The Quality Power Electrical Equipments IPO

In today’s Finshots, we break down the Quality Power Electrical Equipments IPO. And just a heads up, we’ll be mentioning figures in ₹ million since that’s how the RHP (Red Herring Prospectus) quotes them.

The Story

Before diving into the IPO, let’s start with some context on the energy space.

Energy is hands down one of the most valuable commodities in the world. Humans need energy to create an abundant and prosperous future. It has always been so, and it will continue to be so. No nation, developed or developing, consumes a low amount of energy. And as technology accelerates, so will energy consumption.

And an interesting thing to observe here is the transition of energy. A few years ago, any energy dealer with coal, oil or natural gas would have been living their best life. But today, they, along with new players, are shifting to renewable energy sources like solar, wind and hydrogen. And this transition isn’t happening in isolation. Energy moves. First, it is generated, then transmitted, then distributed, and finally consumed. And for this transition to work, the infrastructure that moves energy needs an upgrade too.

And that’s where Quality Power Electrical Equipments steps in.

Simply put, the company manufactures equipment that ensures high-voltage energy moves smoothly across the grid and new energy sources integrate smoothly into this grid. To understand how, let’s look at the products themselves.

There are two key technologies in energy transmission ― High Voltage Direct Current (HVDC) and Flexible Alternating Current Transmission Systems (FACTS). These fall under the broader category of grid modernisation equipment.

You can think of HVDC as a super-efficient highway for electricity. It reduces energy loss over long distances. On the other hand, FACTS helps stabilise power flow and improve grid reliability. And these technologies are essential for transmitting electricity, especially as renewable energy sources like solar and wind are integrated into the power grid.

That’s exactly what Quality Power Electrical focuses on. It provides equipment under these categories through two segments:

- Power Products: This includes reactors, transformers and line traps, which are essential components for high-voltage power transmission.

Reactors regulate voltage levels and reduce power losses. Transformers adjust voltage to ensure efficient transmission. And Line Traps block unwanted communication signals from interfering with power transmission.

- Power Quality Systems: These ensure stable grid operations, with solutions like static VAR compensators (SVCs), STATCOMs, harmonic filters and capacitor banks.

These equipment basically stabilise voltage and improve power factor to ensure a steady, uninterrupted electricity supply.

In the first half of FY25, these two segments contributed nearly ₹700 million and ₹800 million in revenue respectively. That’s almost an equal split.

And most of this revenue for the company comes from markets outside India. Yup. Exports are what sets the company apart so to speak. Unlike most competitors that generate 20-30% of revenue from international markets, Quality Power makes 80% of its revenue from exports. And with operations spanning nearly 100 countries, the company is India’s top exporter in this niche segment.

That brings us to ask ― How’s the company stacking up against its competitors in doing so?

You see, this market is highly competitive and home to some big names like Siemens, Hitachi Energy, Transformers & Rectifiers and GE T&D. And while Quality Power is a much smaller player in terms of revenue, it has a distinct edge: growth!

A quick glance at the prospectus tells us the story.

Quality Power has seen stellar revenue growth at 28% compounded annual growth rate (CAGR). This is led by its strong export sales portfolio which we just saw. In FY24, its revenue stood at over ₹3 billion, an 18% jump from FY23, whereas the average growth among peers was 12.8%. So, we can say that the company is one of the fastest growing among its peers.

This growth also reflects in its margins. EBITDA, or profit before interest, tax and depreciation, for Quality Power came in at 12% in FY24. That means for every ₹100 spent, the company earned ₹12 before interest, tax and depreciation. And this again, is above the average levels of competitors.

Now, you might say that this isn’t surprising, since the company is smaller in scale and above-average growth is natural. And that’s a valid point. The largest competitor (Siemens) made ₹195 billion in revenues in FY24 ― a whopping 65 times Quality Power’s FY24 revenues!

But one way to verify the performance is by looking at its debt and interest costs. The reason is that the energy transmission equipment business is capital-intensive. It requires huge sums of upfront capital to set up manufacturing units, procure raw material and implement advanced tech. It also comes with a long payback period. And that’s why getting capital at good interest rates as well as managing debt becomes crucial.

Well, it seems that Quality Power has been keeping a close eye on its borrowings too. The average debt-to-equity ratio of its peers stood at 0.24x, 0.26x and 0.15x from FY22 to FY24, respectively. But for Quality Power, the same stood at 0.20x in FY24 and presently it sits at 0.1x.

As the prospectus states.. Quality Power Electrical Equipments Ltd. debt has increased from Rs. 106.08 million in FY23 to Rs. 382.79 million in FY24 where equity was at Rs. 1,756.57 million in FY23 and increased to Rs. 1,903.26 million in FY24. The debt decreased in H1FY25 while the equity increased to 2386.26 million making the debt-to-equity ratio 0.11 indicating reduced borrowings.

So we could say that despite keeping expansion in mind, the company has been allocating funds wisely. You could also verify this by looking at something called the ‘gearing ratio’. This ratio tells us how much of a company’s funding comes from debt versus equity. So, a high gearing ratio = high reliance on debt, which can be risky in uncertain times.

How does that look for Quality Power? From -0.54 in FY22, -0.31 in FY23 and further improving to just -0.05 in FY24. What this essentially means for Quality Power is that it was not only able to reduce its interest cost but was also more flexible to invest in future growth without being weighed down by more borrowed funds.

This financial prudence also explains why the company has been doing well at the net profit levels. The company’s profit after tax or the net profit has been growing from ₹422 million in FY22 to ₹554 million in FY24. Profit margins stood at 16% in FY24, among the best in the industry, thanks to increased revenue and lower interest and depreciation costs.

However, the company’s return on capital employed (ROCE) is lower than that of its peers. And that’s because it has been expanding aggressively. Let us explain.

You see, ROCE tells you how efficiently a company is using its capital to generate profits. A higher ROCE means better efficiency in generating returns from investments.

So, Quality Power’s lower ROCE is due to its aggressive expansion strategy. The company has been investing heavily in assets, which grew from ₹252 million in 2022 to ₹399 million currently. Expansion often means taking on higher costs before seeing proportional returns. But since it has also been quick in managing debt, its ROCE has not deteriorated much, indicating that its investments are starting to pay off and generate stronger returns.

And all that gives us a sense that the company is doing well in its space.

Now, let’s look at its IPO.

The company intends to raise ₹858.7 crore through its offering, and of this ₹255 crores is through fresh issue whereas ₹633.7 crores is through offer for sale. And it intends to utilise the fresh proceeds in three key areas.

First, the company plans to acquire Mehru Electrical and Mechanical Engineers, a move that could help expand its product offerings and technical capabilities in energy transmission solutions. Second, a portion of the funds will go toward capital expenditure for upgrading and expanding its manufacturing facilities, ensuring that it can meet growing domestic and international demand. And lastly, the company has earmarked a part of the proceeds for inorganic growth and other strategic initiatives, such as potential acquisitions and investments in research and development.

So far, so good.

But what about the downsides? Well, the company sure faces some risks as it operates in a challenging market.

The energy sector is cyclical, and it’s also highly regulated. These factors could affect the company’s revenues and project viability. Then there’s the export concentration risk. With 80% of its revenue coming from international markets, the company is vulnerable to exchange rate fluctuations. Additionally, electrical manufacturing is a high-compliance industry, where any regulatory or legal challenges could impact operations. And the industry relies heavily on skilled labour, and a shortage of highly trained engineers and technicians could impact production efficiency and overall business growth.

That said, Quality Power operates in an industry that has wide room for growth.

If we just look at the power quality products market, it’s set to grow at a CAGR of 18% over the next 4 years!

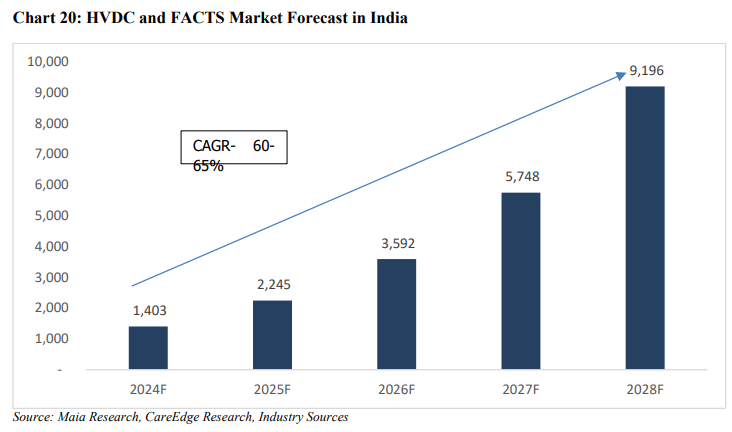

Meanwhile, the HVDC and FACTS market is expected to expand at a staggering 65% CAGR!!!

These are estimates that surely make you want to become an energy equipment dealer, no?

Well, Quality Power is already one.

It operates in a booming industry with competitive advantages as compared to its peers. And there’s undoubtedly stiff competition too. But if it keeps up the momentum, who knows? It might just give the industry a giant run for their money. What do you think?

Until then…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

Only 17% of millennials have a term plan❗

Here’s why getting a term plan early can do wonders for you & your family:

✅Protection: Simply put, term insurance is where you pay a small amount of money in exchange for a large amount of protection. This protection usually kicks in in the event the policyholder passes away.

But not just that, if you ever develop a critical illness (eg. cancer) and have to quit your job, a term plan can give you a lump sum amount to make up for the lost income.

✅Secure Your Parents: As your parents near retirement, they may start to rely on your income. And so, a term plan will give you peace knowing that they'll be financially supported even in your absence.

✅Low Premiums Forever: A term plan of ₹1 crore will cost you much lower premiums at 25 years than at 35. You can even get a ₹1 crore cover for as little as ₹10,000 a year if you are young and healthy. Plus, once these premiums are locked in, they remain the same throughout the term!

So don’t delay it! As they say, “The best time to buy term insurance was yesterday; the next best time is today.”

Click here to book a FREE call with Ditto Insurance’s certified advisors and get your personalised term insurance guidance.