Is the Unified Pension Scheme any better?

In today’s Finshots, we dive into the newly proposed Unified Pension Scheme (UPS) and the tug-of-war it's causing.

Recently, Finance Minister Nirmala Sitharaman stated that the UPS strikes a balance between the interests of government employees and taxpayers. Meanwhile, government employees are protesting across states for a return to the Old Pension Scheme (OPS).

So, we tell you what’s all the fuss about and how it can affect you.

But before we begin, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

There are three big reasons why pensions matter to everyone in India.

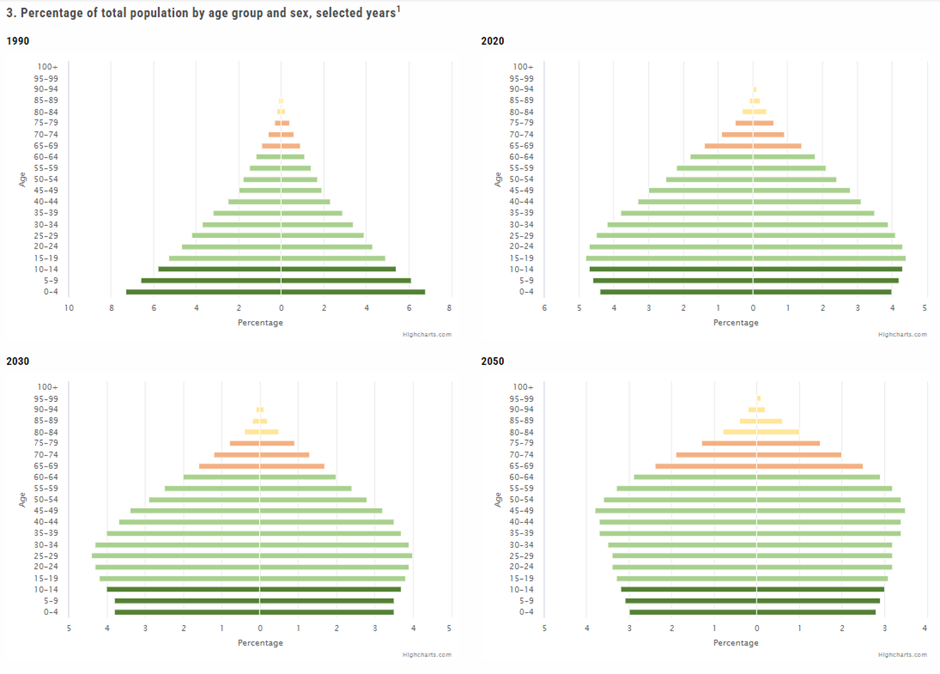

First, India’s retiree population is growing rapidly. Life expectancy, which was just 35 years in 1950, has risen to 67 today, and it’s expected to increase further by 2050.1 More retirees mean a heavier pension burden.

Second, government employees are entitled to pensions, and this affects you—the taxpayer. Why? Because pensions are funded by the taxes we pay.

In March 2023 alone, there were 6.8 lakh central government retirees receiving pensions, along with hundreds of thousands of other pensioners from sectors like telecom, postal services, and railways.2 And guess where all that money comes from? Our pocket.

Now, you could argue that these pensions aren’t entirely funded by taxes, since employees also contribute through salary deductions. And you’re right. But you have to remember that those salaries are paid from government coffers or the money collected through taxes. So, in the end, the entire pension pool is still funded by public money.

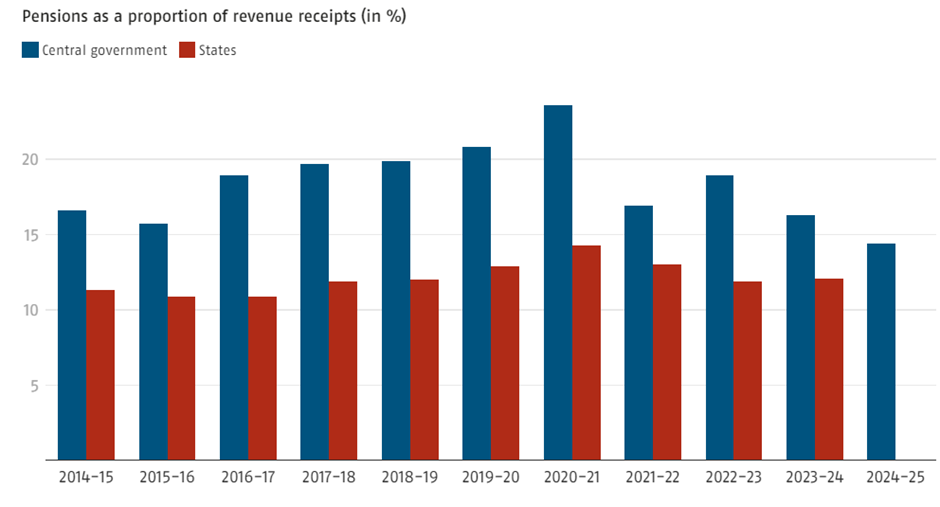

Third, India spends a lot on pensions. At least 15% of both central and state expenditures go toward pensions, leaving less room for infrastructure development and social welfare.

This brings us to the perennial question ― How do we ensure the financial security of a growing retiree population while keeping costs low?

Well, the government asked the same question and to solve this it has experimented with various pension schemes over the years.

First came the Old Pension Scheme (OPS), where government employees didn’t contribute a rupee to their retirement. They received up to 60% of their last drawn salary, adjusted for inflation via Dearness Allowance (DA). It was great for retirees but terrible for the government’s finances. In fact, an Economic Times analysis says that by FY22, over a quarter of state tax revenues went towards pension payments under this scheme.3

To fix this, the National Pension System (NPS) was introduced in 2004. This market-linked plan required employees to contribute 10% of their salary, with the government matching it with 14% contribution. NPS was intended to be a more sustainable solution. But many government employees were unhappy because their pension payouts under NPS were much lower compared to OPS. Some states, like Rajasthan, even reverted to OPS due to political pressure from employee unions.

That’s when the government introduced the Unified Pension Scheme (UPS), scheduled to launch in April 2025. UPS aims to combine the best features of OPS and NPS. The government claims it’s a solution that balances fiscal responsibility with social security.

And this is crucial because around 23 lakh central government employees are said to be eligible for UPS in 2025.

So, here’s why UPS is said to be a gamechanger…

The UPS aims to offer the best of both worlds. It guarantees a pension like OPS but requires employee contributions, similar to NPS. Government employees contribute 10% of their basic salary, and the government adds a generous 18.5%.

At retirement, employees receive 50% of their average basic salary drawn over the last 12 months before retirement. Plus, UPS offers inflation adjustments, so retirees aren’t left at the mercy of market fluctuations. This fixed, guaranteed pension is what makes UPS appealing for employees, while the contribution-based structure keeps it more sustainable for the government than OPS.

But the UPS isn’t without its critics.

One sticking point is its inflation indexation, which is tied to the ‘All India Consumer Price Index for Industrial Workers (AICPI-IW)’. Simply put, this index measures the rise in the prices of goods and services to help the government determine minimum wages or make necessary pay revisions to account for inflation. But many argue that this index doesn’t accurately reflect the real cost of living for retirees, especially in terms of healthcare and housing costs. A broader inflation index could better ensure that pensions keep up with actual expenses.

Another issue is the conflict between the Centre and states. Despite the Centre’s push for UPS, some states are hesitant to opt for it. Why? Because the OPS, while financially unsustainable, is a political goldmine. Fixed pensions are incredibly popular among government employees, and offering them can win votes. States like Rajasthan have reverted to OPS, and for them, UPS doesn’t seem as attractive.

Plus, states that switch back to OPS can defer financial responsibility. It’s because they don’t need to set aside pension funds immediately. They can postpone these expenses till the time it actually becomes due, which makes their short-term finances look better. UPS, on the other hand, requires setting aside a guaranteed reserve fund right away, reducing the money available for other expenditures in the short term.

And all this leaves us with the last bit of this puzzle – How do we solve India’s pension conundrum?

Well, India could take inspiration from other countries’ successful pension schemes.

For example, Germany and Denmark have raised the retirement age to ease the strain on their pension systems. New Zealand has a universal pension scheme that guarantees every citizen a basic income post-retirement, regardless of their employment history. Chile, meanwhile, manages pensions through private funds, giving retirees more control over their savings while reducing the government’s fiscal burden.

India could do some of these tweaking in the upcoming schemes, and perhaps combine public and private sector management of pension funds.

And as we said before, the UPS, while an improvement over NPS, could be further enhanced by revisiting its indexation. Basing it on a more accurate consumer price index or the income growth in society, as seen in Sweden, would ensure retirees are better protected from rising costs.

But for now, UPS remains a work in progress and India remains in a tug-of-war between fiscal sustainability and political populism.

We’ll have to wait until 2025 to see the response UPS gets and if it truly delivers on its benefits.

Until then…

Don't forget to share this story on WhatsApp, LinkedIn and X.

📢 Ready for even more simplified updates? Dive into Finshots TV, our YouTube channel, where we break down the latest in business and finance into easy-to-understand videos — just like our newsletter, but with visuals!

Don’t miss out. Click here to hit that subscribe button and join the Finshots community today!

Story Sources: Data Commons [1], Business Standard [2], Economic Times [3]

Don't let medical bills break the bank!

Most Indian families are just one major medical bill away from bankruptcy. That’s why having the right health insurance is so important. Whether you’re looking for a new plan or want to review your current one, Ditto’s IRDAI-certified advisors are here to help.

Click here to book a FREE call today!