What is going on at Vauld, anyway?

In today's Finshots we see what happened at Vauld

Also, a quick sidenote before we begin the story. At Finshots we have strived to keep the newsletter free for everyone. And we’ve managed to do it in large parts thanks to Ditto — our insurance advisory service where we simplify health and term insurance and make it easy for people to purchase the product. So if you want to keep supporting us, please check out the website and maybe tell your friends about it too. It will go a long way in keeping the lights on here :)

The Story

On Monday, Singapore-headquartered crypto company Vauld shocked the world by releasing a statement saying that it was suspending all withdrawals, deposits, and trading in cryptocurrencies for its users. And it was a shock because just a couple of weeks earlier, it had published a note titled, “Vauld’s 6-month plan to ship great products”.

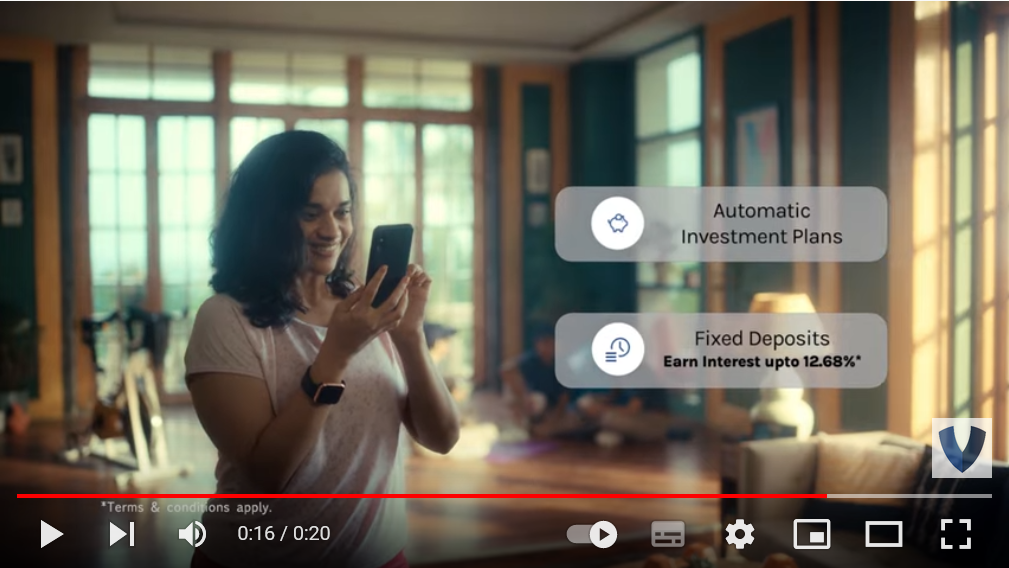

Now before we get into what went wrong at Vauld, let’s rewind to October 2021. Vauld had just grabbed everyone’s attention with its first slick advertisement — “For Everything Crypto Just Vauld”. Vauld’s proposition was that it could do the grunt work of automating your crypto investments. So you could really laze around and do nothing while your money compounded.

At the end of the ad, it also showed us another very interesting thing — Fixed Deposits with a super-high interest rate. Now it’s no secret that Indians love the idea of fixed deposits. But they weren’t just offering a measly 5% interest — the kind banks offer. No, this was an eye-popping 12.68% interest and it looked very enticing.

But Vauld knew that ads alone wouldn’t be able to convince the naysayers. It needed some help. So, it turned to financial influencers to promote their offering. The company got some of the most popular “finfluencers” to wax eloquent about the virtues of crypto “Fixed Deposits!”

And it worked. People jumped on the bandwagon.

So, the big question is — how did these deposits work?

Imagine you’re somebody who has close to $10,000 in bitcoin. It’s just lying there in your wallet and you want to put it to good use. And somebody comes along and makes you an offer. They tell you that you could potentially earn 10–12% interest on your deposit with consistency — almost like a fixed deposit. And you think that’s great.

But you have questions.

How on earth can anybody offer you 12% fixed with such a volatile asset?

Well, here’s one way they could potentially do this. They take your bitcoin and promise to return it sometime in the future. In the meantime, they convert it into cash (or Tether, a cryptocurrency that’s supposedly as good as USD) and lend these proceeds to individuals desperately looking to borrow money — who in turn are expected to pay the principal and interest on top. Now what they do with this money is up to them really. But as you probably already understand, anybody looking to borrow money is expected to put up collateral. So the borrower may put up cryptocurrencies they own. But the total value will have to tally up to something substantial — say 150% of the loan amount — just for extra security. And if the value of this collateral ever dips below a certain threshold, then the institution facilitating the whole transaction can simply sell the borrower’s holdings and pay the lender in full.

So it’s a neat little arrangement that benefits all parties involved.

And while this is a very crude explanation of what’s happening at the backend (and one of many), it still does a reasonably good job of depicting the kind of risks inherent in these products. There’s nothing fixed about this transaction. Borrowers can default en masse. The value of the collateral can dip precipitously. People may seek to withdraw their deposits all at once. Many things could go wrong.

And they kind of did.

Look at Celsius, another company that paused withdrawals quite recently.

As the Wall Street Journal reported, Celsius had given out crypto loans to the tune of $2.7 billion. But it seems they didn’t back this loan with enough collateral. Apparently, the value of the collateral only tallied up to about half the loan value. So when lenders began asking for their principal, they didn’t have enough collateral to liquidate. And without collateral, they had to dip into their own reserves, which ran out rather quickly. Before you knew it, they had to suspend withdrawals and “fixed deposit” investors were left holding the bag.

Is this what happened with Vauld? We don’t know for sure. But we hope that the company does offer more insights on what really went wrong.

So what does this mean for the company and the investors?

Well, not all is lost yet it seems. A London-based crypto lender Nexo seems to be trying to put together a potential acquisition. But, only after it conducts an extensive check to determine what went wrong and what it can salvage out of this situation. And we all know that these things take time.

In the meantime, hopefully, we can at least take some lessons away from this mess.

For starters, if something seems too good to be true, it probably is.

Also, when a company says “all is well”, while there’s pandemonium in the streets, you should probably second guess their statement.

And finally…don’t just believe what influencers on social media tell you. They’re paid to sell. They’ll sell anything so long as they can make money off of the brand. You need to exercise better discretion.

Until then…

Don't forget to share this article on WhatsApp, LinkedIn and Twitter