Sunny Side Up 🍳: Dhobis in malls & The Everything Goes to Sh!t Financial Plan!

Hey folks!

Remember the meme from 2016 that went viral because someone scribbled “Sonam Gupta Bewafa Hai” on a ₹10 note?

We ask because the chatter around ‘scribbling on notes’ is back. There’s a message doing the rounds that’s causing some panic. It claims that writing on banknotes could make them invalid.

And the Press Information Bureau stepped in and did a quick fact check. It said that a few scribbles on a banknote wouldn’t strip it of its legal tender status.

But hey, that shouldn’t encourage anybody. Scribbling can deface a banknote and reduces its shelf life. That means more soiled notes and higher currency printing costs for the central bank.

Which is why former RBI governor, Dr Bimal Jain introduced a ‘Clean Note Policy’ in 1999 to suck out soiled notes from circulation and issue fresh or clean notes. 2 years later the RBI even urged banks to use bands instead of stapling notes to increase their life.

So, although the viral message turned out to be fake, the intentions behind it probably weren’t! Using crisp and clean banknotes is a different feeling after all.

Don’t you agree?

Here’s a soundtrack to get you in the mood 🎵

Dreaming In My Mind by Jaden Maskie

Have you poured yourself a hot beverage yet?

Let’s get started!

What caught our eye this week 👀

You can now take your chores to a mall!

What would you do if you had just a one-day weekend and had to shop, but also do stuff like laundry and get a haircut?

If I were you, I’d first do the chores and check in to a salon. After that, if I had any time (thank you traffic) and energy left, I’d probably think about stepping into a mall. Or maybe just postpone my shopping plans.

But what if malls offered a whole host essential services and you didn't have to hop from one place to another? It would be quite the life-saver, no?

Well, some mall operators have caught on to this idea. And they’re diversifying their tenants now. They’re roping in tailors, cobblers, pet groomers, launderers and even pop-up health labs so that people don’t skip mall visits and run helter-skelter to finish their errands.

Now it’s not a selfless cause, of course. They’ve realized that they need to innovate and keep up with the times.

See, mall operators earn their rents these days in either of these two ways.

1. A fixed fee is charged from the tenant. So they’ll make money irrespective of whether stores make good sales or not. But if malls don’t woo customers and sales remain flat, then there’s a high chance of brands closing down their mall stores. The mall could turn into a ‘ghost’ mall — with low footfall and high vacancy. And they’ll lose revenue.

2. A revenue-share model. If the stores do well, the mall operator can pocket a bigger fee. So if people reduce the time spent in malls because they’ve got other places to be, it can dampen sales or at best, it’ll stagnate. And the money doesn’t pour in either.

So by giving everything under one roof, they’re simply trying to get people to spend more than the typical 2-3 hours at the mall. More time at the mall = more money being spent = more revenue for the mall operator!

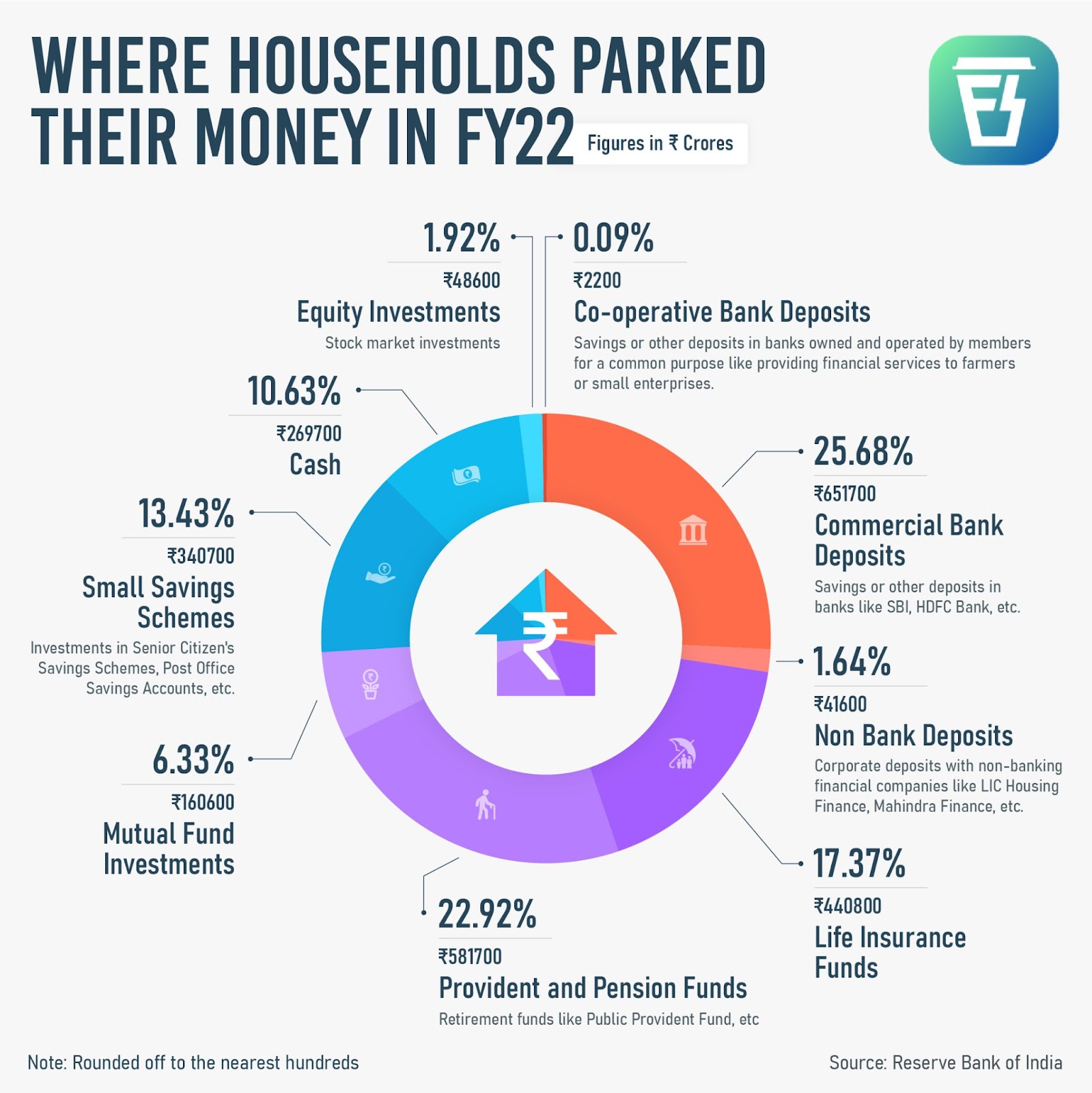

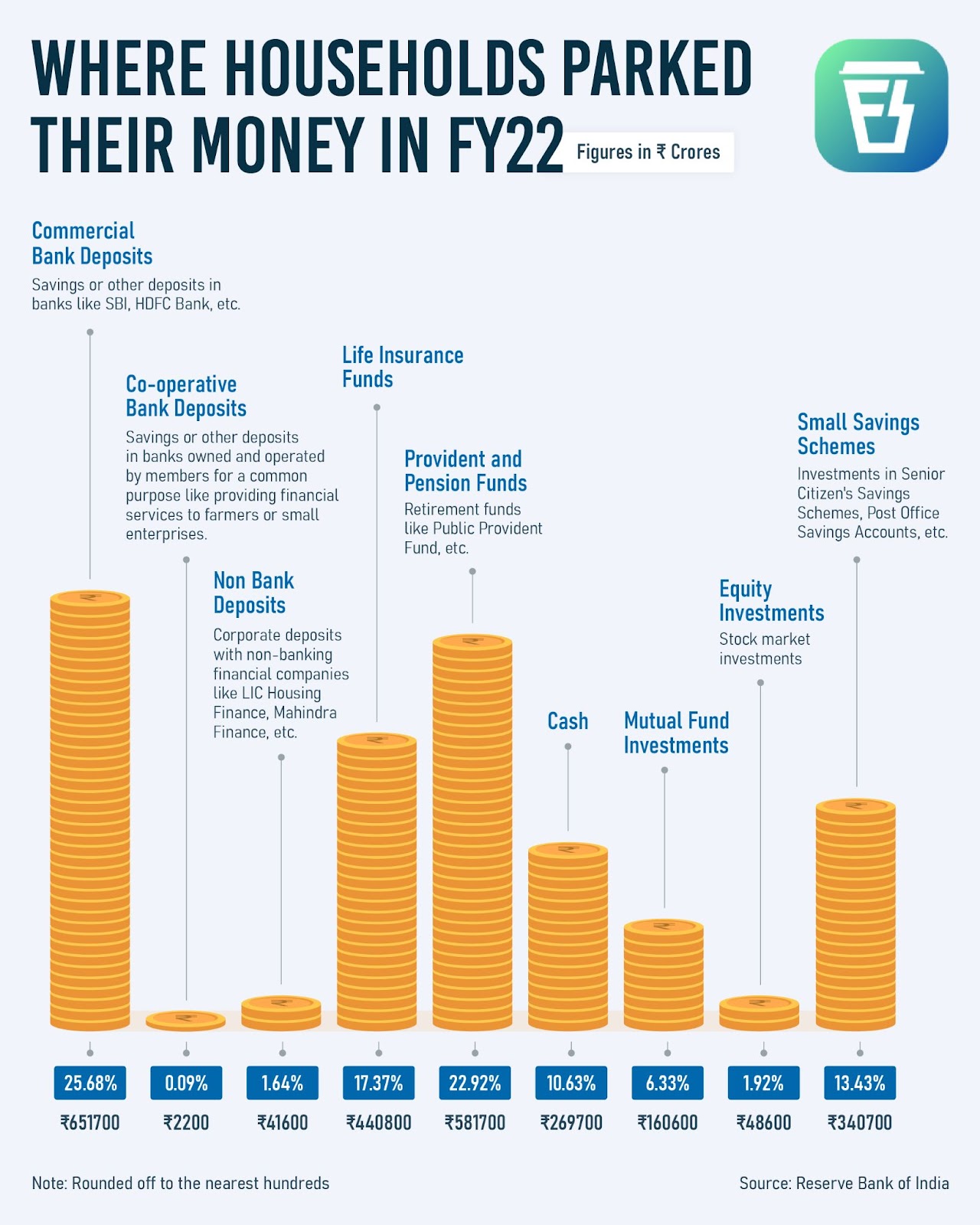

Infographic 📊

Quirkonomics 💸

The Diamond-Water Paradox aka the paradox of value

What if we told you that we’re doing a Finshots giveaway of a diamond solitaire?

It’s obviously a hypothetical scenario. But didn’t it thrill you for a moment?

Now imagine that we told you that we’re giving away a bottle of mineral water. How would that make you feel? Meh, we’re guessing.

And that’s probably to do with how expensive diamonds are. But have you ever thought why the inconsequential diamond is costlier than a life-saving liquid like water?

Well, Adam Smith (the father of modern economics) did. In 1776, he pondered over this conundrum in his book An Inquiry into the Nature and Causes of the Wealth of Nations. And he couldn’t quite put a finger on it.

Economists tried to explain it using various theories. Such as the labour theory. Meaning, the more labour it takes to produce something, the pricier it is. After all, water was available in abundance. In streams, rivers, everywhere. Whereas diamonds were rarer, they were deep underground and hard to get. You needed more manpower for the job. So diamonds naturally were more expensive.

But not everyone was convinced. Because there were places where even water was rare. Like the deserts. So why didn’t water prices reach stratospheric levels in the desert?

Well, it took 100 years, but Alfred Marshall finally cracked the paradox and put the debate to rest. He said it’s not the absolute level of utility of the product but rather the diminishing marginal utility which matters.

In simple terms, the first litre of water is precious. It will quench your thirst. But what will you do with another 5 litres of water? You could store it for use but the more water you have, the less you start valuing it.

But that’s not the case with diamonds. Each additional diamond has the same allure. No one says no to the extra bling. You put this and its scarcity together and boom, you have a high price!

So yeah, that’s the Diamond-Water Paradox for you in a nutshell.

Money tips 💰

The ‘Everything Goes to Sh!t’ Financial Plan!

When the good times are rolling, we just think life’s going to be a bed of roses every day. But one day, reality strikes — you hear terms like recession, layoffs, and funding winter being bandied about. And you think — maybe the job isn’t so secure after all.

The question is — do you have a plan B if the worst were to happen? How can you trim down your bloated spending habits?

That’s why you need the ‘Everything Goes to Sh!t Financial Plan!’ Think of it as a survival pack you’d need in case of a zombie apocalypse. You use it only in the direst situations.

Step 1:

What’s the bare minimum amount you need to survive each month? I’m talking only about the essentials. Things like housing, groceries, and utilities. Salaries to your cook and house help don’t fall into essentials. You can make do without them. You can cancel your Netflix subscription too. Just the bare minimum.

Step 2:

Get your healthcare situation in order. Everyone relies on health insurance provided by the employer. But when you’re laid off, that disappears. And it’ll be the worst time to make a trip to the hospital. You can rack up a hefty bill pretty quickly if you have to visit the doctor and it can wipe out any savings you have. So make sure you have substantial health insurance coverage. And if you don’t, please schedule a call with my colleagues at Ditto Insurance ASAP!

Step 3:

Start building your emergency fund. If your monthly expenses are ₹50,000, start by saving up towards that amount first. Gradually, increase that to a point where you have at least 6 months' worth of these expenses in your bank account. It should be readily accessible. And it’s okay if it doesn’t earn you sky-high returns. The purpose is safety. Just so that you can sleep well at night.

Oh, and be honest about what you’re trying to achieve. If your friend calls you and says, “Hey, let’s go on a trip,” and you’re trying to shore up your emergency fund first, let them know. Maybe even convince them to get their finances in order first. Once it’s set, you can take your holiday in peace knowing that you’re in a financially sound place!

Do these 3 things first and you’ll breathe easier.

Readers Recommend 🗒️

Liner - a web productivity extension

This week we picked an amazing recommendation from our reader Mehak Jain. Liner is a browser extension that lets you highlight anything you see online. Be it articles, images or even videos! The extension saves everything you highlight in a folder so that you can look at it later, all in one place.

“You can also pinpoint time stamps of any YouTube video via it. It’s very handy and convenient and a great tool for research.” she says.

Thanks for the tip Mehak. That’ll surely help us when we’re researching for our stories and we hope our readers find it useful too.

***

With this, we’re wrapping up this edition of the Sunny Side Up.

We hope you enjoyed it.

Don’t forget to tell us what you think and send us your book, music, business movies, documentaries or podcast recommendations. We’ll feature them in the newsletter! Just hit reply to this email (or if you’re reading this on the web, drop us a message: morning@finshots.in).

We’ll be back next Sunday!

Until then...

Don't forget to share this edition on WhatsApp, LinkedIn and Twitter