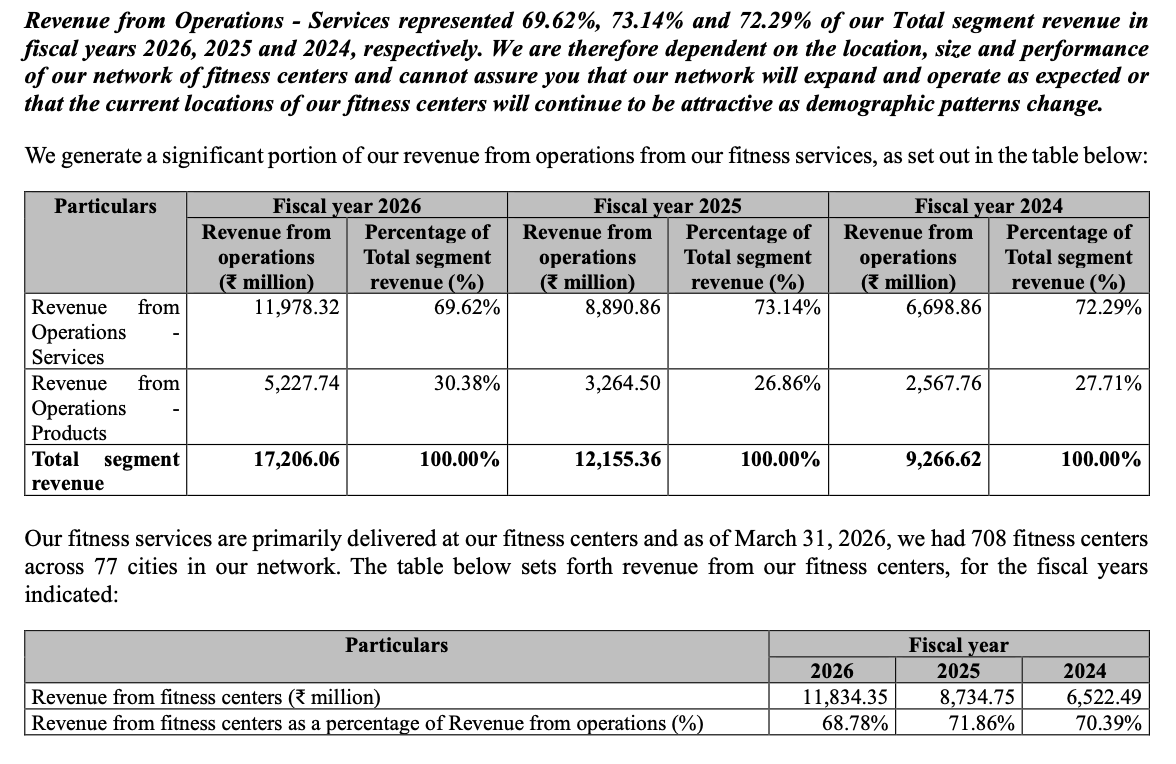

At first glance, you might look at Cult.fit and assume it is just a high-tech chain of boutique gyms. But that is only half the picture. The company actually runs a dual-engine model. Roughly 70% of its revenue comes from fitness services, which includes gym memberships, personal training packages, and corporate wellness programs. The remaining 30% comes from its product division, selling things like treadmills, activewear, and recovery gear.

The secret sauce that connects these two distinct worlds is the Cult mobile app. When a user signs up for a gym membership, the app actively coaxes them into the retail ecosystem. And the strategy is working. Today, nearly one-third of all active fitness members end up buying physical products directly through the platform.

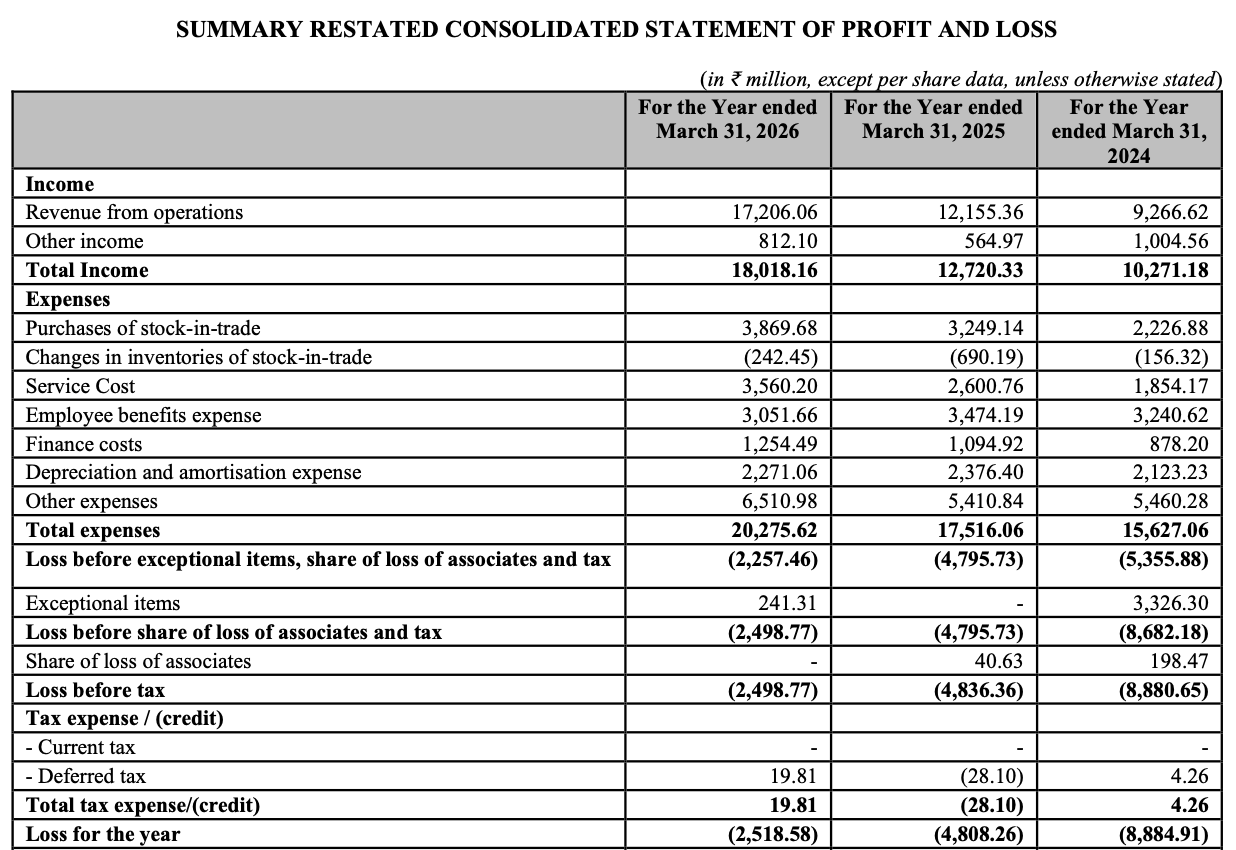

From a growth perspective, the company is clearly picking up speed. Their revenue has practically doubled over the last two years, skyrocketing from ₹927 crore in FY24 to ₹1,721 crore in FY26.

Even better, after years of heavy cash burn, its adjusted EBITDA (operating profit) has finally turned positive. If you look at the services side of the business alone, it has actually become quite comfortably profitable at a segment level.

But there’s a twist. Despite these operational milestones, the overall company is still deep in the red. In FY26, Cult.fit reported a net loss of ₹252 crore.

So, why is a business with a million paying subscribers still struggling to make a clean profit?

Well, the answer lies in the unrelenting costs of running a nationwide network of gyms. Every time Cult.fit opens a new location, it hits the books with heavy depreciation from expensive equipment, substantial finance costs, employee stock compensation, and expensive lease obligations.

In fact, while the company's traditional borrowings are not alarmingly high, lease liabilities because of physical gyms require long-term rental commitments. If certain underperforming subsidiaries continue to lose cash, Cult.fit will have to keep injecting fresh capital into them through corporate loans or equity infusions. That means less cash available for real expansion, and this raises the risk of painful future write-offs if those internal investments fail to recover.

In FY26 alone, Cult.fit spent over ₹90 crore simply on leasing its company-owned gyms, and another ₹90 crore on leases for warehouses, offices and retail stores. Put together, lease payments alone accounted for nearly 9% of the company's total expenses. And that's before spending a single rupee on trainers, electricity, maintenance or marketing.

And that's exactly the dilemma Cult.fit finds itself in. The company is losing money today, but pulling back on expansion isn't really an option either. India's organised fitness market is still severely underpenetrated, competition is intensifying, and the first player to build scale could enjoy lasting advantages in brand, network, and customer acquisition. So instead of slowing down to protect profits, Cult.fit is choosing to double down on growth. And that's precisely where the IPO comes in.

The single biggest use of the fresh capital is expansion. About ₹277 crore will go towards setting up new Cult Elite and Cult Neo fitness centres. Another ₹218 crore has been earmarked to pay lease and licence obligations on existing company-operated gyms. The rest will go towards repaying borrowings, brand marketing, and opening new Cultsport retail stores.

But the company has not actually finalised every single location for these proposed fitness centres, nor has it signed the leases for all of them. This means that a large portion of the expansion plan carries significant execution risk, leaving it squarely in the hands of management to deliver on their promises.

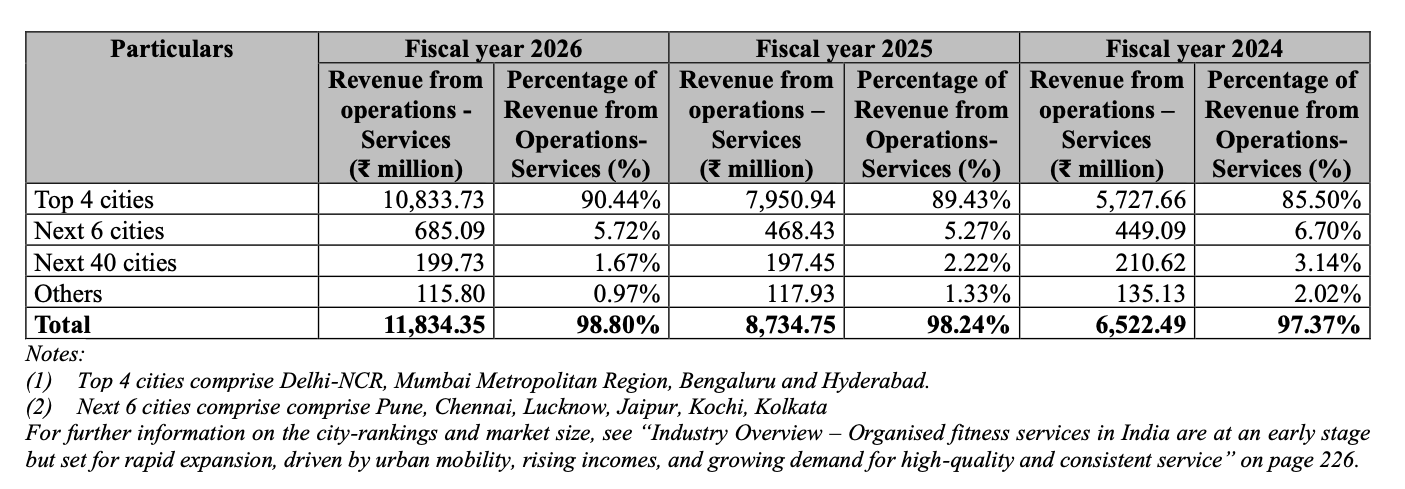

There is another reason why this expansion matters. Despite operating more than 700 fitness centres, Cult.fit's business is still heavily concentrated in India's biggest metros. In FY26, over 90% of its fitness services revenue came from just four cities: Delhi-NCR, Mumbai, Bengaluru, and Hyderabad.

That means its next phase of growth depends on successfully replicating the same economics in Tier-2 and Tier-3 cities, where consumer spending, fitness habits, and willingness to pay for premium memberships could look very different.

The management, of course, believes it has a clear blueprint to unlock true profitability. So instead of building capital-heavy, company-owned gyms everywhere, the plan is to pivot aggressively toward an asset-light franchise model. They are also looking to lock in high-margin corporate memberships, shift to localised manufacturing to insulate themselves from expensive imports, and expand the retail footprint of Cultsport. It is an incredibly ambitious strategy, but like most consumer platforms, every single lever depends entirely on flawless operational execution.

Ultimately, the Cult.fit IPO is a fundamental bet on a single thesis: can organised fitness in India mature into a highly profitable consumer tech platform, or will it always be weighed down by the heavy real-world economics of a traditional gym chain?

The company undeniably holds some incredible cards. It is the undisputed category leader, commands brand equity and has built a working ecosystem that successfully bridges physical services and retail products.

At the same time, it embodies the exact challenges that define India's new-age tech IPOs. It remains unprofitable on a net basis, relies heavily on adjusted metrics to show progress, and operates in a fiercely competitive market, all while early venture capital backers and the founder take a partial exit.

The real question moving forward is not whether more Indians will start working out, but whether Cult.fit can build a business where the financial metrics look as healthy as its customers. Because at the end of the day, public markets only reward a healthy balance sheet.

Until then…

Liked this story? Share it with a friend, family member or even strangers on WhatsApp, LinkedIn, and X.

How strong is your financial plan?

You've likely ticked off mutual funds, savings, and maybe even a side hustle. But if Life Insurance isn't a part of it, your financial pyramid isn't as secure as you think.

Life insurance is the crucial base that holds all your wealth together. It ensures that your family stays financially protected when something unpredictable happens.

If you’re unsure where to begin, Ditto's IRDAI-Certified insurance advisors can help. Book a FREE 30-minute consultation and get honest, unbiased advice. No spam, no pressure.