The great Indian IT selloff, IDFC Fraud, and more...

In this week’s wrapup, we talk about social media regulation for teenagers, the US Supreme Court blocking tariffs, the ₹590 crore fraud at IDFC First Bank, Adani wanting to bring F1 back to India, and why the RBI is mad at Indian banks.

Also, in this week’s Markets edition, we break down the Indian IT selloff and what you, as an investor, can make of it. You can read it here.

With that out of the way, let’s look back at what we wrote this week.

Can we regulate attention?

What began as a moral panic about teenagers on their phones is turning into policy. Countries like Australia and France are restricting social media access for minors, and India may not be far behind.

You see, the argument is simple: excessive screen time carries real cognitive and economic costs. However, social media is also where young Indians discover opportunities, build careers, and participate in the digital economy.

So regulating attention isn’t just about mental health. It’s about human capital, entrepreneurship, and privacy.

But if India chooses to intervene, will it strengthen its demographic dividend or constrain the very ecosystem it wants to grow?

Find out in Monday’s newsletter here.

Why US tariffs just got slower

The tariffs that hit the world last year took many of us by surprise: the higher duties made goods more expensive and forced both governments and companies to adapt. For India, the stakes were higher because we had relatively higher reciprocal tariffs than most. We just assumed this was the new reality and made changes accordingly.

But that assumption changed when, last week, the US Supreme Court struck down the tariffs, calling them ‘illegal’. Because they were imposed under emergency powers, not meant for long-term trade policy. The judgment didn’t ban tariffs outright, but it made it clear that presidents can’t unilaterally impose indefinite tariffs without Congress’s authority.

What does it mean for the future, the tariffs paid and trade deals that were already signed? We break it all down here in our Tuesday newsletter.

A ₹590 crore fraud at IDFC First Bank!

Cheques may account for less than 3% of transactions in India. Yet one allegedly forged cheque trail managed to siphon off ₹590 crore from the Haryana state government’s accounts at IDFC First Bank’s Chandigarh branch.

But how did something of this scale slip through in the first place?

Because large institutional accounts run on layered approvals and maker-checker systems. Which means such amounts rarely move without multiple eyes on them. So where exactly did it break?

Read Wednesday’s story to understand what really happened, and why this episode may be more important than the headlines suggest.

What would it take to bring F1 back to India?

In 2013, India was at the centre of Formula 1. But quickly after that, the race vanished. Undone not by fans or drivers, but by taxes, legal disputes, and an unsustainable financial model.

Now, with the Adani Group signalling interest, the question isn’t about building a track. It’s about underwriting hosting fees, ensuring tax clarity, and securing a spot on a packed global calendar.

So, what does it really take to bring the sport back to India? Find out here.

The end of forced selling at banks?

Applying for something as important as a home loan has never been easier than it is today. Make a call, open an app or walk down to your bank branch and they’ll have somebody there for you. Background checks are clean, paperwork goes through and everything looks normal, until you notice a complete insurance policy hiding between the fine print.

Banks have long nudged borrowers into buying extra products — especially insurance, when taking out loans, often buried in dense paperwork. Many customers ended up paying for covers they didn’t fully understand or even need, simply because refusing felt like it could jeopardise loan approval.

That’s why the RBI wants to put an end to this grey area starting July this year. In yesterday’s story, we broke down what the new rules are and how they will change the way banks sell to customers going forward.

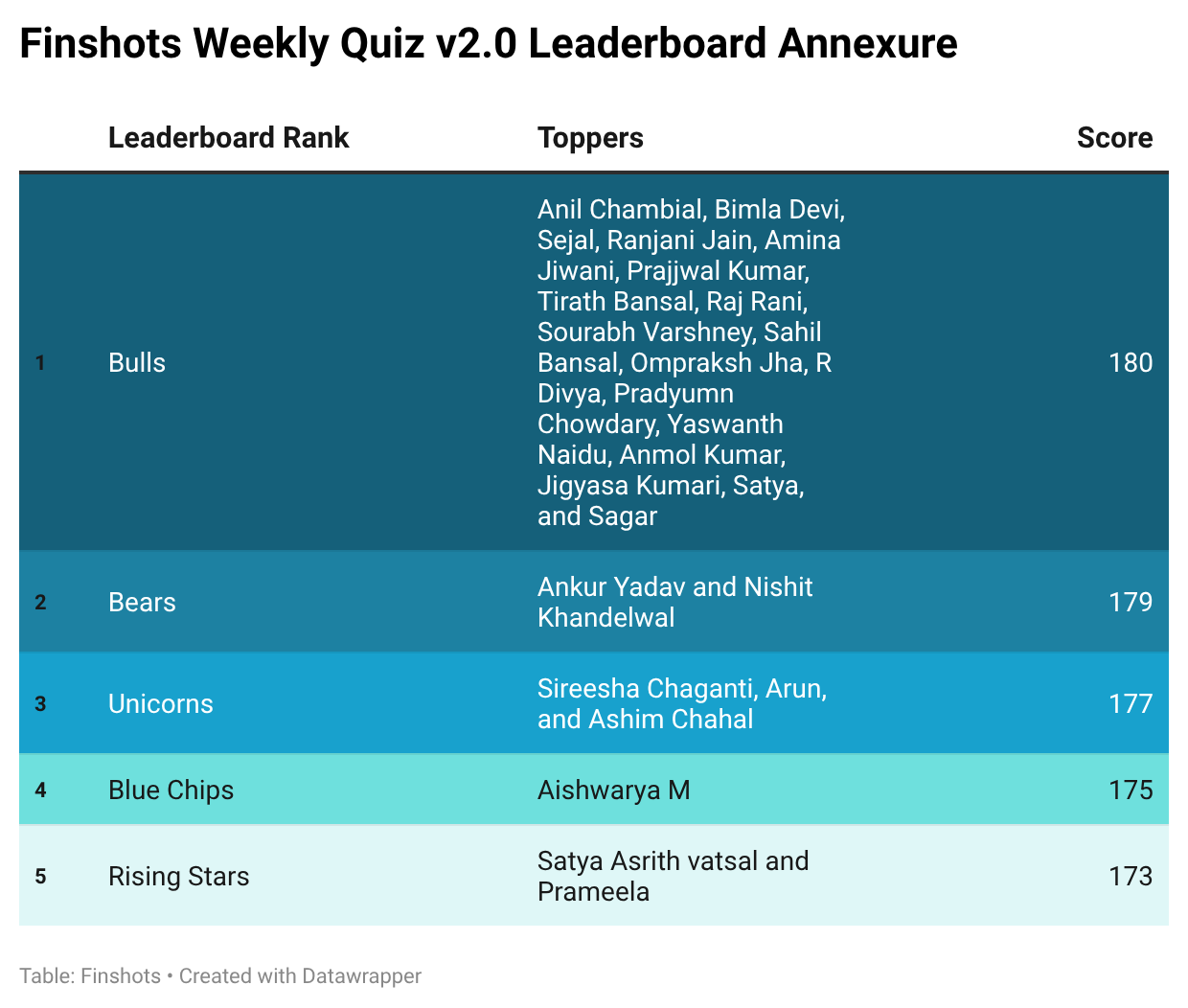

Finshots Weekly Quiz v2.0 🧠

Hey folks! As you probably already know, the Finshots Weekly Quiz has a new avatar. If you missed out on it in the last couple of months, don’t worry. Click here to check out the rules and set a reminder to participate consistently starting next month!

Next, let’s move on to the top scorers from our previous weekly quiz. There were a whole bunch of you who participated, and many of you ended up with the same scores. So we’re calling you Bulls, Bears, Unicorns, Blue Chips, and Rising Stars. Here’s how the leaderboard looks right now:

If your name has been featured on the leaderboard, then congratulations! If not, don’t lose hope. If you attempted last week’s quiz, keep at it and answer all the weekly quizzes this month. You never know when the turntables! Click on this link to take this week’s quiz, which is open till 12 noon, Friday, 6th of March, 2026. The more answers you get right, the better your chances of appearing on the Finshots Weekly Quiz leaderboard. We’ll publish it every Saturday in the Weekly Wrapup. And the winner will be announced next week.

Liked this week’s wrapup?

Don’t forget to share it with your friends, family, or even strangers on WhatsApp, LinkedIn, and X. And subscribe to Finshots, if you haven’t already. Plis!

Myth Alert: I'm Too Young to Buy Life Insurance!

The other day, one of our founders was chatting with a friend who thought life insurance was something you buy in your 40s. He was shocked that it was still a widely held belief.

Fact: Life Insurance acts as a safety net for your family. The younger you are, the cheaper it is. And the best part? Once you buy it, the premium remains unchanged no matter how old you get.

Unsure where to begin or need help picking the right plan? Book a FREE consultation with Ditto's IRDAI-Certified advisors today.