The Ujjivan Small Finance Bank IPO

We have a special edition today. Ujjivan Small Finance Bank is going public. And on popular demand, we are covering the issue right here, right now.

So let’s get right into it

The Story

Before we get to Ujjivan, the small finance bank. We need to talk about Ujjivan, the Financial Services company.

For the uninitiated, Ujjivan Financial Services started off as a Non-Banking Financial Corporation in 2005 with a very specific focus — Microfinance. Meaning they wanted to target the unbanked and the underprivileged by offering them small loans at reasonable interest rates (we will explain this) so that the people wouldn’t have to rely on loan sharks who were downright extortionate. They did this for a while until, in 2016, they were granted a banking license. Okay, not an actual banking license like the kind allotted to SBI, HDFC, and the likes. No, this was a special kind of license called the small finance banking license. Meaning unlike conventional banks, Ujjivan was expected to stick to a very specific mandate i.e. they had to operate at least 25% of their banking outlets in unbanked rural areas and 50% of their loans had to be limited to sizes< 25 lakhs. There are other restrictions as well. But these are the more important ones and they tell us something very important — Despite being a for-profit bank, there is a social motive here and we can’t entirely look past this.

So let’s begin with that, shall we? How does a for-profit bank serve the low-income population?

The Joint Liability Group

Well, the first problem to tackle here is the creditworthiness problem. The rural unbanked don’t have a credit score to speak of. So it’s very hard to tell if a borrower is likely to pay you back in full. Ujjivan tackles this problem by primarily issuing loans to groups of people rather than individuals. They call this the Joint Liability Group and there are some obvious advantages here right off the bat.

For one, during the formation of a group, participants have every incentive to screen each new entrant so that they don’t prove to be a liability. This way, the group can screen itself. Also, once the loan is sanctioned, they are more likely to ensure the amount is used judiciously. But more importantly, the shame and guilt associated with being a defaulter in a group will prevent any one person from squandering the money and not repaying the loan. So the concept works pretty well.

Unfortunately, these loans are still unsecured i.e. they are predominantly offered without collateral. Meaning if the group defaults there’s no recourse for the bank. Yes, they could resort to scare tactics threatening people with broad repercussions. But most state governments have issued strict directives to prevent this sort of thing. So that’s a no go. Meaning they’ll have to take precautions some other way.

The Business Model

One way the likes of Ujjivan put up safeguards is by issuing loans of small ticket sizes. Usually, the loans range from Rs.2000 to Rs. 60,000 with a tenure of up to two years. Hence the name — MicroLoan. This way even if a group does default, the damage is contained. Yes, they do offer vehicle loans and loans for affordable housing but about 82% of their loans fall into the microloan category.

Secondly, they charge pretty high-interest rates. We are talking 22–24%. This is a way of compensating for the risks associated with unsecured lending. Now I know we said these were reasonable rates. But that was a relative assessment. If you are comparing this with the loan sharks who usually charge upwards of 60%, immediately this proposition will look enticing. Also more often than not, Ujjivan disburses loans at the customer’s doorstep. This way people won’t have to wait inside a conventional bank all day long. There's convenience here folks.

Finally, Ujjivan offers most of its loans to women entrepreneurs. The academic evidence is unanimous here. Women prove to be good borrowers and good payers. And if you’re a bank, that kind of assurance can go a long way. So long story short, the company has a very nice setup in place. And once they were allowed to transform into a small finance bank in 2016, it paved the way for the company to start accepting deposits. This was a monumental change for Ujjivan.

Bring down the Cost

Banks make most of their money based on a simple premise. They borrow at low-interest rates and lend at relatively higher interest rates. However, when you are borrowing from other banks, funds don't come cheap. More often than not, they charge you upwards of 10%. But if you’re accepting funds from the public, say via getting them to park their money in a savings account, you can effectively borrow at 3-4%. So by taking in deposits, banks can mobilise funds at a much lower cost.

However, this comes with a caveat. To be able to transition into a deposit-taking institution, you will need to set up local branches, have the right kind of manpower and make big investments that might take a while to pay off. But Ujjivan for its part has been dealing with this part pretty well. Their cost to income ratio has declined from 95% in 2017 to 64% in June 2019. Meaning they are reigning in their costs while still making a lot of money. And since India has the highest number of unbanked adults in the world, there’s still a lot of room to expand.

Unfortunately, things are not always as straightforward as they seem.

For the people

On 8 November 2016, the Government of India announced that it wanted to demonetise all ₹500 and ₹1,000 banknotes. While the intended motive was to curb black money and punish corruption, the exercise had far-reaching consequences. Most importantly it had a veritable impact on the informal sector. Consider Western UP for example. Small and Medium-sized enterprises that primarily relied on daily wage labour could not cough up the cash required to pay their workers. Soon enough good people who wanted to come through on their loan repayments simply couldn't do so because of the cash crunch. And as more people began defaulting, there was a strong demand for loan waivers from many parts of the state. The upcoming elections in Uttar Pradesh only exacerbated the problems. Politicians started making bold promises and committed to waiving loans entirely if voted to power.

If you haven’t figured out the problem here, then let me make it simple. Political insinuations like these could spell a lot of trouble for banks like Ujjivan. In fact, post demonetisation, the company saw a rise in bad loans, it had to stop its expansion spree, regroup once again and change its strategy. Although the bank managed to wiggle out of the ordeal relatively unscathed, it was bad. Because once people realise that they don’t have to pay back their loans, there will be defaults in large numbers. It spreads like wildfire. And if there's one thing about fires, it's that you don't play with them.

Who's the promoter?

Another potential issue is the promoter conundrum. While Ujjivan Small Finance Bank is fully owned by Ujjivan Financial services (a holding company) the company does not have a promoter. Yes, technically Ujjivan Financial Services would be the promoter here. But then Ujjivan Financial Services has no promoter. It’s a professionally managed enterprise and some people believe that No Promoter = Lack of vision/ambition.

But not everybody agrees with this assessment. Ujjivan has done exceedingly well for all these years. So why would anyone expect anything to change on this front? In fact, it's greedy promoters that often screw up. So one could contest that the lack of a promoter here is actually a good thing.

But even without a greedy promoter, Ujjivan was recently on RBI's radar. And that is most certainly a problem. While the issues didn’t seem like they were all too grave, you can’t be messing about when you’re a bank. There’s a whole bunch of red flags and we highly recommend you read this article from BloombergQuint if you want the full scoop.

And since we have already stretched this too far, we need to stop here. But before we leave, here’s a nice infographic comparing the most important operational metrics of Ujjivan with other small finance banks.

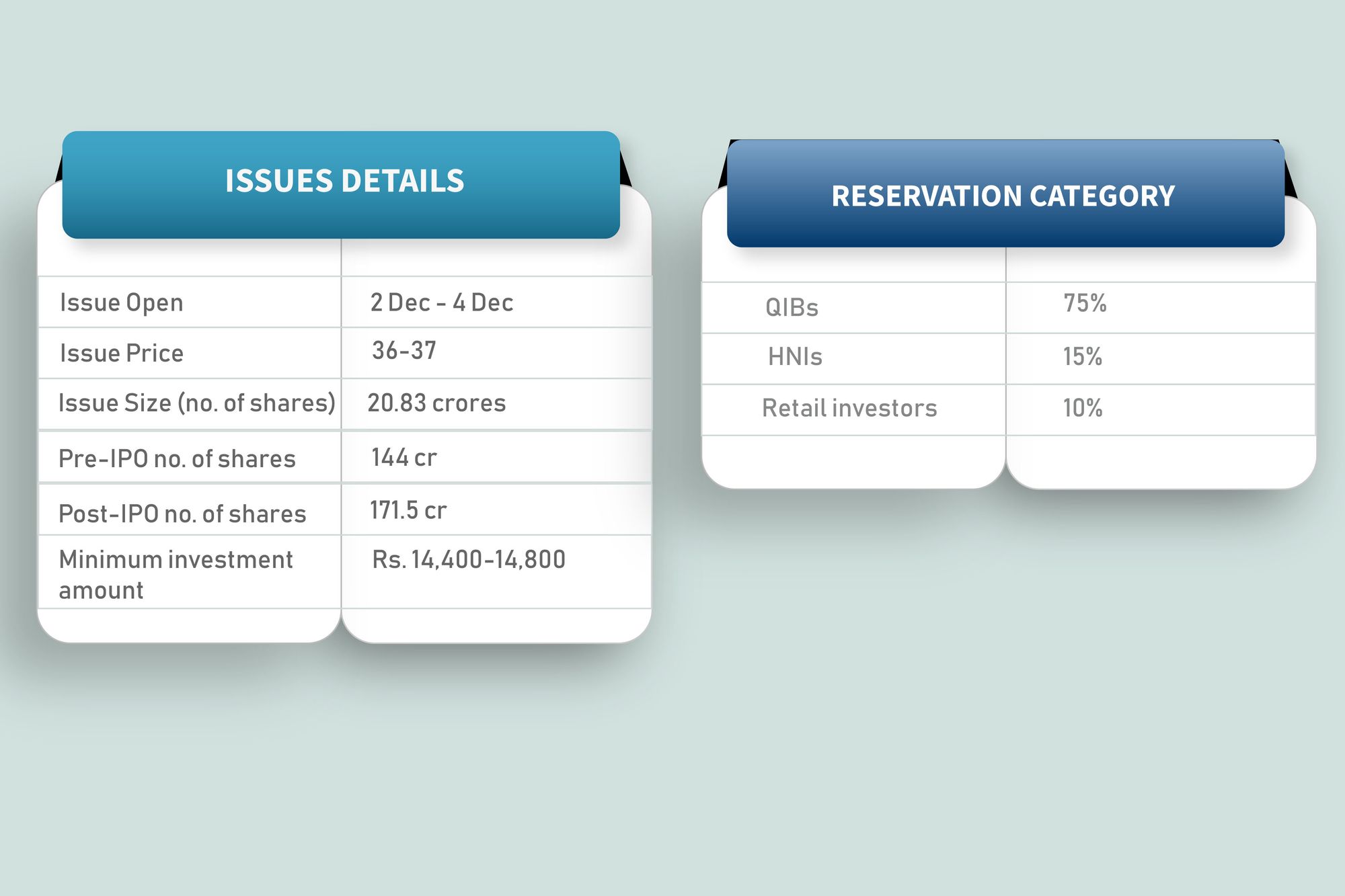

That’s it from us. The issue opens on 2nd December and we wish you the best of luck if you’re planning to make an investment.

Until then… Goodbye, Goodday :)

If you like this story share this on Whatsapp right now or you could Tweet about it :)