The Economic Survey 2025 explained

In today’s Finshots, we break down India’s latest Economic Survey to see where the economy stands and where it’s headed.

But just a heads up before we dive in. This is one of those stories that’s going to be a bit longer than usual. After all, squeezing a 436-page document into one story takes some extra room. But we promise to return to our short, crisp reads from tomorrow :)

The Story

Let’s start with the economy. As per the survey, India’s economy is staying strong even in an uncertain global environment. And projections say it will keep growing at a rate of 6.3% to 6.8% in the next financial year (FY26).

And while many things contribute to this, the finance sector is one theme that deserves a key mention.

Why? Because banks are giving out more loans and they’re keeping up with the deposit growth. At the same time, banks are making more profits and handling loans better. In fact, bad loans (gross non-performing assets) have dropped to their lowest level in 12 years at just 2.6%.

These factors have propped up financial inclusion, with the RBI’s Financial Inclusion Index going up from 53.9 in 2021 to 64.2 in 2024. And a big part of this growth is happening in rural areas.

But this growth begs a few questions…

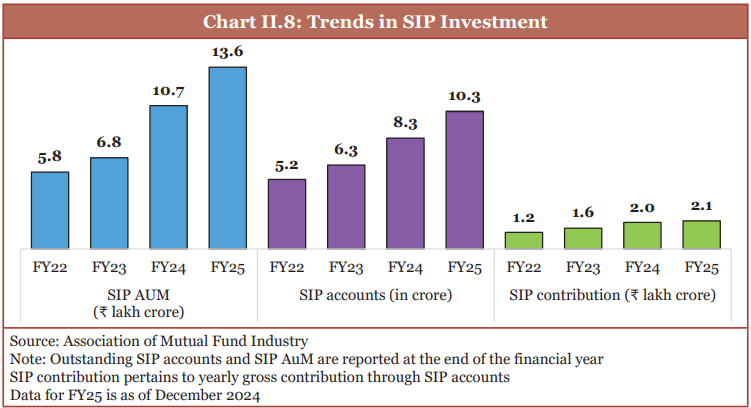

You see, India’s stock market is doing better than many other countries, with record highs and rising retail participation. This has meant domestic savings are finding their way into financial investment products.

Mutual fund’s assets under management (AUM) have crossed ₹66.9 lakh crore, with rise in systematic investment plan (SIPs).

Companies are also raising more money. There were six times more IPOs (Initial Public Offerings) in 2024 than ten years ago. The total money raised through the stock and bond markets reached ₹11.1 lakh crore between April and December 2024, which is 5% more than the full previous year.

However, the influx of investors and a shift in household savings from banks to markets echoes a concern which the survey also raised last year: Are people moving their savings into markets assuming they only go up?

Not only that. The survey warns that financial growth needs to match real economic growth. Because if too much money flows into markets, it also comes with debt. And if debt piles up when prices go up too fast, they can also come down quicker. It mentions research…

Research also shows that rapid financial sector growth tends to favour high collateral–low productivity projects. Often, financial booms are associated with the growth of sectors such as construction, where the collateral is high, but productivity growth is relatively low.

The banking system has its own issues. People are borrowing more, and unsecured loans are increasing. This means more people are in debt, which could be risky. Perhaps that’s why the RBI has been asking banks to set aside more money for risky loans.

And if you add digital lending to this mix, the economy gets huge liquidity gaps which could spell trouble.

So, while growth is great, making sure the financial system stays stable is just as important. That’s the challenge for policymakers today.

But let’s now see what the survey says as to how things are panning out at the ground economy level.

India’s manufacturing sector has been growing steadily. But can it become a global manufacturing hub is the next question the survey mulls at.

And a few stats say why. India’s share in global manufacturing stands at 2.8%, far behind China’s 28.8%. But there’s room to grow. Industries like steel, cement chemicals and petrochemicals have kept industrial growth steady, while consumer-driven sectors like automobiles, electronics and pharma are fueling the next wave. And small businesses are the backbone of India’s industrial economy. While government support through credit schemes is helping, financial constraints still limit their expansion. And that’s why we saw a host of announcements for the MSME sector in the Budget.

But overall, if you take a closer look at the industrial growth, it’s also scattered. Industrial sector grew by 6.2% in FY25, driven by strong electricity and construction growth. But in Q2 FY25, industrial growth slowed to 3.6%, hit by weaker export demand, erratic monsoons and shifting festival sales.

Why these fluctuations? Because the world is also facing major manufacturing disruptions. Geopolitical tensions, supply chain breakdowns, rising commodity prices and a shift in global spending toward services. And India isn’t immune to them.

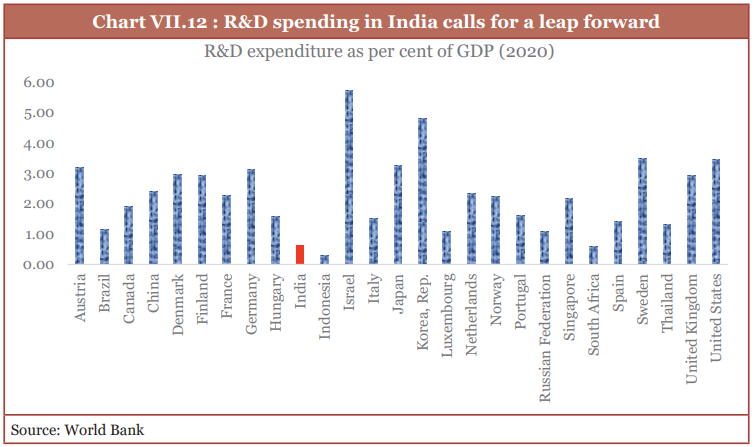

Innovation is also lagging. India’s R&D spending is just 0.64% of GDP, much lower than global leaders like the US and China. Although R&D investment has doubled in the last decade, most of it comes from the government. Private sector involvement remains low.

And these issues are something that the survey points that India should focus on to drive real growth.

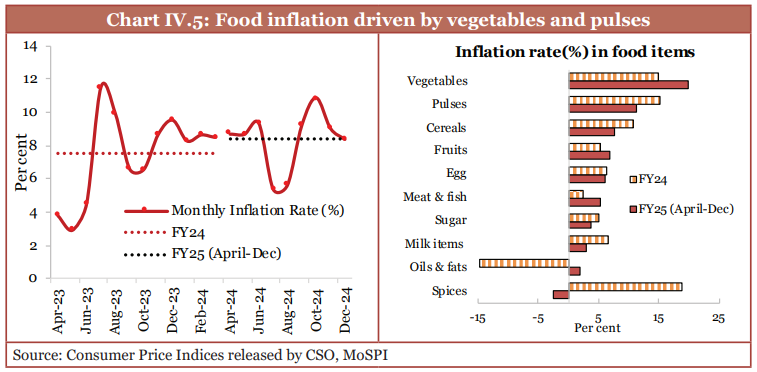

Retail inflation has eased, and core inflation (inflation excluding food and fuel) is at a decadal low. That’s the good part. But food inflation remains a puzzle.

You see, food prices make up for 40% of India’s inflation basket. And even though overall retail inflation has softened, some food prices have seen sharp spikes and thereby tilted the scales. Vegetables and pulses alone contribute about 32% of food inflation in FY25, even though they carry a weight of just 8.4% in the overall index. The main culprits? Tomatoes, onions, and pulses (TOP).

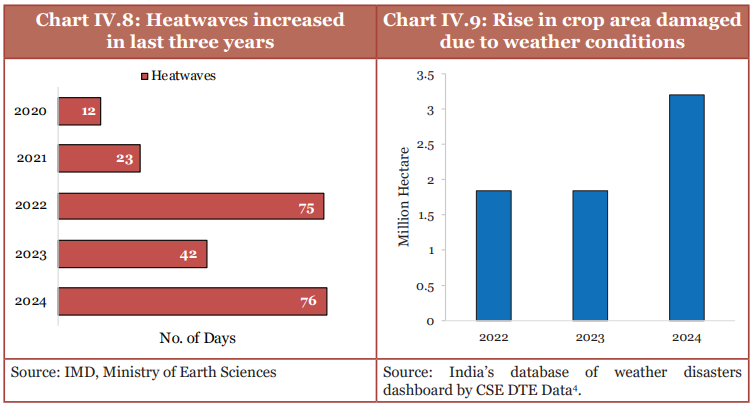

If you’re wondering why, well, erratic weather (monsoons and heatwaves), supply chain inefficiencies and storage issues.

And that’s why the survey proposes robust data systems for monitoring prices, developing climate-resilient crops, reducing crop damage and post-harvest losses - a few things that could help stabilise prices.

It also recommends capping stock limits on pulses and wheat, and ease imports of key food items to stabilise supply.

So the key takeaway here is that inflation may be easing, but the challenge now is balancing price stability with climate resilience.

The survey takes a long, hard look at automation. And the conclusion it draws is that AI won’t replace jobs, it will replace job descriptions. Hmmm…

Take banking. ATMs didn’t kill bank jobs; they just changed them. Today’s bank tellers don’t just handle cash, they sell financial products. And similarly, AI will take over routine tasks, forcing workers to upskill. The only worry?

Many workers don’t have the right skills for the jobs available. This happens because the quality of education varies, and many graduates don’t get the practical skills employers need. The end result is that their degrees don’t always match job market demands, leading to underemployment. For context, about 88% of the workforce are employed in roles below their educational qualifications.

Now, that’s a problem, considering that the job market is shifting faster than our skilling programs can keep up.

The suggestion here is to increase investment in AI skilling, build industry-academia collaboration and rethink labour laws.

The Budget hasn’t ignored this issue either. It’s building on the initiative announced in July 2024 by setting up five National Centres of Excellence for skilling. These centres, backed by global expertise and partnerships, aim to equip young people with the right skills for the right jobs. And with some luck, that could help bridge the skill gap and tackle underemployment.

The Survey acknowledges India’s tricky position. It’s the seventh most vulnerable country to climate change, which is why it’s important to balance economic growth with sustainability. And one highlight here is that India has done a great job adapting to climate change by harnessing renewable energy. But scaling up isn’t easy. We’re short on critical minerals, and our storage technologies still have a long way to go.

And the real deal is that we’ve been funding this transition largely on our own. To put that in perspective, spending on climate change adaptability jumped from 3.7% of GDP in FY16 to 5.6% in FY22.

And to step up, financial support from the developed world could have made all the difference for developing nations like India. But at COP29, those hopes took a hit. The funds pledged to help us tackle climate change fell short by nearly 40%. So, we’re left to figure things out on our own, tweaking targets, reworking strategies and making the most of what we have.

Some solutions are familiar — reducing our dependence on fossil fuels, revitalising waterbodies, recharging groundwater, recycling and boosting green cover. But one intriguing idea is tackling the urban heat island effect, where cities become significantly warmer than their surroundings due to dense buildings and infrastructure. And a creative fix here is vertical gardens!

By turning concrete facades into lush green spaces, these gardens don’t just make buildings look better; they also improve thermal efficiency, absorb carbon and encourage biodiversity; essentially helping cities breathe a little easier. Countries like Singapore, Japan and those in the EU have already embraced this. Even India’s Income Tax Department has experimented with it across 17 states.

If scaled up, this could shape the future of urban planning, making our cities not just more liveable but also more sustainable.

To wrap this up with a few key observations…

The Survey celebrates India’s economic resilience, and rightfully so.

But read between the lines and it throws a sharper question: Can a country aiming for Viksit Bharat by 2047 afford to just play defensive?

While India's structural reforms have propelled it forward, the challenge now is to push the envelope further.

Deregulation remains a key theme and the survey warns that the cost of inaction is not just lost opportunity, but a future where India’s aspirations outpace its execution.

As the preface states…

The Indian economy is on a steady growth path. The macroeconomic health checklist looks good. As the country aims to accelerate its economic growth rate in the coming years, it has the tailwind of strong balance sheets in the domestic corporate and financial sectors. But, globalisation is on the retreat. Hence, raising the growth average in the next two decades will require reaping the demographic dividend through a deregulation stimulus. As the Spartans apparently believed, “the more you sweat in peace, the less you bleed in war”.

And perhaps an important lesson from the survey? It’s that sometimes, the best policy is to simply get out of the way and let ambition take its course.

Above all, underpinning specific policy efforts will have to be the philosophical approach to governance. “Getting out of the way” and allowing businesses to focus on their core mission is a significant contribution that governments around the country can make to foster innovation and enhance competitiveness. The most effective policies governments - Union and States - in the country can embrace is to give entrepreneurs and households back their time and mental bandwidth. That means rolling back regulation significantly. That means vowing and acting to stop micromanaging economic activity and embracing risk-based regulations. That means changing the operating principle of regulations from ‘guilty until proven innocent’ to ‘innocent until proven guilty’. Adding layers of operational conditions to policies to prevent abuse makes them incomprehensible and regulations needlessly complicated, taking them further from their original purposes and intents.

Perhaps that’s where the economy stands…at crossroads. The macro numbers look great. Growth is steady. Investment is flowing. The economy isn’t faltering. But it’s sure waiting to break free.

The question then is: Can India get out of the way of its growth story and take bold steps to thrive in the changing world order?

Until then…

Don’t forget to share this story on WhatsApp, LinkedIn and X.

Can Delhi afford all the freebies?

Delhi is gearing up to elect its new government, and this time, every party — BJP, Congress and AAP, is going all out with freebies!

Free water, free electricity, handing out cash, you name it.

But it got us thinking… can Delhi actually afford all these subsidies? Where’s the money coming from, and more importantly, is this sustainable?

The answer might just surprise you!