The Brightcom saga gets a final verdict!

In today’s Finshots we tell you about how SEBI caught onto the accounting tricks Brightcom Group has been pulling for years.

But before we begin, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

Brightcom Group Ltd (BGL) has been a master of disguise. It has changed names four times, flipped business strategies, and managed to stay in SEBI’s crosshairs without ever really getting caught. And while doing so, it also managed to attract well-known investors, drew the ire of retail shareholders, all while spinning a grand narrative of global dominance in digital marketing (through its three divisions: media marketing, software services, and future technologies).

Yet, despite its shifting identity and red flags, many investors remained hopeful. We even wrote about it a few years back…

But despite all this, there’s a steady group of people who still believe in the gospel of Brightcom — some 7860 members of the “Brightcom Group Investors Group.” They continue to hold great conviction in the company’s prospects and we hope that their conviction pays off.

So, did that conviction pay off?

Well, the stock sits at ₹10 flat (languishing from its high of over ₹100 in 2021), with about 6 lakh retail investors holding over 80% of the company today. And the kicker here is that most of them aren’t invested by choice. The stock is suspended from trading on both the BSE and NSE. And now, SEBI has confirmed what many suspected all along, issuing a final order detailing multiple violations by BGL.

So, let’s break it down.

Violation #1 – Hiding impairment losses

Brightcom’s promoters had a simple trick up their sleeve: tweak numbers, hide losses, and keep the stock price flying high. And from what it seems, they pushed things under the carpet for as long as possible.

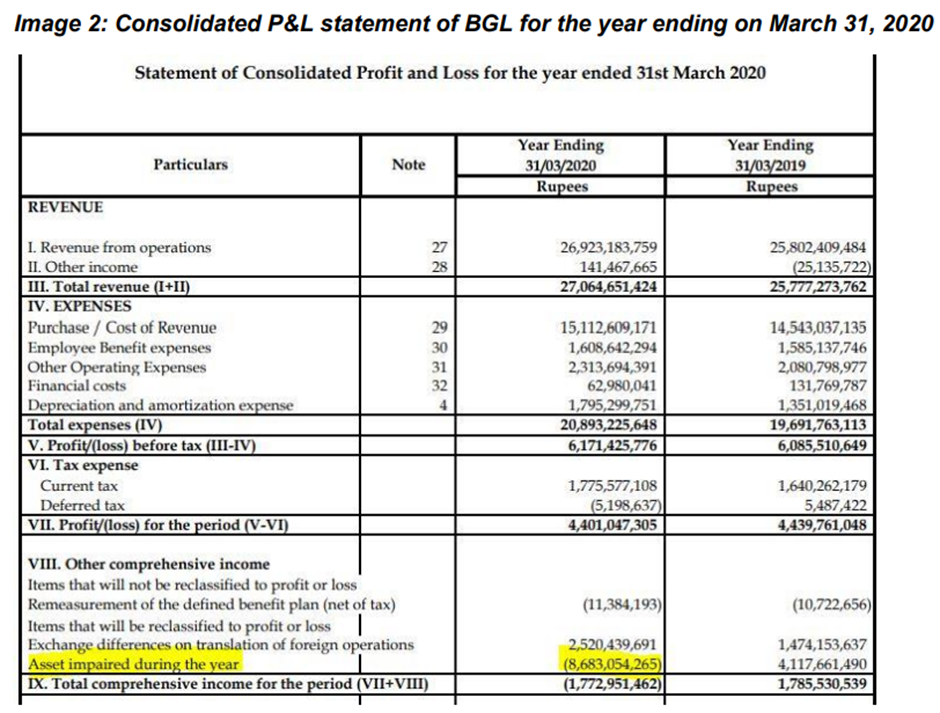

Take impairment losses, for example. When a company realises an asset has lost value and won’t generate the returns it once expected, accounting rules require it to recognise the loss immediately (under Ind AS 36 - Impairment of Assets). These losses should be recorded in the Profit & Loss (P&L) statement to reflect the true value of an asset on the company’s books. And it helps in preventing any inflated valuations on the books that could mislead investors.

Brightcom however had a different approach. From 2016 to 2019, there were signs that assets were turning into dead weight or impaired losses. Did it recognize these losses? Nope. It waited. And waited. Until, suddenly, in 2019-20, it dropped a bombshell: an impairment loss of ₹868.3 crore. Its defence? That it only recognized them when they became ‘permanent’. Or basically saying that ‘we didn’t hide losses; we just didn’t think they were losses yet.’

And instead of placing this loss in P&L (where it would impact the net profits), the company conveniently parked it under “Other Comprehensive Income” (OCI).

Why does this matter? Well, any profit or loss directly affects the reporting net profits—the number investors obsess over. After all, net profit figures are the foundation for key financial ratios and valuation metrics that analysts and investors rely on.

So, had the impairment loss of ₹868 crores been subtracted from net profits of ₹440 crores, the company would have reported a net loss of ₹428 crores instead. And stock prices would have dropped, and investors would have started asking tough questions. But by slipping the loss into OCI, Brightcom managed to keep up appearances. On paper, it still flaunted an after-tax profit of ₹440 crores instead of exposing crores in losses, all thanks to its creative accounting at work. And to an average investor looking at Brightcom’s financials, nothing seemed amiss.

#2 – Misleading shareholding patterns

Now, while these impairment losses were being quietly swept under the rug, BGL’s promoters were also quietly cashing out.

Think about it this way. The promoters knew the books bled losses, not profits. So, before the truth surfaced and the stock crashed, all they wanted was to sell their shares at high prices as quickly as possible. And that’s exactly what they did.

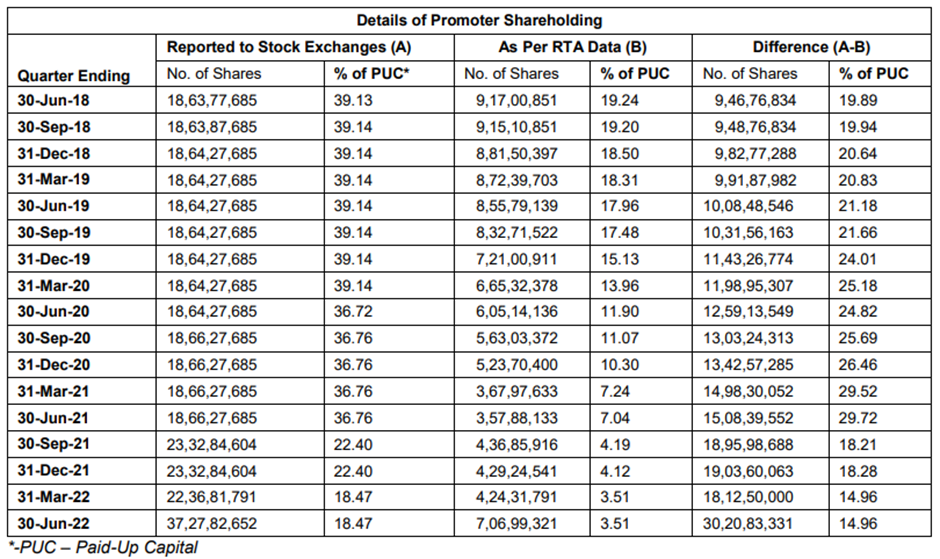

Between 2014 and 2022, promoter shareholding fell from 40% to just 3.5%. Ouch.

Normally, such a massive sell-off would trigger panic. But Brightcom’s stock remained unaffected. Why? Well, because promoters managed to keep retail investors in the dark by misreporting its shareholding.

For instance, as of June 30, 2022, the company reported promoter shareholding at 18.47% on stock exchanges. But SEBI found that the real number was a mere 3.51%:

So what this did was create the illusion that promoters still had skin in the game. And SEBI discovered that Brightcom misrepresented its shareholding pattern in 31 out of 34 quarters between 2014 and 2022. That’s nearly a decade of deception!

But the shenanigans didn’t stop there…

Because there’s also a violation #3 – wrongly capitalising R&D costs

Seems like Brightcom had a knack for playing around with accounting rules. For example, let’s talk about its ₹504 crores worth of Research & Development (R&D) costs in question.

Typically, when a company spends money on R&D, it’s supposed to record it as an expense—unless, of course, that research actually results in a clearly defined product that will generate future revenue. But Brightcom chose to classify its ₹504 crore R&D spend as an asset instead of an expense.

So, instead of reducing profits by ₹504 crore (as it should have), Brightcom boosted its balance sheet with a shiny new “asset” by capitalizing it. Profits were up by ₹504 crores. Assets went up by ₹504 crores. But in true sense, it should have been ₹504 crores in expenses subtracted from profits.

Investors looking at the financial statements thought, “Wow, this company is doing great! Profits are strong, and their assets are growing!” But in reality, it was just shifting expenses around to make things look financially healthier.

And that brings us to another similar violation that BGL pulled off which is…

#4: Incorrect reporting of intangible assets

When a company develops an intangible asset, like a new technology or patent or a proprietary software, it must decide whether to treat this cost as an expense or capitalise them as an asset.

And accounting rules have a clear say here - if the asset isn’t generating revenue yet, the costs should be expensed immediately in the P&L. But if it’s already generating revenue, it can be capitalized on the balance sheet as an asset. And misclassifying these costs (i.e. either recognizing them too early or too late or treating an expense as an asset) can distort the true financial position.

For instance, if you spend ₹100 on developing a software today which isn’t ready yet, it should still be recorded as an expense in the P&L. But if you call that ₹100 an “intangible asset”, it sits on your balance sheet instead, making it seem like you’ve built something valuable which is already generating revenue.

And what did BGL do with its intangibles? Well, it delayed recording them as expenses and instead lumped everything into “intangible assets” at the end of each year or even the next year.

As the order states… For example, in FY 2015-16, the additions to “Intangibles under Development” and “Capital Work in Progress” were INR 102 crore and INR 70 crore respectively and this was reflected in FY 2016-2017 “Intangible Assets” as addition of INR 172 crore. (This pattern is seen across all financial years except in the case of FY 2014-15)

And this changed things by giving promoters complete control over when and where these assets appeared on financials. Instead of letting costs impact profits as they occurred, they could show them as assets at key moments…say before raising funds from any investors or during quarterly result announcements.

So yeah, by now you would know that anyone glancing through BGL’s financials was being taken for a ride, year after year.

And while SEBI pointed at these violations, Brightcom had an explanation for everything. On fudging shareholding data, it claimed that the transfers were done legally and just part of corporate restructuring. On R&D costs, it insisted that it was simply following industry norms. And regarding intangible assets, it brushed it off as a timing issue for operational alignment.

But well, SEBI wasn’t having any of it and slammed them all with detailed explanations.

And that brings us to the question - What happens now?

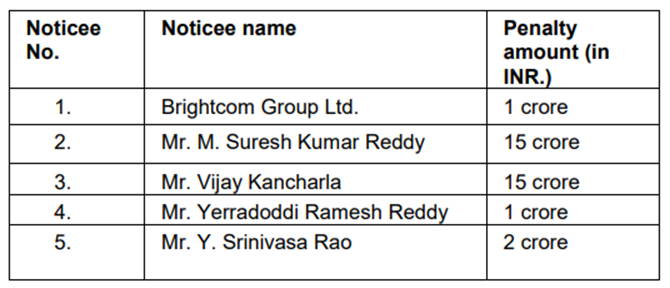

Well, the company and its promoters are barred from the stock market and have been hit with penalties. However, many believe the penalties seem oddly light—the promoters allegedly misrepresented hundreds of crores and benefitted from it while facing just ₹34 crore in fines.

But as the order points out that the promoters are at more stringent penalty than the company itself…

Finally, in my view, Noticee No 1 (BGL) deserves comparatively lesser penalty and period of restraint for the reason that it is now largely owned by public shareholders who have borne the brunt of the fraud perpetrated by the promoter directors.

And it has also outlined for what might come next...

SEBI shall determine the quantum of illegal gains/ benefit made by way of the fraudulent scheme as established in this Order and action may be initiated in accordance with law.

As for retail investors stuck with Brightcom shares, the stock remains untradeable, and there's no telling if or when it will relist.

In response, BGL recently held an AGM and offered some vague assurances. As per the AGM minutes…

“The company’s legal team is reviewing the order in detail.” … “The company remains committed to transparency and will continue to provide regular updates as and when appropriate.” … “The exchanges will notify the company and shareholders as soon as they are ready. We will keep the community informed as soon as there is clear visibility on the relisting timeline.”

Uh oh. In short, it's asking investors to sit tight and hope for the best.

And there’s also a bigger issue at play here. You see, Brightcom was once a part of the Nifty Alpha 50 index. Meaning many mutual funds and ETFs had exposure to it. And as a result, this simply means that countless passive investors unknowingly held its shares through these funds.

Nevertheless, this story also is for anyone who isn’t a shareholder in the company.

Despite numerous warning signs, many investors held on, convincing themselves they had found an undervalued gem backed by big names. But when a stock is littered with fraud allegations, it pays to question every assumption before betting small or big.

And perhaps the biggest takeaway? If you ever find yourself thinking “Why am I so lucky to have found this once-in-a-lifetime opportunity?,” it’s worth considering that you might just be missing something.

For Brightcom investors and shareholders, that moment of realization came far too late.

Now, all they can do is wait, hoping the stock will trade again someday so they can finally cut their losses. And we can only hope that day comes sooner than later.

Until then...

Don’t forget to share this story on WhatsApp, LinkedIn and X.

Only 17% of millennials have a term plan❗

Here’s why getting a term plan early can do wonders for you & your family:

✅Protection: Simply put, term insurance is where you pay a small amount of money in exchange for a large amount of protection. This protection usually kicks in in the event the policyholder passes away.

But not just that, if you ever develop a critical illness (eg. cancer) and have to quit your job, a term plan can give you a lump sum amount to make up for the lost income.

✅Secure Your Parents: As your parents near retirement, they may start to rely on your income. And so, a term plan will give you peace knowing that they'll be financially supported even in your absence.

✅Low Premiums Forever: A term plan of ₹1 crore will cost you much lower premiums at 25 years than at 35. You can even get a ₹1 crore cover for as little as ₹10,000 a year if you are young and healthy. Plus, once these premiums are locked in, they remain the same throughout the term!

So don’t delay it! As they say, “The best time to buy term insurance was yesterday; the next best time is today.”

Click here to book a FREE call with Ditto Insurance’s certified advisors and get your personalised term insurance guidance.