How did Dubai become the 'City of Gold'?

In today’s Finshots, we tell you how Dubai became one of the largest gold hubs in the world.

But before we begin, if you’re someone who loves to keep tabs on what’s happening in the world of business and finance, then hit subscribe if you haven’t already. If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

When geopolitical tensions rise, there’s one favourite topic we always like to talk about — safe haven assets. When markets turn shaky, investors usually rush out of equities and look for safer places to park their money. That often means government bonds, a strengthening US dollar, or the all-time favourite: gold.

Today we’ll talk about gold because something unusual has been happening in the world of gold over the past week.

According to the London benchmark, gold prices have actually slipped from about $5,300 per troy ounce (around 31 grams) to roughly $5,000. And that’s odd, because times of geopolitical stress usually push investors toward gold, not away from it.

One reason for that is the fact that gold had already rallied sharply in the past few months. And after such a strong run-up, buying it suddenly didn’t look as attractive. At the same time, rising interest rates on US bonds and a strong dollar began pulling investors in that direction instead. Because unlike gold, bonds actually pay interest, so when yields rise, they become a more appealing option.

There’s another thing too. When equity markets fall sharply, many investors face margin calls on their trading accounts. To cover those losses, they often need quick cash. And one of the easiest assets to sell in a hurry is gold. So when investors start liquidating their gold holdings, it creates widespread selling pressure, pushing prices down further.

But there’s also a less obvious factor behind gold’s recent behaviour — Dubai.

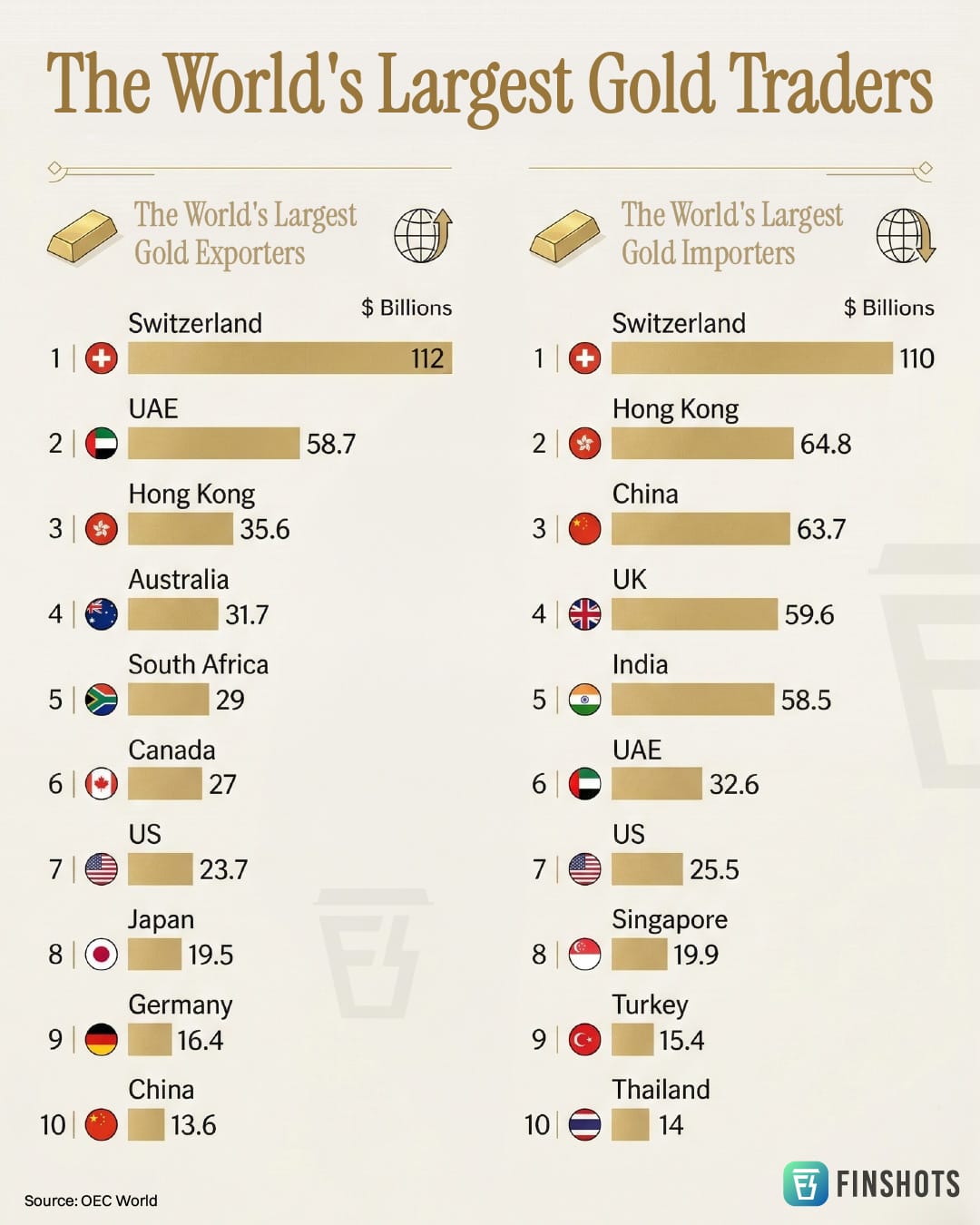

Dubai is one of the world’s most important gold trading hubs. In fact, about 20% of the world’s gold passed through Dubai last year, making it the second-largest hub after Switzerland.

The problem is that the recent tensions in the Middle East triggered by the US-Iran-Israel war, have disrupted cargo movement in the region. Dubai imports gold from African countries like Mali, Ghana, Guinea, Sudan and South Africa. And after refining it, much of that gold is shipped to major demand centres like India, often via cargo on passenger flights.

But with airspaces closed, that flow has slowed. Besides, keeping large quantities of gold sitting in vaults isn’t cheap. Storage and insurance costs start piling up. So to move inventory faster, traders in Dubai have apparently begun selling gold at discounts of up to $30 per troy ounce compared to the London benchmark. For context, that’s roughly ₹100 cheaper per gram.

So between higher bond yields, forced selling by investors, and discounted gold being sold in Dubai, the metal’s price has been behaving a little differently than usual.

But that also makes you ask, “How did Dubai become such a powerful hub in the global gold trade despite not producing any gold itself?”

Well, let’s take it from the top.

Long before skyscrapers pierced Dubai’s skyline, the city was nothing more than a sun-scorched settlement built around a saltwater creek. We’re talking about the early 1900s. Back then, Dubai made a living from pearl diving, fishing and small coastal trade. The population was modest too, so gold was barely in the picture.

But its geography had a different fate carved out for Dubai. If you look at the map, you’ll see that it sits neatly along the Persian Gulf, with India to the east, East Africa to the west, and Europe accessible through the Gulf and Persia to the north. Naturally, trade routes began to converge here.

So Indian and Iranian merchants started using Dubai Creek as a stopover on the route between Gulf ports, the Indian subcontinent and Persia. And wherever traders gather, markets tend to follow. That’s how a small gold trade slowly emerged around these merchants, with a handful of jewellers setting up shop along the old spice trading routes. That’s the very place we now know as the Gold Souk in Dubai’s Deira.

The ruling Al Maktoum family spotted this opportunity and decided to capitalise on it by abolishing taxes on imports and exports. That effectively turned Dubai into a free port, which meant that foreign merchants began pouring in. The population doubled. Goods began to flow in volumes Dubai had never seen. And among those goods, increasingly, was gold.

But that was only the beginning, and the rise of the gold trade hadn’t really begun until two things happened.

The first had a lot to do with us Indians and our love for gold. For many families in India, gold has always carried deep cultural value. Gold always showed up in weddings, festivals, as a symbol of family wealth and even our mothers’ dowries (which aren’t a thing of pride; please don’t give, take, or encourage them).

But around the 1940s and especially after independence, India imposed strict controls on gold. The government restricted gold imports and even tried to limit how much gold individuals could hold. The idea was to reduce demand by making gold harder to access.

Except it didn’t quite work that way.

Instead of killing demand, it simply pushed the trade underground. Gold smuggling surged. And because of those restrictions, a massive price gap opened up between Dubai and India. In some cases, the same gold could sell for almost double the price in India.

Dubai’s merchants spotted the opportunity instantly and began moving gold to India via boats, with buyers collecting their cargo in international waters near the Indian coast.

By the 1960s, Dubai had become a major centre for gold trading. Much of the gold flowed in from London, which at the time was one of the world’s key bullion markets. To give you a sense of scale, in 1968 alone, Dubai imported £56 million worth of gold.

But its true transformation into the “City of Gold” began when oil was discovered in Dubai around the same time. Oil wealth allowed the city to build serious infrastructure. The creek was widened so large vessels could dock. Ports, dry docks and an international airport soon followed. And because taxes remained low and trade was still largely unrestricted, Dubai became even more attractive for merchants.

Then came another unexpected boost. A civil war broke out in Lebanon, which until then had been one of the Middle East’s leading financial and trading centres. As conflict spread, many of Lebanon’s gold traders, bankers and commodity merchants fled the country looking for a safe space. Dubai welcomed them with open arms. And almost overnight, the city gained an entire ecosystem of trading expertise.

As more traders arrived, gold volumes kept growing. The once modest Gold Souk in Deira expanded into a glittering marketplace filled with 22-karat necklaces, bangles and jewellery, eventually housing over 300 retailers.

And that’s when the nickname truly stuck. Dubai had become the City of Gold.

Modern policies helped strengthen its position even further. In 2002, for instance, the UAE government set up the Dubai Multi Commodities Centre (DMCC) — a free zone designed specifically for commodity trading, including gold. Over time, it grew into the world’s largest commodities free zone, eventually hosting more than 1,800 companies involved in gold trading, refining and manufacturing.

A few years later came the Dubai Gold and Commodities Exchange (DGCX), which gave institutional investors a regulated platform to trade gold futures.

But the real cornerstone of Dubai’s gold trade still remained its tax policies. While buyers in many European countries pay 15–20% in taxes on gold purchases, Dubai traditionally imposed none. A 5% VAT was introduced only in 2018. And even that is refundable for tourists at the airport.

Dubai has also tried to build credibility around its gold ecosystem. Its refineries now meet the strict standards of the London Bullion Market Association (LBMA). And the DMCC’s “Dubai Good Delivery” standard aims to ensure that gold passing through the emirate is responsibly sourced and ethically certified.

That said, the gold trade in Dubai hasn’t been without controversy. The UAE, including Dubai, has often been accused of being a major destination for gold smuggled out of Africa. For context, a report by Swissaid estimated that around 435 tonnes of gold worth about $31 billion left Africa undeclared in 2022 alone, much of which may have reached the UAE. That’s roughly 40% of the continent’s production, or about 12% of global mined supply.

But yeah, no trade comes without its downsides. What’s undeniable, though, is how a city with no gold mines of its own managed to become the world’s second-largest gold hub, with nearly 1,500 tonnes of gold passing through it every year.

And Dubai isn’t done yet. To make this moniker even more evident, there’s chatter that it may soon build an 800-metre-long street lined with gold in the city’s new gold district in Deira, right where the Gold Souk is located (with over 1,000 retailers today).

How that plays out for Dubai will likely depend on how the Middle East crisis unfolds.

Until then…

Note: An earlier version of this story included a Middle East map that showed an incorrect depiction of India to its east. We apologise for the error and have since replaced it with the correct version from the Survey of India.

Liked this story?

Share it with a friend, family member or even strangers on WhatsApp, LinkedIn, or X.

Did you know? Nearly half of Indians are unaware of term insurance and its benefits. Are you among them?

If yes, don't wait until it's too late.

Term insurance is one of the most affordable and smartest steps you can take for your family’s financial health. It ensures they do not face a financial burden if something happens to you.

Ditto's IRDAI-Certified advisors can guide you to the right plan. Book a FREE consultation and find what coverage suits your needs.

We promise: No spam, only honest advice!