Why is every app trying to become a microfinance app?

In today's Finshots, we talk about how microfinance became so prevalent in India.

But here’s a quick side note before we begin.

A few days ago, one of our founders was chatting with a friend who thought life insurance was something you buy in your 40s. He was shocked that it was still a widely held belief.

Fact: Life Insurance acts as a safety net for your family. The younger you are, the cheaper it is. And the best part? Once you buy it, the premium remains unchanged no matter how old you get.

Unsure where to begin or need help picking the right plan? Book a FREE consultation with Ditto's IRDAI-Certified advisors today.

Now on to today’s story.

The Story

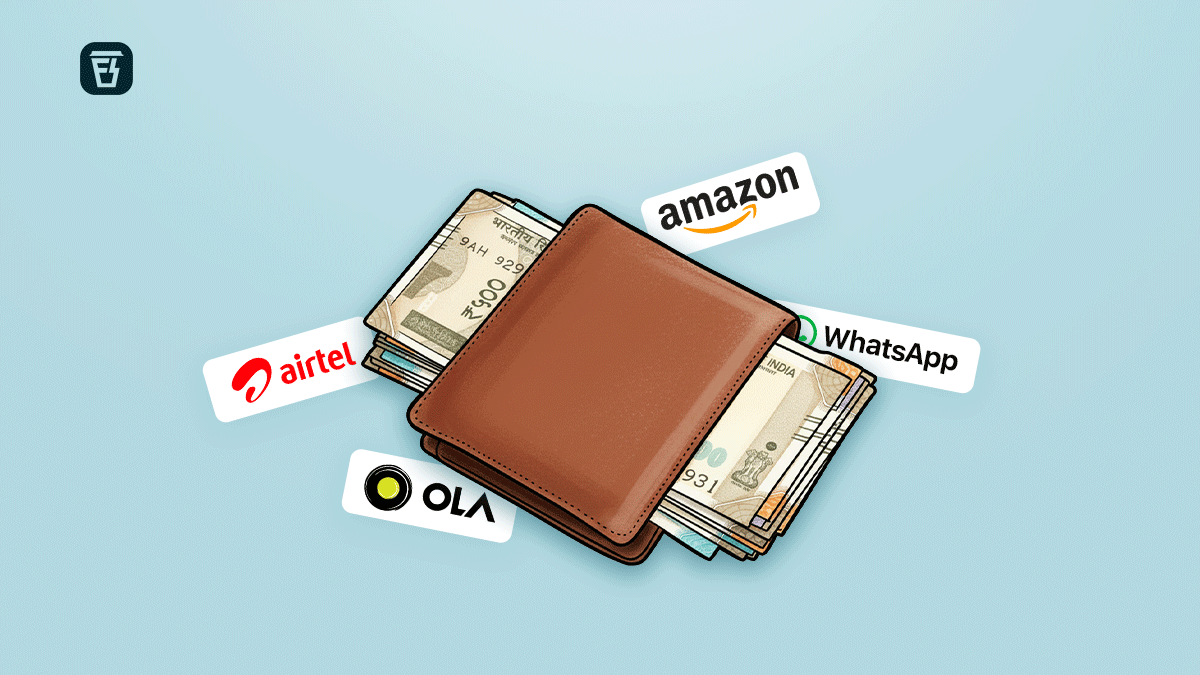

A few days ago, Amazon launched a feature that lets users invest in fixed deposits and mutual funds through Amazon Pay. A decade ago, that would have sounded absurd. eCommerce apps were supposed to sell products, deliver food, or help you book rides. Not manage your savings or lend you money. Yet here we are.

Microfinance has seeped into almost every consumer app these days. But to understand why, let’s rewind a few years and look at what apps did initially to monetise their users.

You see, a decade ago, consumer apps in India competed on one thing alone: distribution. Whoever could acquire users faster, cheaper, and at scale usually won. Discounts, cashbacks, free deliveries, and aggressive marketing were all justified by the same belief that once scale was achieved, profits would eventually follow.

As a result, companies invested heavily in marketing and built large customer bases. But that belief was eventually shattered because having users alone did not guarantee conversion. On top of that, growth eventually slowed as competition increased across sectors, and capital also became scarce.

In this environment, companies were discovering a hard truth: selling goods or services alone is a weak business model. Margins became thin, customer loyalty became fragile, and price competition never really ended. Which is why so many platforms have gravitated toward microfinance. But why finance?

Unlike food delivery, e-commerce, or ride-hailing, where transactions end at checkout, financial products create recurring interactions and predictable revenue streams. Finance monetises scale and retention far more efficiently than commerce ever can. And savings and investment products anchor users over long time horizons. Because let’s face it, once we start using an app for investing, we’re far less likely to actually shift to a different one unless something dramatic happens.

And that’s exactly what companies want to bet on. This is why Amazon now lets you invest via Amazon Pay, Airtel runs a payments bank inside their app, WhatsApp has UPI embedded right beside your chats, and even Ola lets you get a personal loan on their ride-hailing app. They operate through partnerships, positioning themselves between users and regulated institutions.

You see, India’s financial system has a well-documented gap between formal banking and large sections of the population. Millions of individuals and small merchants remain underserved because traditional lending relies on income proofs, collateral, and credit histories that many people simply do not have. Banks are constrained by regulations and cost structures and struggle to serve these segments profitably at scale.

NBFCs, on the other hand, do not face the same constraints. But NBFCs do not have a good distribution system to get users. Apps like Amazon, Ola, and Airtel have exactly that.

They already observe user behaviour continuously. They see transaction histories, spending patterns, repayment consistency, geographic stability, and cash-flow signals in real time. This data allows platforms to underwrite small-ticket credit quickly by partnering with NBFCs or banks, without building branches or employing loan officers. What physical microfinance institutions once did through field agents and paperwork, apps now do through software and data.

As a result, buy-now-pay-later products became a direct outcome of this shift. They reduce friction at the point of purchase and encourage users to stay within a platform’s ecosystem. From the app’s perspective, credit becomes a tool to accelerate commerce while simultaneously building a financial relationship that can be monetised repeatedly.

The same logic explains why co-branded credit cards have proliferated. These cards extend the platform’s influence beyond its own app and into a user’s broader spending behaviour. Each transaction reinforces brand presence, generates interchange income, and deepens the financial link between the user and the platform. Compared to one-off commerce transactions, this is a far more durable way to monetise attention.

However, the strengths of embedded finance are also where the risks begin.

The ease with which credit is offered changes how borrowing feels. Traditional loans involve friction, which forces borrowers to evaluate their debt. Embedded credit removes much of that, and repayments are broken into small instalments, charges can be deferred, and borrowing is framed as convenience rather than obligation. Individually, these loans may appear manageable. But if overused, they can become difficult to track, especially when you stack multiple BNPL products across different apps.

This problem is compounded by pricing opacity. While headline interest rates may look low or even zero, effective annualised costs often rise sharply once fees, penalties, and delayed payments are included. The user experiences the benefit immediately but absorbs the cost gradually, which weakens financial discipline rather than strengthening it.

There is also a systemic risk element that is easy to overlook.

Most consumer apps operate lending through partnerships, sitting between the customer and the institution that actually owns the loan. Now, this is generally good for both parties, as it allows rapid scaling, but it also creates misaligned incentives. Platforms are rewarded for growth and engagement, while credit risk sits elsewhere. So, when economic conditions worsen (as they did after COVID), defaults rise, and lenders pull back. This reduces access to the credit that was once available easily, and users who grew accustomed to frictionless borrowing suddenly find themselves locked out (or even worse, it shows up on your CIBIL score).

Yet it would be misleading to frame this entire shift as exploitative. For many first-time borrowers, app-based credit serves as an entry point into the formal financial system. Responsible usage and timely repayment help build credit histories, which can later unlock cheaper loans, mainstream banking access, and better financial products. And in that sense, embedded microfinance is far better than informal moneylenders as they expand inclusion at a scale traditional banking has struggled to achieve.

This is probably why every app wants to move in this direction. Finance offers higher margins, recurring revenue, and stronger user lock-in than commerce. All while credit accelerates spending, and savings products deepen the relationship. From a platform’s perspective, this evolution is rational, even inevitable.

For users, however, the burden of responsibility increases.

When borrowing becomes invisible and effortless, financial discipline matters more, not less. Embedded finance delivers real value when it substitutes expensive, informal credit and expands access responsibly. But it becomes harmful when it normalises constant, fragmented debt without clear signals of cost or risk.

The future of finance is likely to be deeply embedded and largely frictionless. Whether that future improves financial well-being or undermines it will depend on how transparently these products are designed, how carefully they are regulated, and how consciously users engage with credit that no longer feels like borrowing at all.

Until then...

Don't forget to share this story with your friends, family or even strangers on WhatsApp, LinkedIn and X.

For the third year in a row, we present Finshots’ Current Affairs Round up 2025!

A FREE and comprehensive compilation of our most impactful financial, economic, tech and business highlights of the year is here. Get our classic 3-min reads in an easy to access PDF eBook.

Plus, we made sure to add our signature infographics too! Click here to access the PDF resource now.

And don’t forget to share this with your peers, friends, and anyone in your network who might benefit from it.

Happy Reading :)