Mutual funds gifting, IPL valuations and more...

Hey folks!

There is a quiet ritual that plays out every Diwali, every birthday and every wedding anniversary across India. Someone hands over an envelope. Inside is cash or a gift card for Amazon or Myntra. It gets spent, sometimes wisely, sometimes on something forgotten by the following month. SEBI, it turns out, has been thinking about this moment too.

Last week, India's markets regulator released a consultation paper proposing something that sounds almost too obvious once you hear it: the ability to gift a mutual fund. Not advice or a nudge. An actual, ready-to-use prepaid card that someone can walk away with and use to begin their investing journey.

The process is quite simple. Someone, be it a parent, an uncle or a friend buys a Gift PPI, short for Prepaid Payment Instrument, through standard banking channels. It looks and works like a gift card. They hand it to whoever they have in mind. That person then logs on to an asset management company's website, claims the card, picks a mutual fund scheme they like, and the money goes straight in. Any returns, when they eventually come, land only in that person's own bank account. No shortcuts, no workarounds.

The idea came from AMFI, the mutual funds industry body, and SEBI has taken it seriously enough to open it for public comment until April 14. The regulator's own words in the paper are telling: the Gift PPI, it says, is "expected to improve financial inclusion through onboarding of new investors in the mutual fund space."

Now we know what you’re thinking: What if the receiver just withdraws it and decides to get a little naughty?

Well, that’s why the safeguards built around it are intentionally tight. Each card can hold up to ₹10,000, cannot be reloaded, and cannot be used to withdraw cash or shift money anywhere other than a mutual fund scheme. If the card goes unused, the amount is refunded to the buyer after one year.

There is also a broader ₹50,000 annual limit per investor across all such prepaid routes, and only money loaded through debit cards, net banking, or UPI can be used — no credit balances, no cashback, no promotional credits.

Perhaps the most thoughtful detail is this: while the giver can suggest a fund, the final choice rests entirely with the recipient. SEBI has been careful to ensure that no part of the transaction is treated as investment advice. Plus if you’re starting your investment journey, why not do it by making your own choices?

What SEBI is really proposing is a change in how people first encounter investing. Gifting stocks, of course, is not a new idea. Families have been transferring shares for generations, and platforms have made it relatively straightforward.

But that world has always required the recipient to already have a demat account, a broker, and some basic understanding with how markets work. It assumed someone who was already, in some sense, inside the system. A gift card changes the entry point. It hands someone a reason to start, without demanding much.

India has hundreds of millions of people who save but do not yet invest. For some of them, all it might take is the right gift at the right moment.

Here's a soundtrack to put you in the mood…

Gungunaya by Tvasthaar

You can thank our reader, Shivansh Jhalani, for this recommendation. And if you’d like your music recommendation featured too, send them our way, especially hidden gems from underrated Indian artists many of us haven’t discovered yet. We can’t wait to hear them!

What caught our eye this week

Why an IPL Team Costs More Than Most Companies

Royal Challengers Bengaluru just sold for $1.78 billion. Around the same time, Rajasthan Royals changed hands at $1.63 billion.

RCB makes roughly ₹700-800 crore yearly in revenue. This amounts to how buyers pay almost 20-22 times the franchise’s annual revenue. For context, even the hottest tech companies rarely trade above 10-15x revenue. An average FMCG company may trade at 3-5x. So on a spreadsheet, this looks absolutely bonkers.

But here’s the thing. Sports teams aren’t business. They’re closer to a sea-facing penthouse in Bandra or a rare art piece at an auction. They are scarce, desirable, and priced by what the richest person in the room is willing to pay. With just 10 IPL franchises and a whole lot of billionaires, the math does the heavy lifting.

The revenue model is something quite fascinating to look at. Unlike a regular business where one hustles to build a top line, about 70-75% of an IPL team’s income comes straight from the BCCI’s central pool. We’re talking about broadcasting deals, league sponsorships, and more which are split among the franchises. This is less like running a startup but more like buying a toll booth on a national highway because the cars will keep coming, regardless.

This also explains something curious about the RCB and RR acquisition deals. RCB’s brand value is $269 million while Rajasthan Royals’ stands at nearly half of that amount, at $146 million. Yet, the sale prices are only about $150 million apart. RCB just won its first championship in 18 years while RR is a veteran champion. The valuations, sort of don’t make sense. But why so?

Well, because brand value is the icing but not the cake. When the bulk of your revenue comes from the central pool, having Virat Kohli as your star power might be a bonus but never the foundation.

There’s also a structural advantage the IPL has over leagues like the English Premier League. In the EPL, one bad season can send you tumbling into a lower division and your valuation crashes overnight. The IPL doesn’t have such a relegation system. It’s a closed league, much like the USA’s NFL and NBA. This safety net makes IPL teams fundamentally more predictable as investments.

Nobody buys an IPL team just for its annual profit. In fact, most teams barely break even operationally. However, the real return is appreciation. IPL teams went from roughly $100 million in 2008 to $1.6-1.8 billion today. That’s about 18x in 18 years!

This is better than most mutual funds, plus you get a front row seat at the stadium.

So, with valuations soaring past what any Excel model can justify, is this the smartest bet in Indian sports? Or are we watching a bubble that only looks obvious in hindsight?

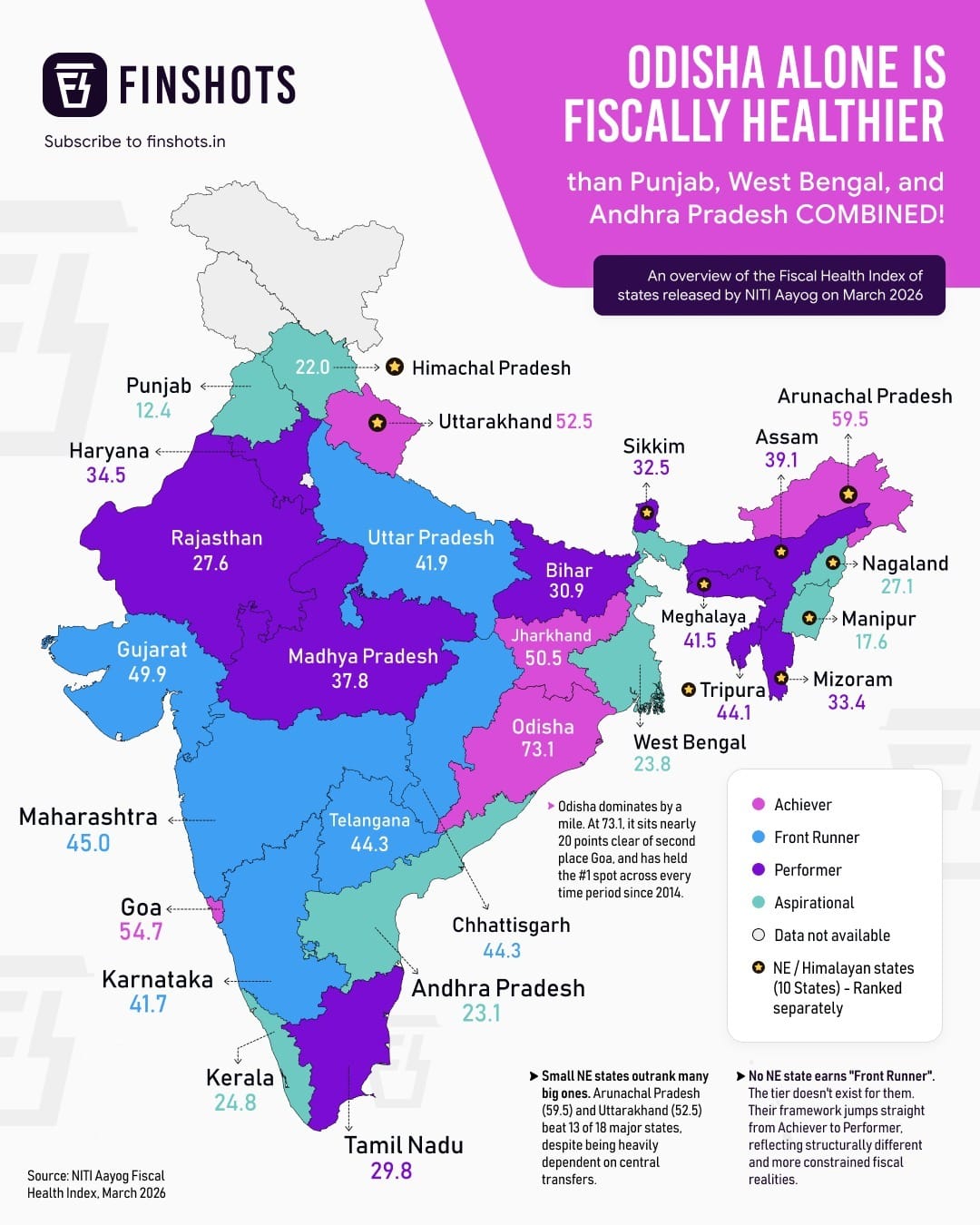

Infographic

NITI Aayog's Fiscal Health Index 2026 paints a picture of stark contrasts across Indian states. Fiscal health isn't just about numbers. It shapes how well a state can deliver schools, hospitals, and roads to its people.

Readers Recommend

This week’s book recommendation is The Silent Patient by Alex Michaelides, recommended by our reader Neha Sharma. The book tells the story of a criminal psychotherapist who becomes obsessed with uncovering the motive of a famous painter who shot her husband dead and has since refused to speak.

Thank you for the recommendation, Neha!

That’s it from us this week. We’ll see you next Sunday!

Until then, send us your book, music, business movies, documentaries, or podcast recommendations. We’ll feature them in the newsletter! Also, don’t forget to tell us what you thought of today's edition. Just hit reply to this email (or if you’re reading this on the web, drop us a message at morning@finshots.in).

Don’t forget to share this edition on WhatsApp, LinkedIn and X.