Working the WeWork India IPO

In today’s Finshots, we look at what’s hailing WeWork India and if its upcoming IPO is a promising one.

The Story

In 2023, WeWork Inc. filed for bankruptcy. A company once valued at $50 billion had crashed and burned. But now, WeWork India is knocking on Dalal Street’s doors with an IPO.

And that raises an interesting question — why would anyone invest in a failed business model?

Well, here’s the thing. WeWork India isn’t exactly WeWork Inc. It operates as a joint venture with Embassy Group (holding 73% stake), a major real estate developer in India. It’s an independent business that simply licenses the WeWork brand. And while its global parent was busy moving fast and breaking things (you can read our explainer on that here), WeWork India took a different route, focusing on sustainability and profitability.

So, how did WeWork India avoid the mess its global sibling created?

For starters, it learned what not to do. It fixed the business model.

Running a co-working space may sound simple. You rent an office, throw in some modifications, set up desks and lease them out. But there’s a catch because the biggest challenge is the mismatch between long-term leases and short-term clients. This means that most office spaces that WeWork rented were locked in for 10+ years, while co-working clients signed up for just a few months. That’s exactly what ruined WeWork Inc. When demand fell, the company was stuck with massive long term lease payments.

And you bet that WeWork India didn’t want to make the same mistake, so it took a different approach. Instead of just signing long term leases, it introduced two other things into the mix to make it asset-light.

- A revenue-sharing model where it partnered with landlords to split profits rather than paying fixed rent upfront. This way, if the space performed well, both parties benefitted. If not, they shared the losses.

- It also focused on attracting large enterprises as clients. The reason was simple. Startups come and go, but big companies lease office spaces in bulk for extended periods.

So although WeWork India primarily follows a leasing model, charging members a monthly fee per desk, it has experimented with asset-light approaches in select centres, roping in stability.

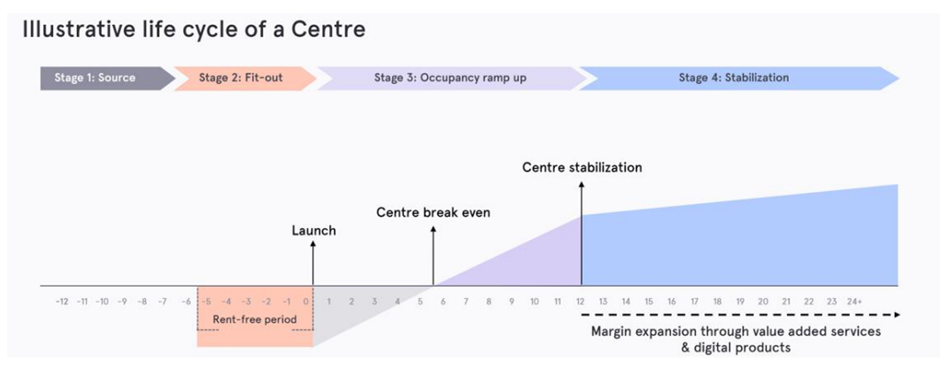

Another thing is that it didn’t blindly sign long-term leases. Instead, it leased bare shell (or unfurnished) properties and negotiated better lease terms. Most of its leases have a 3-5 year lock-in within a lease term of 10-year. So this reduced financial strain and risk. Plus, in some places it went on to secure an average rent-free period of over 5 months before lease payments kick in. And centers operating on a revenue-sharing model also shifted risk to landlords.

It has also played it smart financially. It turned profitable for the first time in 2024 (₹1,741 million profit in the first half of FY25), something WeWork Inc. never managed to do sustainably.

The next thing was fixing the economics of space utilisation. See, a profitable co-working space needs high occupancy rates and strong pricing power. If too many desks sit empty, costs spiral out of control. That’s actually also what happened with WeWork Inc. Despite having over 500 locations globally, nearly 30% of the office spaces in big markets such as the US sat vacant.

The reason?

Oversupply.

WeWork Inc. expanded in markets that weren’t ready for the coworking space revolution yet. And you could say that this served as a lesson for WeWork India. It only opened up spaces in tier 1 cities where the demand for coworking spaces was high instead of spreading its wings everywhere. Bengaluru is its biggest market, and overall occupancy rates across premium co-working spaces remain strong (We’ll talk about the numbers in a bit). Also, the demand is far greater than supply, which is a good sign for WeWork India. Demand for flexible workspaces (the category that WeWork India is the leader in) is outstripping supply too, especially in key cities like Bengaluru, Mumbai and Gurgaon.

That puts it in a great spot to capitalise on the booming coworking trend. For context, in 2018, it operated in just three cities with 8,700 desks. Today, it has over 94,000 desks across eight cities.

So yeah, that’s one piece of the puzzle solved. But the next question you might want to ask is: how sustainable is this growth?

Well, you could look at a few metrics that matter like the net ARPM (Average Revenue Per Member) which tells us how much the business earns per desk. And the revenue-to-rent multiple which tells us how efficiently the business operates.

And these numbers look great for WeWork India. Its net ARPM has grown steadily (from ₹16,000 in 2022 to ₹19,000 in 2024), and its revenue-to-rent multiple is a healthy 2.7x. In other words, it’s generating nearly three times what it pays in rent.

One of its key revenue drivers is the occupancy rate which is around 80%.

This also helps its unit economics. The more the occupancy, the more its coworking centres mature. And as they do that, they turn profitable. You see, the company achieves breakeven on a centre by reaching a 54% occupancy rate, and this is typically achieved within 4 to 6 months of opening of the centre.

Most of the initial operational expenditure incurred for a Centre is recovered by this breakeven point. And voila, any incremental utilisation beyond breakeven flows to the company’s unit-level profitability.

This also creates another benefit. The company’s fixed costs such as employee expenses and corporate overhead create a source of operating leverage as they become spread over a higher area across centres.

Add to that the fact that the company has prioritised big and corporate clients over small teams. As of 2024, about 60% of its revenue or net membership fees came from large enterprise customers with multi-year contracts. And that number has increased in FY25.

This has significantly reduced churn, and the company’s average membership tenure here was 28 months. That’s better than industry norms.

And it also means fewer cancellations and lower marketing costs.

Then you have to look at competition, which is quite fierce. As of now WeWork seems to have neck to neck occupancy rates and better rental as well as operating revenues than its peers ― folks like Smartworks, Awfis and IndiQube. But you have to remember that co-working is still an evolving market in India. And commercial real estate giants are jumping into the space, looking to offer flexible workspaces without the middleman. That’s something WeWork India will have to navigate.

That said, the final and big question now is: should you consider investing in the IPO?

On the one hand, WeWork India has a lot going for it.

But on the other hand, the IPO is an Offer for Sale (OFS). This means that all proceeds will go to existing shareholders, not the company. So, no fresh funds comes in for expansion. That raises some questions: If WeWork India is such a great business, why are existing investors cashing out? Without fresh capital, how will it fund its future growth?

Well, as the company puts it in the draft prospectus…

We do not expect to have any additional borrowings following the Offer. We conducted a rights issue of ₹5,012.81 million on January 11, 2025, and on January 13, 2025, we made a payment of ₹5,611.96 million to pre-pay our redeemable non-convertible debentures in full using the proceeds of the rights issue and operational surplus. As at January 15, 2025, we had ₹3,169.59 million outstanding borrowings, and we expect that our internal cash accruals would fund our growth capital expenditures.

In simple terms, the company is getting cash to expand its business as much as it seems the capacity for and it’s not overreaching for it by adding debt in its books. All this will again help it turn more profits as it goes on focusing its core markets in top tier cities.

The company isn’t stretching itself thin. It’s growing at a pace it can sustain. And that’s something its global parent could never figure out.

So yeah, WeWork India is undoubtedly a success story in the Indian co-working space.

But whether the IPO is a good bet will depend on valuations. If the price is right, it could be a good take on India’s flexible workspace future.

Either way, the IPO will be one to watch out for.

Until next time…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

🚨ATTENTION: FINSHOTS FAMILY

This Free Webinar on Life Insurance could be the key to securing your family’s financial future!

📅 Date: Saturday, 8th February

⏰ Time: 10:00 AM

We are organising an EXCLUSIVE webinar on one of the most important financial topics— LIFE INSURANCE.

What will you learn?

✔️ How to Secure Your Family’s Future Without Overpaying for Insurance

✔️ Struggling to Calculate Your Ideal Life Insurance Coverage? We’ll Show You in Seconds!

✔️ Why Mixing Insurance with Investments is a Costly Mistake—What to Do Instead

✔️ The Best Insurance Plan—Term, ULIP, or Endowment?

✔️ Life Insurance for Young Indians—Start Early, Save More!

Click here to register now. Only 400 spots available! Don’t miss out.

Pro Tip: We’re expecting a big audience of over 300 attendees! Join early to ensure a smooth entry and secure your spot.