What market volatility actually tests

In today’s Finshots, we do an explainer on what market volatility is really testing and why your biggest investment decisions often have less to do with the market and more to do with how you respond to it.

But here’s a quick disclaimer before we begin. This story is not investment advice. The examples and data shared here should not be taken as recommendations to buy or sell any asset. Investments are subject to market risk, and past performance does not guarantee future returns. Always do your own research or consult a qualified financial advisor before making investment decisions. Do not YOLO.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. If you’re already a subscriber, thank you! Maybe forward this newsletter to someone who’d enjoy our stories but hasn’t discovered us yet.

Now onto today’s story.

The Story

The new financial year has just begun. For most investors, this is when you review your portfolio, tweak your SIPs, and adjust your goals. But this year feels different because that sense of control isn’t quite there.

Global tensions, especially in West Asia, have made oil prices volatile. Markets are swinging more often. Portfolios that looked steady a few months ago now feel uncertain. Which means even experienced investors are starting to wonder if their strategy can hold up.

And when markets get shaky, long-term thinking simply takes a back seat. You suddenly start judging a portfolio meant for 5–10 years, week by week, you start doubting gains, your losses feel bigger, and decisions that were earlier calm and planned start turning emotional.

But this isn’t new. It happens in every cycle. Each time, it creates the same feeling — that you need to do something different.

But here’s the part we often miss. Volatility isn’t a flaw. It’s how markets work. Prices move because expectations change, and expectations are always changing. What really matters isn’t volatility itself, but how investors react to it.

And that reaction is what shapes outcomes.

When markets fall or feel uncertain, stepping back feels natural. People pause SIPs, move to safer options, or wait for clarity before investing more. It sounds sensible. If prices fall further, you can invest later at lower levels.

But markets rarely operate that way. They don’t tell you when they’ve stabilised or hit the bottom. And by the time we get clarity, prices have often already adjusted, and the recovery is already underway. So the investor who stepped aside during uncertainty ends up re-entering at higher levels, having avoided the fall but also missing the rebound.

The real cost, therefore, is not the decline itself. It is the absence during the recovery.

To understand how this plays out in practice, let’s look at a simple dataset.

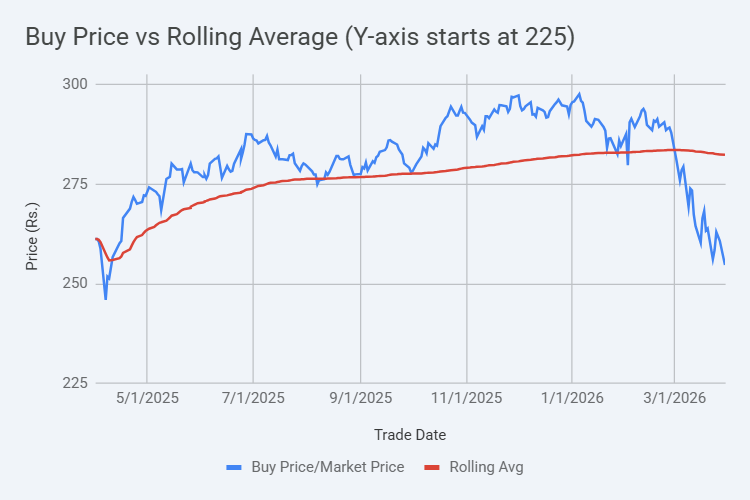

Over the past year (from 1 April 2025 to 1 April 2026), I have been buying one Nifty ETF (NiftyBees) every single day, without trying to time the market. As a result, I have deployed roughly ₹70,000 across 249 trading sessions. And my average purchase price was around ₹282 per unit, while the price on 1st April 2026 sat closer to ₹255. On paper, this translates to a loss of nearly ₹6,900.

At first glance, this appears to confirm the fear. You kept investing through volatile phases, and the market ended up below your average cost. It feels like a case where waiting would have produced a better outcome.

However, that interpretation misses what the data is actually showing. Because the value of this exercise does not lie in the current loss, but in the pattern of accumulation.

Prices did not move in a straight line. They oscillated, sometimes sharply, sometimes gradually. But throughout this period, units were accumulated across a wide range of prices, including periods when the market dipped significantly below the average.

If you look closely at the price trajectory relative to the rolling average, you will notice that the market spent extended periods above that average. The decline toward the end feels more pronounced because it is recent and unexpected.

Now consider the alternative.

If you had waited for the “right time”, you would likely have avoided buying during uncertain periods, especially when prices were falling. But those are precisely the periods where your buy price tends to be lower. By stepping aside during volatility, you are not just avoiding risk. You are also avoiding the opportunity to accumulate at more favourable levels.

And this is where the idea of timing becomes extremely tempting.

Because if you could just wait a little longer and deploy capital closer to the bottom, your returns would be meaningfully higher. The logic is intuitive. Lower entry price, higher upside.

But when this idea is tested over long periods, the results are not as compelling as they appear in theory.

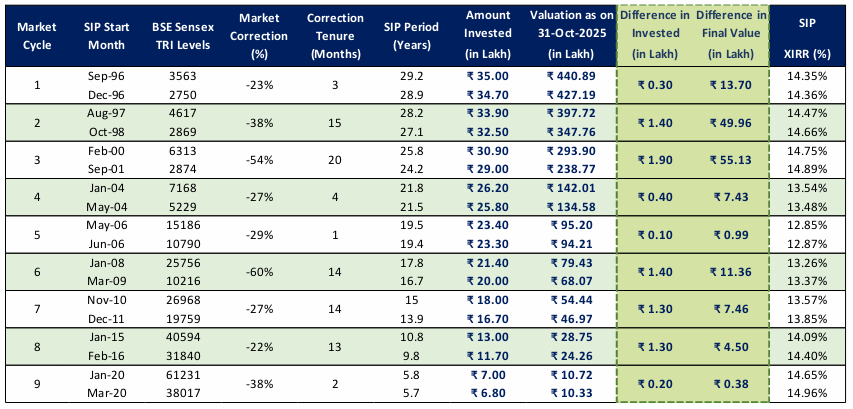

A study spanning three decades of market cycles sought to answer a simple question: What happens if you start an SIP at the market's peak versus its bottom?

Intuitively, you would expect a significant gap in outcomes. The investor who started at the bottom should outperform by a wide margin.

But that is not what the data shows.

Over long periods, the difference in returns between these two scenarios is surprisingly small. The XIRR (Extended Internal Rate of Return, annualised return, basically) converges to similar levels, regardless of whether the investment journey began at the top or the bottom of the cycle. The compounding effect of consistent investing gradually outweighs the initial disadvantage of a poor entry point.

So while the theoretical advantage of timing exists, the practical ability to execute it consistently does not. And that gap between theory and behaviour is where most outcomes are decided.

This brings us back to the role of volatility.

Volatility does not just create price movements. Instead, it creates moments where investors are forced to choose between sticking to a plan and reacting to the environment. And these decisions are rarely made in isolation. They are influenced by recent losses, headlines, peer behaviour, and the constant urge to avoid regret.

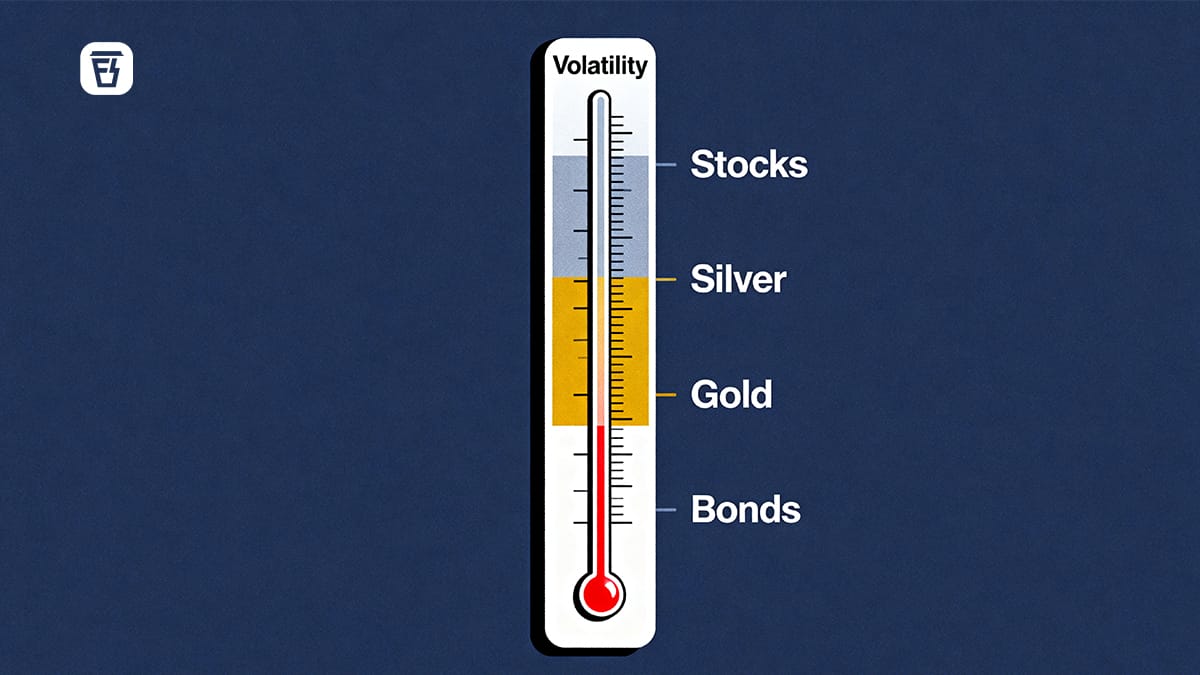

You can see this dynamic play out across asset classes as well.

Consider bonds. In a textbook scenario, rising inflation leads to higher interest rates, which makes fixed-income instruments more attractive. Capital flows adjust accordingly, often at the expense of equities and other risk assets.

But in practice, individual investors rarely capture these shifts perfectly. By the time inflation data is widely understood and rate hikes are expected, asset prices have usually already adjusted. That leaves most investors reacting to changes, not getting ahead of them.

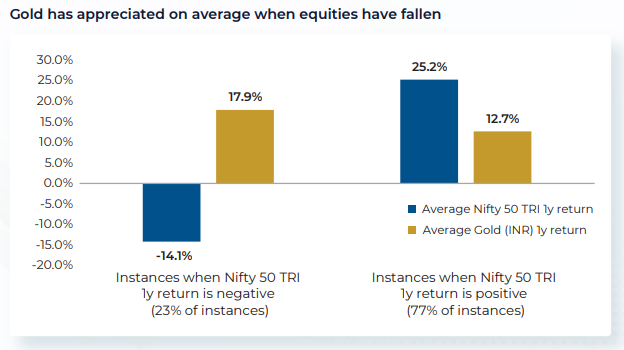

Gold tells a similar story, but through a different lens.

During periods of uncertainty in the stock market, gold tends to perform well as a store of value.

But instead of entering early, most investors wait for a correction, hoping to buy at a better price. The issue is that gold does not always provide those corrections in a clean or predictable manner. It often consolidates at higher levels or continues to trend upward in phases.

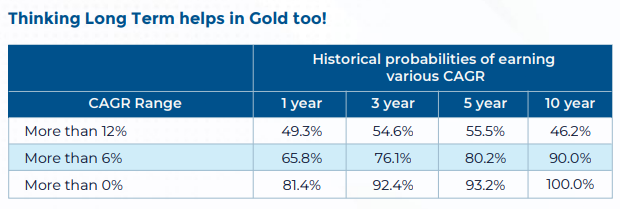

Historical data from June 1999 to August 2025 shows that 10-year rolling SIPs in gold yielded an XIRR of over 6% in 90% of instances. Most notably, none of the 10-year SIPs over that 26-year period yielded negative returns.

So the act of waiting does not necessarily improve the entry point. It simply delays participation.

Silver, on the other hand, amplifies this behavioural challenge.

Its price movements are sharper, more volatile, and often more erratic than gold. This creates the perception that it can be timed more effectively. Sharp rallies followed by corrections give the impression of clear entry and exit points.

But what happens is the opposite. Investors usually miss the early part of rallies, enter once momentum becomes visible, and exit during corrections. And the volatility that appears to offer opportunity ends up exposing behavioural weaknesses instead.

However, over a 42-year horizon between 1983 and 2026, silver's compounded annual growth rate is still around 10.5%. But because silver is driven by both precious metal sentiment and industrial demand (like solar panels and electronics), it acts less like a steady compounder and more like a high-swing asset.

Across all these examples, a consistent pattern emerges.

Volatility creates the impression that better decisions can be made by waiting. But in practice, waiting often leads to delayed action and, in turn, missed compounding.

And when you step back and connect all of this, you’ll see that markets will always move in cycles. But what changes from one cycle to another is not the pattern of markets, but the pattern of investor responses.

During calm periods, discipline feels effortless. But when uncertainty increases, that same discipline starts to feel uncomfortable. Every new data point invites a reassessment. Every correction creates the urge to act. And slowly, a structured plan begins to turn into a series of reactive decisions.

This is where the real test lies.

Because long-term investing is not built on the assumption that investors will always make the best possible decision. It is built on the assumption that they will continue to make decisions even when uncertain, and that those decisions will remain broadly consistent over time.

The data we have seen, whether through daily investing patterns or long-term SIP outcomes, all point in the same direction — the cost of being slightly early or slightly late is relatively small. But the cost of not being invested at all, especially during recovery phases, is much higher.

Over long periods, these decisions accumulate and show up not as dramatic losses but as lower returns, delayed goals, or missed opportunities. And because each decision felt reasonable at the time, the impact is often only visible in hindsight.

So when markets become volatile, what is really being tested is your ability to remain aligned with a strategy when outcomes feel uncertain. Because in the end, it does matter. Investing is less about navigating every fluctuation correctly and more about avoiding the series of small, emotionally driven decisions that pull you away from consistency.

And that is the uncomfortable truth about volatility.

Until next time…

Liked this story? Share it with a friend, family member or even strangers on WhatsApp, LinkedIn, or X.

How Strong Is Your Financial Plan?

You've likely ticked off mutual funds, gold & silver, and maybe even a side hustle. But if Life Insurance isn't a part of it, your financial pyramid isn't as secure as you think.

Life insurance is the crucial base that holds all your wealth together. It ensures that your family stays financially protected when something unpredictable happens.

If you’re unsure where to begin, Ditto's IRDAI-Certified insurance advisors can help. Book a FREE 30-minute consultation and get honest, unbiased advice. No spam, no pressure.