The NSDL IPO is here! Is the pioneer still the best in town?

In today’s Finshots, we unpack the NSDL IPO which opens for subscription tomorrow and closes on August 1st.

But before we begin, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

Ask your parents if they ever traded in shares in their twenties or thirties. Go ahead, just ask them.

Because chances are, you’ll hear stories that sound like financial folklore. Stories of calling up a broker, who’d scream orders across a chaotic trading ring, or receiving physical share certificates in the mail that were either forged, stolen or mysteriously lost. Or in many cases, you may hear that they simply never invested because the whole thing felt too risky, too shady.

In the 1990s, this wasn’t unusual. Physical share certificates were a mess, brokers could vanish and scammers like Harshad Mehta thrived in the chaos.

So the government had to fix it. Some folks suggested building a giant vault in the Western Ghats to store all paper share certificates. But that would cost hundreds of crores. Then came a more radical concept: dematerialisation of securities. This could turn paper shares into digital entries. Basically, store them in a computer, not a locker. And it would cost just a sixth of the vault plan! So India ran with it. And in 1996, it became the first country to dematerialise its securities nationwide.

How?

Thank NSDL for that.

Short for National Securities Depository Ltd., it was set up in 1996 with backing from heavyweights like the NSE, IDBI Bank, and UTI. And it quietly built the invisible backbone of India’s capital markets. It digitised everything, made transfers effortless and for four straight years, ruled the roost. Everyone from LIC to banks and mutual funds rushed to it. Then in 1999, BSE launched a challenger — Central Depository Services Ltd. or CDSL. And just like that, India’s depository space turned into a duopoly.

But by then, NSDL had already built its moat. It had onboarded high-value institutional clients, gained more assets under custody and cemented its place in India’s stock market infrastructure.

And to know how it did it, you need to look at NSDL’s business.

At its core, NSDL holds your stocks and bonds digitally, ensures smooth asset servicing when you buy or sell these instruments and enables companies to issue shares in dematerialised form.

But over time, it evolved, and today, its business has three major parts:

- Depository services: The bread-and-butter. Charging companies and brokerages to maintain their shares, transaction charges for share transfers, IPO facilitation fees, and so on.

- Banking Services: Yup, NSDL also runs a payments bank through its subsidiary – NSDL Payments Bank Ltd (NPBL) which was launched in 2018.

- Database Services: NSDL Database Management Ltd (NDML) runs KYC verification, insurance repositories and the National Skills Registry.

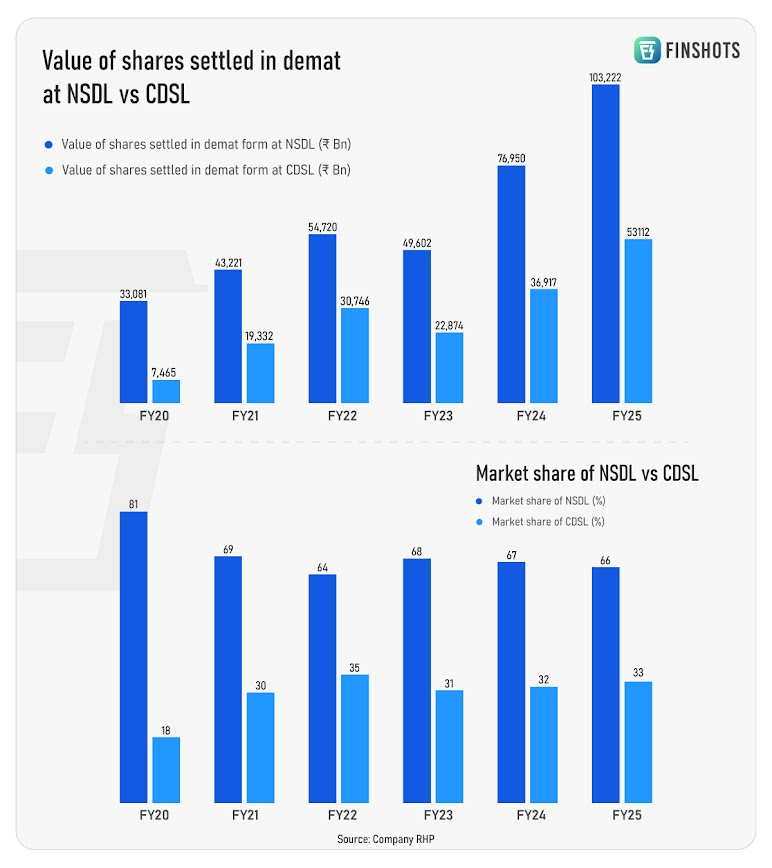

Now, here’s the interesting bit. Although CDSL chipped away at NSDL’s market share over the years, it’s NSDL that still dominates in terms of asset value. To put things in perspective, as of March 2025, NSDL accounts held a whopping ₹464 trillion worth of securities in demat. Or six times more than CDSL’s ₹71 trillion. But… CDSL has more demat accounts.

And if you’re wondering why, well, you can thank COVID.

When the pandemic hit in 2020, retail investors flooded the markets. And discount brokers like Zerodha*, Upstox, Groww became household names. And most of them picked CDSL as their default depository simply because of lower transaction fees, simpler APIs (Application Programming Interface or the bridge that helps connect brokers’ systems to CDSL’s) and faster account opening processes.

The result? In FY20, NSDL had 81% market share (by value of securities settled). That dropped to 69% the next year. And today it’s 66%, with CDSL at 33%.

So yeah, NSDL still holds bigger assets, but CDSL has captured a huge part of the retail game. Even NSDL admits this… “We have in the past experienced a loss of market share in the depository business due to the rapid emergence of new age fin-tech brokers”.

And now, NSDL is heading to the markets with its initial public offering (IPO).

But it’s not raising any fresh money. At the upper price band of ₹800 per share, this is a ₹4,011 crore offer-for-sale (OFS), where existing shareholders like IDBI Bank, NSE, SUUTI (Specified Undertaking of the UTI) are offloading part of their stake. NSDL won’t receive a rupee from it.

And that begs the question: Should you subscribe?

Well to understand it, let’s look at how NSDL earns its money and what moves it.

At first glance, NSDL looks like a classic moaty business. It has 29 years of legacy, trillions in custody and a highly regulated duopoly. But the business has changed from what it used to be in the 90s.

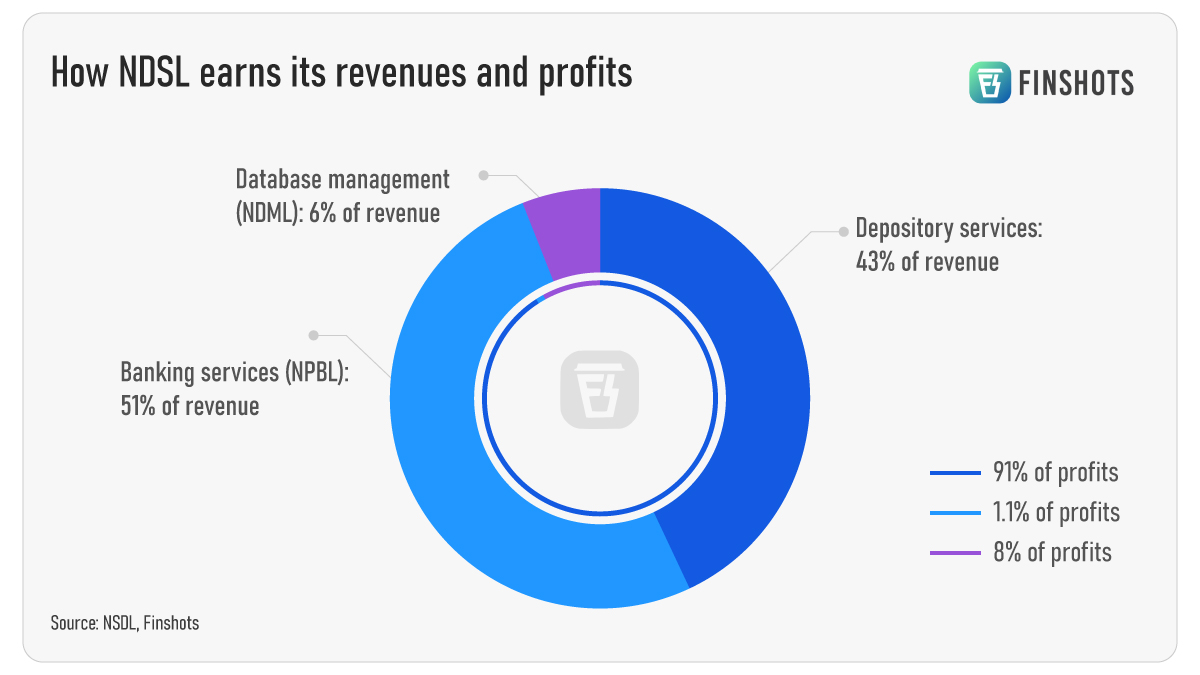

In FY25, depository services made up just 43% of NSDL’s revenues. The largest chunk, or 50%, came from NPBL, its banking services arm, and NDML contributed another 6.3%.

That may sound like good diversification, right? But it isn’t.

Because while banking brings in 50% of revenue, it contributes only about 1% to profits. Yup, that’s not a typo. Meanwhile, depository services, though just 43% of revenue, generate 91% of profits. NDML adds the remaining 6-7%. So, despite all the noise about diversification, the real driver of value is still the depository business.

Hmmm. This skew naturally begs the question: why does the payments segment earn so little in profits?

Because payments banks are low-margin, capital-intensive and face brutal fintech competition (think Airtel Payments Bank or Paytm Payments Bank). And when you look at segmental operating profit margins (OPM), it becomes clearer:

- NSDL (depository) enjoys 50% OPM

- NDML operates at 32%

- NPBL runs at just 0.5%

So if you’re betting on NSDL, you’re betting on this core depository engine to keep delivering.

The good news is that NSDL’s still strong. Standalone depository revenues have grown at 17% CAGR over the past seven years, and profits at 20%. And profit margins have stayed steady at around 45%.

Overall, the company has zero debt and over ₹2,000 crore worth of consolidated net worth.

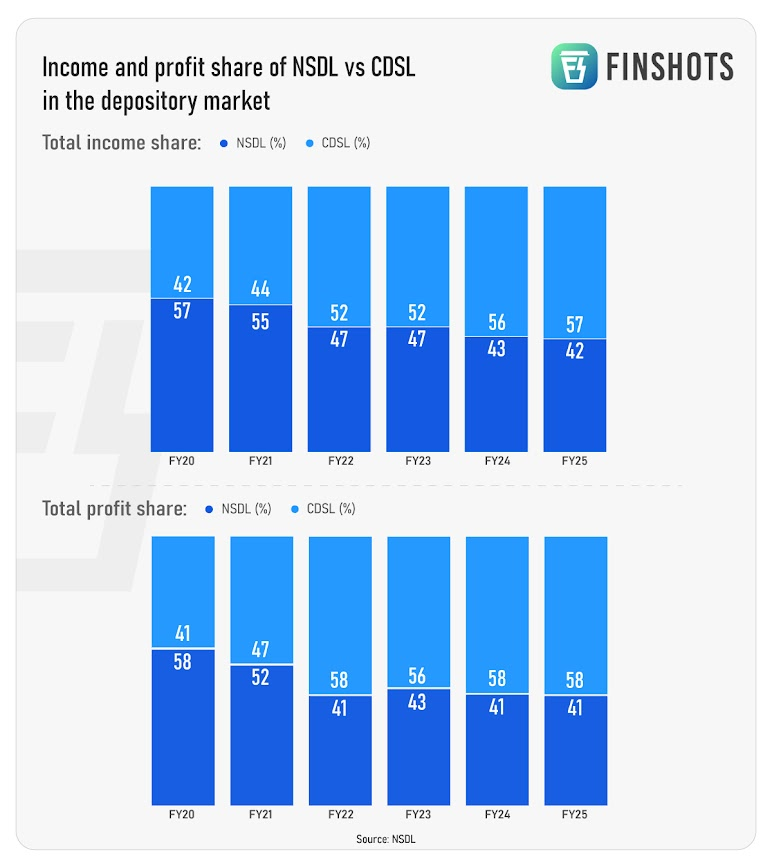

But there’s a subtle shift in the depository segment. CDSL’s revenues and profits here have been outgrowing NSDL’s in the past few years. It’s a signal that CDSL, with its retail-heavy, transaction-rich model, is beginning to lead in pure-play depository growth.

That doesn’t mean NSDL is losing sheen, though. Far from it.

Its future still looks promising as IPO volumes are rising, tier-2 and tier-3 retail investors are entering markets, and e-governance infrastructure (like DigiLocker) is expanding. All of this drives demand for demat accounts and digital recordkeeping, and NSDL is well-positioned to tap into that.

But what about valuations?

We ran some back of the envelope calculations. At the upper price band of ₹800 and an EPS (earnings per share) of around ₹17, NSDL’s IPO is priced at about 47 times its FY25 earnings. That’s noticeably cheaper than CDSL, which trades at a P/E of 68.

But here’s the thing. CDSL’s business is leaner. It focuses purely on the depository space, has ridden the retail boom like a pro and doesn’t rely much on side hustles. So when you factor that in, the valuation gap between the two doesn’t feel all that wide.

So, whether NSDL’s IPO is worth it comes down to a few big bets.

Can it scale up NDML and ride India’s formalisation wave?

Can it turn its banking arm from a cost centre into a growth lever?

And most importantly, can it defend its stronghold in the institutional space while CDSL keeps gobbling up retail market share?

To sum it up, it really depends on the kind of story you want to back.

NSDL built the system, has scale, trust and deep institutional roots. But its banking business is dragging down profitability, and CDSL on the other hand, is lean, focused, riding the retail rocket and is slowly catching up in core depository income.

Also remember, none of the IPO money is going back into NSDL’s business, which means you’re betting on an old-but-evolving infrastructure player in India’s booming capital markets.

So yeah, if you believe retail and institutional participation will keep growing, there’s money to be made in this duopoly.

For now, we’ll only have to wait and see if NSDL can catch up on the growth story.

Until then…

If this story made the NSDL IPO easier to follow, share it with friends, strangers, and anyone with a demat account — on WhatsApp, LinkedIn or X!

*Zerodha, through its Rainmatter Fund, is an investor in Finshots.

🔊Introducing Pitch Perfect 2025!

If you've been following us for a while, you know our story didn't begin in a corporate boardroom. It started in a college dorm room with 3 broke students who chose to skip placements and chase something bigger.

That something was Finshots.

Today, Finshots reaches over 500,000 readers, and through Ditto, we've empowered 800,000+ Indians to make smarter insurance decisions.

Now, we're looking for the next game-changing idea to back.

Introducing Pitch Perfect 2025 – a flagship startup pitch challenge powered by Zerodha.

So, if you've got a BIG idea that could help Indians get better with money, pitch it to us!

What's at stake:

✅₹10,00,000 in prizes

✅Potential funding from Zerodha Rainmatter

✅All-expenses-paid trip to Bangalore to pitch directly to Nithin Kamath and industry veterans

Ready? 👉Apply Now!