The Oswal Pumps IPO – riding on a government pipeline?

In today’s Finshots, we dive into the business of Oswal Pumps which closes its IPO application window on 17th June ’25 (Tuesday).

Prefer listening instead? Whether you're jogging, commuting, or just too lazy to read, tune in to listen to this story and more on Spotify or Apple podcasts.

Also, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

You’ve probably seen them before. A dusty farmland with a tube well sunk deep into the earth and an electric pump buzzing next to it, pulling water to the surface like magic. It’s been the beating heart of India’s agricultural productivity. And behind that pump, there’s a good chance the motor came from Oswal Pumps.

Why do we say that?

You see, India’s farmers have always depended on groundwater, with over 85% of rural water supply drawn from it. But to do that, you need lots of power. Either diesel (which is costly) or electricity (which is often unreliable). And that was a big problem until 2019 when the government launched a ₹34,000 crore scheme called PM-KUSUM. The scheme has three moving parts: mini-grids on barren land (Component A), off-grid solar pumps replacing diesel ones (B), and on-grid solar pumps replacing electric ones, plus agri-solarisation (C). And it plans to install or solarise over 49 lakh pumps across Indian farms to slash electricity bills, boost productivity and make agriculture greener. The government would roll out subsidies and rope in companies to build and install the systems.

So for manufacturers like Oswal, this was a windfall. The company already made traditional submersible pumps. Adding solar modules and mounting frames to its portfolio was a natural extension. So after starting in 2003 manufacturing low-speed monoblock pumps, Oswal eventually began building the entire ecosystem itself—from motors to impellers to casting parts.

Today, it’s one of India’s few integrated pump manufacturers serving three main segments:

- Pumps – both for agriculture and domestic uses (like apartment complexes).

- Castings – including third-party supplies.

- Turnkey solar-powered pumping systems and solar PV modules – especially for government clients.

And now, it wants to raise a total of ₹1,387 crores from its initial public offer (IPO).

So let’s take a closer look at how the company makes money.

Well, the real kicker for Oswal is its solar pump business. Thanks to the PM-KUSUM scheme, Oswal began offering bundled solutions that include solar panels, inverters, controllers, mounting structures and the pump itself. The final kit is then installed for state agencies.

And that’s where it has found its stride. In FY24, nearly 85% of its revenue came from solar water pumping systems sold under PM-KUSUM. Between FY22 and FY24, revenue more than doubled. Net profit grew from ₹17 crores to ₹97 crores. But here’s the thing. PM-KUSUM-based solar pumping systems still accounted for over 87% of Oswal’s revenue in nine months ended FY25. And that’s a problem because the scheme is nearing its original target as well as its deadline in March 2026. Unless a Phase II or new subsidy framework is announced, Oswal’s revenue stream could start drying up in less than a year.

And revenue diversification still seems like work in progress. There’s talk of more exports, a retail push for regular pumps and there are solar panels and pressure booster pumps in the mix too. But for now, these form a small sliver of the revenue pie. The bulk of the business still flows through subsidy channels and the non-subsidy business is still reliant on price-sensitive rural markets.

Which brings us to the numbers.

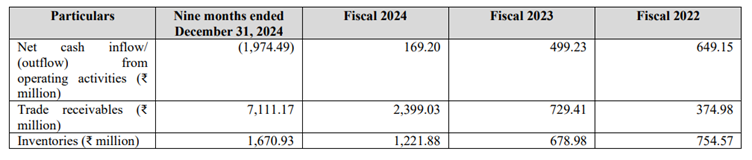

As of nine months to December in FY25, Oswal clocked ₹1,067 crore in revenue and ₹321 crore in earnings before interest, tax and depreciation expenses (EBITDA). That’s 30% of sales in operating profits. But that didn’t translate to cash since operating cash flow was negative ₹197 crore.

Why?

Working capital issues.

See, selling to the government or through government channels is a slow game. Payments are delayed, receivables pile up and inventory builds as projects get staggered. That’s perhaps why Oswal had 66% of its revenues stuck in trade receivables (up from 30% in 2024), about 40 days of inventory (goods sitting in storage) and a working capital cycle (the time it takes to convert inventory and receivables into cash) of 142 days. So while profits looked good, the cash was still on paper.

As the company puts it… ‘trade receivables increased from ₹ 729.41 million as of March 31, 2023 to ₹ 2,399.03 million as of March 31, 2024 and further to ₹ 7,111.17 million as of December 31, 2024 as we started direct billing under the PM KUSUM scheme from October 2023, which has a relatively longer payment realization.’

This creates two problems. First, the company has to borrow more to finance its operations. Second, interest costs are chewing up profits (₹28 crore in nine months of FY25 alone from ₹8 crores in 2022). Compare that to peers with tighter cycles and net cash positions, and Oswal looks stretched.

To its credit, Oswal plans to change that. Of the ₹1,387 crore IPO (₹890 crore fresh issue + ₹497 crore offer for sale), ₹280 crore will go toward debt repayment, ₹273 crore into a new solar module manufacturing unit for its subsidiary Oswal Solar, ₹89 crore in funding capital expenditure and the rest for subsidiaries and corporate use.

It’s a sensible allocation to clean up the balance sheet and build out new verticals. But sensible on paper doesn’t always mean safe.

The solar module business is already dominated by giants like Reliance, Adani and Tata Power, all of whom secured subsidies under the government’s PLI scheme. And the real question is whether Oswal can compete on price, volumes, and distribution without similar tailwinds.

Then there’s geographic risk.

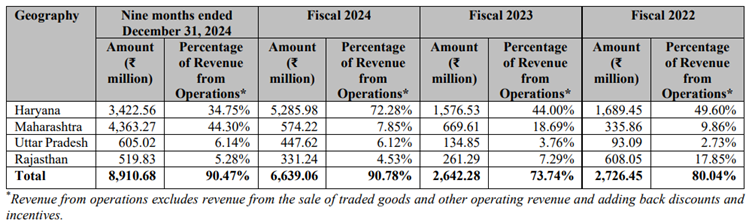

Oswal still earns about 80% of its revenue from a few states in northern and western India. There’s minimal presence in eastern or southern markets. It hasn’t cracked metros. International sales are 3-4% of total revenues.

And lastly, let’s get to the big question: valuation.

The IPO is priced in the band of ₹584–614 per share. That values it at a price to earnings ratio (P/E) of over 60x (as per earnings per share or EPS of 9.8 on FY24 earnings)! Compare that to its biggest peers in the industry — Shakti Pumps (66x P/E) or Kirloskar Brothers (41x), and Oswal doesn’t look cheap. Especially for a company still so dependent on one scheme, one customer and one market.

Oswal’s closest listed peer, Shakti Pumps, also rode the KUSUM wave. But it diversified early by building a solid export book, launching EV chargers and automation systems and selling to private irrigation clients.

And while this isn’t a huge exit, the promoters are offloading a sizeable chunk through the OFS.

So yeah, Oswal Pumps has ridden the policy tide well. It scaled fast, integrated backward and tapped into the solar dream when the sun was shining brightest.

But the question isn’t whether the company is good, it’s whether it's ready for a world where policy support no longer exists. To keep growing, it will need new customers, new geographies, better cash flow management and bold capital allocation.

And until it turns its integrated manufacturing strength into a truly diversified, scalable business, the bet on IPO could be less about pumps and more about investor patience.

Until then...

Don’t forget to share this story on WhatsApp, LinkedIn and X.

Did you know? Nearly half of Indians are unaware of term insurance and its benefits.

Are you among them?

If yes, don’t wait until it’s too late.

Term insurance is one of the most affordable and smartest steps you can take for your family’s financial health. It ensures they do not face a financial burden if something happens to you.

Ditto’s IRDAI-Certified advisors can guide you to the right plan. Book a FREE 30-minute consultation and find what coverage suits your needs.

We promise: No spam, only honest advice!