The Tata Sons - Shapoorji Pallonji feud

A couple of weeks ago, Tata Sons and the construction giant Shapoorji Pallonji Group were on the verge of fighting another bitter courtroom battle that would have further strained their relationship. But then within a matter of days, both parties reached a compromise that would help them walk away from the feud rather amicably. And if you’re wondering what this story is about and why any of this is relevant, today’s Finshots Market is for you.

Read the full story, to piece together the puzzle.

Act 1 — Bad Blood

The Tata empire is massive and its structure — quite complicated. At the top, we have Tata Sons. It’s the glue that holds together all of Tata’s ventures — Tata Steel, Tata Motors, Tata Consultancy Services (TCS), etc.

“Tata Sons”, in turn, primarily belongs to two large institutions.

- Tata Trusts — a group of charitable organizations set up by Sir Ratanji Jamsetji Tata. They own about 66% of the company and…

- The Shapoorji Pallonji group, who own about 18% of “Tata Sons”

In summary, Tata Trusts owns a majority stake in the enterprise. And Shapoorji Pallonji (SP) group, a minority stake.

With us so far? Good!!!

When Ratan Tata turned 75, he handed over the reins of his global empire to Cyrus Mistry, son of construction giant Pallonji Mistry. It was time to take a backseat, he said. He was impressed with Cyrus’s vision for the future and was further reassured by the fact that he had had a long association with Tata Sons. But this confidence didn’t last long.

On 24th October 2016, four years after Mistry’s appointment, Tata Sons shocked the business community by announcing that Cyrus Mistry had been asked to step down as the Executive Chairman of Tata Sons.

According to reports, Mistry had been asked to resign minutes before a board meeting. They also threatened to dismiss him through a no-confidence motion if he did not relent. Mistry for his part refused to step down and the board members took matters into their own hands. They fired him.

Ratan Tata was made interim Chairman. And Natarajan Chandrasekaran finally took over the reins on 21 February 2017. In the meantime, Cyrus Mistry filed a case of oppression and mismanagement against Ratan Tata and several others. The matter is yet to be resolved. But it’s safe to say that there is some bad blood between the SP Group and Tata Sons.

Act 2 — The Fundraise

Remember how we said that the Shapoorji Pallonji (SP) group mainly works in the construction and real estate sectors. Yeah, time to talk about that bit.

So ever since Coronavirus made landfall, the construction sector has had to deal with a triple whammy. First — the reverse migration. During the 40-day lockdown, over 10 lakh workers were forced to ditch construction sites and find shelter elsewhere. Some went back home. Even others turned to relief camps. But the damage had already been done. Labour costs skyrocketed in many parts of India and developers felt the pinch.

Also, considering multiple state governments had imposed heavy restrictions on movement and outdoor activities, there wasn’t a lot of construction happening in the first place. Meanwhile, companies also had to contend with cashflow problems. They had idle machinery, unused supplies and vacant facilities just lying around. They couldn’t use this stuff. But they had to keep paying their dues. This added financial burden meant many entities had to reevaluate entire projects even after the lockdown restrictions were lifted.

Including the SP Group. The company had to deal with financial problems of its own and it was desperately looking to raise some money in a bid to tide over the crisis. Thankfully, they managed to elicit some interest and rope in a clutch of global investors to raise about ₹11,000 crores in total. On September 4th, they finalised the paperwork and were hoping to access some of these funds.

But almost immediately Tata Sons intervened.

Why? you ask.

Well… SP Group was raising money by putting up shares of Tata Sons as collateral. And the board at Tata Sons wasn’t very comfortable with this arrangement. Their contention was simple. Pledging of shares technically amounts to a transfer of sorts. After all, if SP Group fails to repay in full, the borrowers will own these shares by default. And according to the Articles of Association (a document that defines rules for running an organization) that's a no-go. Because the document clearly prescribes that the board of Tata Sons ought to have the right of first refusal.

Meaning, they get first dibs before anybody else can make an offer. They have a right to buy these shares at fair value before somebody else can walk in. So just one day later, they went to the Supreme Court to stop the company from pledging the shares altogether and the court agreed with their assessment. They barred the SP Group from pledging shares. Until October 28, when the court promised to deliver a verdict on the matter.

The SP group, of course, was outraged. They believed Tata was deliberately blocking their efforts at fundraising. As an SP group spokesperson noted, “This vindictive move by Tata Sons is solely aimed to create delays and roadblocks in the fund raise that will jeopardize the future of 60,000 employees and over 1 lakh migrant workers who draw sustenance by working at various SP Group facilities.”

And for a while, it seemed like things were about to get out of hand. But then, there was a truce. Tata offered to buy the 18% stake SP group held in the company (Tata Sons). And SP Group, for its part, saw it best to accept the offer. They also added that it was in everybody's best interest for Tata to simply buy them out.

And that leaves us with the final question — How is Tata funding the deal?

Act 3 — The Buyout

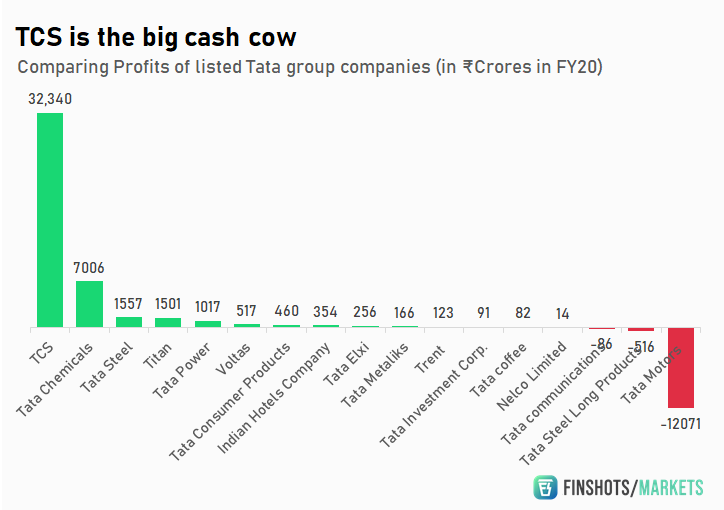

For starters, there’s going to be some debate surrounding what the stake is actually worth. According to reports, SP Group pegs the value at ₹1.8 lac crores. Tata seems to think its only worth about ₹1.5 lac crores. But even if we were to go with the more conservative estimate, it’s going to be really challenging for Tata to raise this kind of money. Most of Tata’s group companies are bleeding cash. And they can’t borrow money either because they only recently promised to reduce debt by the boatloads over the next few years. And that leaves us with one final option — TCS.

Tata’s stake in TCS is worth close to ₹6.7 lac crores. If they were willing to sell parts of TCS to fund this exercise, maybe they could pull it off. But selling TCS also means they’ll have to forego part ownership in their crown jewel. And there are definite downsides here because Tata has used money from TCS to fund some of their other loss-making ventures in the past. So if Tata keeps selling these shares whenever they’re in trouble, that probably sets a bad precedent, no?

What do you think?

How will Tata fund this little program and do you believe they’ll be forced to make some tough choices now?

Let us know your thoughts on Twitter.

Share this Finshots Markets on WhatsApp, Twitter.

The ₹2000 Note Dilemma

Also, have you been wondering where all the ₹2000 notes are disappearing?

Actually. You know what…. It doesn’t matter if you have been thinking about it because the fact of the matter is — It is indeed a rare sight to spot one of these notes these days and if you’re interested in knowing how we got here, you’ll probably want to read this story. It’s a good one you know :)

Don't forget to share this Finshots Markets on WhatsApp and Twitter.