Why Goldman Sachs is betting big on BSE

In today’s Finshots, we look at why everyone’s getting excited about BSE’s stocks.

But before we dive in, we have something exciting to share - Introducing Money Playbook!

Our brand-new series where we break down real-world money-making strategies with experts. And for the first episode, we're tackling a question we’ve all wondered at some point—how do you actually make money in real estate? Instead of guessing, we went straight to an expert to get the real answers.

The episode is live, and trust us, you don’t want to miss it. Watch it here!

The Story

It’s not every day that a financial giant like Goldman Sachs makes a big bet on a company. So when it picked up 7,28,000 shares or about 0.5% of BSE Ltd., everyone sat up and took notice.

Now, big institutional investors don’t just throw money around. Their moves are strategic, calculated, and backed by research. And in this case, Goldman’s vote of confidence has sent BSE’s stock soaring.

But what makes BSE such a compelling bet?

Let’s take it from the top.

You might’ve heard the phrase “The house always wins” in casino gambling, yeah? What it simply means is that casinos rake in profits regardless of whether gamblers win or lose.

Well, the stock exchange business works similarly. Traders and investors might make profits or losses, but intermediaries like stock exchanges, brokers and depositories always take their cut. And that’s where BSE (formerly Bombay Stock Exchange) comes into the picture. No matter which way the market moves, BSE makes money.

And that happens in several ways — charging transaction fees on every trade, collecting listing fees from companies going public, earning income from margins deposited by members, selling market data (data dissemination) and offering corporate bond listing and training services.

So you could say that it has a well-diversified revenue model spanning throughout financial markets. And what makes it even stronger is that its business is built for long-term retention and growth. Because once companies list on exchanges or traders start using its platform, switching isn’t easy. And this creates a sticky customer base. Plus, as more participants join the exchange, trading volumes increase, liquidity improves and more businesses and investors are drawn in. This is what we call the network effect and it makes the platform even more valuable over time.

That aside, we also have to consider that BSE is an integral part of India’s financial market. It runs BOLT Plus, the world’s fastest trading platform, executing transactions in microseconds. It facilitates trading across equities, debt, derivatives, mutual funds and commodities like gold and silver. And with a 15% stake in CDSL, one of India’s two major depositories, BSE has a strong grip on the financial ecosystem.

Put all that together and you’ll see why BSE is a solid business to bet on.

Then there’s the fact that BSE’s earnings and profits have been soaring, which is probably what Goldman Sachs is watching too.

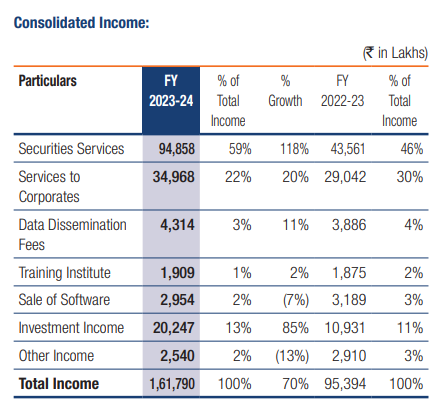

To break that down, a major chunk of its revenue flows from trading & clearing services. And right now, the real cash cow is Securities Services, the segment that directly rakes in transaction fees from trading activity.

In FY24, this segment contributed 59% of BSE’s total revenues, up from 46% in FY23. And the quarterly performance tells a similar story.

That’s because, more the trading volume, higher BSE’s transaction income in this segment. So yeah, steadily rising volumes is great news for equity cash, equity derivatives, mutual funds and clearing house income, the segment’s key contributors. For context, revenues from this segment jumped to ₹511 crores in Q3FY25, a whopping 157% increase from the previous quarter. And this growth wasn’t driven by just one factor. All major income streams played their part.

And let’s not forget BSE StAR MF, India’s largest mutual fund distribution platform. This segment delivered record-breaking performance in Q3FY25, with revenues soaring 92% YoY to ₹63.5 crores. The platform processed 17.99 crore transactions, a 39% increase over the previous quarter. On a monthly average, transactions jumped from 3.21 crore last year to 5.37 crore this year, proving that mutual fund activity is only gaining momentum.

So, the securities services segment is one of the key growth drivers for BSE.

In fact, if you take a step back and look at FY24 revenues, they surged 70% year-on-year, with the securities services segment alone growing by a massive 118%. And the momentum hasn’t slowed. Every revenue stream has been consistently expanding quarter after quarter.

But it won’t be fair if we only sing praises of one segment without talking about the other, the corporate services.

This segment, which handles IPO listings and other corporate transactions, contributes 22% of the business revenues and has been thriving.

Again the proof is in the pudding. In the last quarter (Q3FY25*), BSE saw 30 new listings, raising a record-breaking ₹95,512 crores — a staggering 261% jump year-on-year. And there are 108 active applications in the pipeline, signaling sustained momentum.

*Just a note here though. BSE’s latest concall transcript says that this income belongs to Q3FY24, but we believe this could be a mistake since the concall focuses on the latest quarter results.

This boom naturally reflects in BSE’s earnings. Listing fee income surged from ₹197 crores in 9MFY24 to ₹250 crores in 9MFY25. Meanwhile, other corporate services such as book-building fees more than doubled, jumping from ₹50 crores to ₹112 crores in the same period.

So looking at both the key segments ― the securities services and corporate services, delivering blockbuster growth, we could say that BSE clearly is on a roll.

But the real magic lies in BSE’s future plans.

You see, a focus area for BSE is StAR MF Plus, the next evolution of its mutual fund platform. Designed for better scalability and a seamless user experience, this could be a game-changer as India’s financialisation of savings accelerates.

Then there’s derivatives trading, where NSE has ruled for years. But BSE is pushing back, tweaking its model to attract more traders and expand its share of this high-volume market.

Beyond that, BSE’s subsidiaries are thriving in their respective domains. Its index business, run through Asia Index Private Limited (AIPL), has launched 15 new indices this year, creating fresh benchmarks for passive funds. Meanwhile, in a global push, India INX, BSE’s subsidiary exchange at GIFT City, is expanding its product offerings and attracting international investors into Indian markets.

And it doesn’t stop there. BSE is stepping beyond traditional trading, venturing into insurance distribution (BSE Ebix), power trading (Hindustan Power Exchange), and agricultural markets (BSE E-Agricultural Markets).

Each of these is a strategic move to diversify its revenue streams. And when you put all these pieces together, BSE’s growth story becomes crystal clear.

It’s the perfect mix of industry tailwinds, sharp strategic moves and a relentless focus on scaling its thriving businesses.

And hey, beyond expansion, BSE has also been smart with its finances.

How, you ask?

Well, its financial performance has been nothing short of impressive. In FY24, revenue surged 70% year-on-year. Net profit skyrocketed too ― 275%, with net margins doubling to 50%.

The best part? It’s a debt-free company with good return ratios. And for those who love dividends, BSE doesn’t disappoint. Even after trimming its dividend payout ratio in FY24, the actual dividend per share rose from ₹12 in FY23 to ₹15 in FY24. So investors are getting rewarded every year and they’re happy about it.

So Finshots, are you saying that BSE is bullet proof and destined to be the next multibagger?

Nope. Every business faces risks, and BSE is no exception.

NSE is still the go-to platform for derivatives trading, and when it eventually goes public, it could attract even more institutional interest. Then there’s the pricing game. Stock exchanges operate in a commoditised market where raising fees is tough, especially in India where BSE and NSE operate in a duopoly market. So BSE’s best bet is to increase market share, but that’s easier said than done. And finally, regulatory risks loom large. SEBI’s rules can impact everything from margins to listing procedures, affecting profitability. BSE has navigated these waters well so far, but staying nimble will be key.

But yeah, that said, the bigger picture still favours BSE. More Indians are entering the markets. The IPO boom continues. Financial products are becoming mainstream. And as India’s high-growth economy keeps expanding, the stock market and stock exchange’s business will only expand further.

And maybe that’s why Goldman Sachs wanted a piece of BSE. It sees the potential. Do you?

Until next time…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

📢Finshots College Weekly Programme is now on Whatsapp Channels! Click here to join the Finshots Student Community and get your weekly financial fix.

Only 17% of millennials have a term plan❗

Here’s why getting a term plan early can do wonders for you & your family:

✅Protection: Simply put, term insurance is where you pay a small amount of money in exchange for a large amount of protection. This protection usually kicks in in the event the policyholder passes away.

But not just that, if you ever develop a critical illness (eg. cancer) and have to quit your job, a term plan can give you a lump sum amount to make up for the lost income.

✅Secure Your Parents: As your parents near retirement, they may start to rely on your income. And so, a term plan will give you peace knowing that they'll be financially supported even in your absence.

✅Low Premiums Forever: A term plan of ₹1 crore will cost you much lower premiums at 25 years than at 35. You can even get a ₹1 crore cover for as little as ₹10,000 a year if you are young and healthy. Plus, once these premiums are locked in, they remain the same throughout the term!

So don’t delay it! As they say, “The best time to buy term insurance was yesterday; the next best time is today.”

Click here to book a FREE call with Ditto Insurance’s certified advisors and get your personalised term insurance guidance.