Finshots Cracks Crypto #1: What are blockchain and cryptocurrency anyway?!

In today’s Finshots, we kick off the Finshots Cracks Crypto series and break down the basics of cryptocurrencies, blockchain and Bitcoin!

Just a heads-up though. These stories from the series won’t be your usual short reads. Instead, we’ll dive deep into cryptos and the technology behind them, breaking it down step by step. So, grab a cup of coffee or chai, settle in, and let’s get started.

The Story

In the 1860s, Britain had a strange law called the Red Flag Act which said that every car had to move very slowly and have three people with it. A driver. An engineer. And one person walking in front waving a red flag to warn people. Yup, no kidding! Imagine someone walking ahead of your car today with a flag. It sounds nuts. But back then, cars were new, scary, and seen as dangerous as dynamite. And the law was supposed to keep people safe, but instead, it slowed down progress. While Britain stayed stuck, other countries moved ahead, improving cars and changing transportation forever.

The point? Revolutionary ideas often seem scary at first. They’re dismissed as risky fads, but their progress is usually unstoppable.

Doesn’t this remind you of how people talk about Bitcoin and blockchain today? Just like the first cars, they’re new, unfamiliar and mistrusted. Critics call Bitcoin a bubble, blockchain a gimmick and cryptocurrencies a playground for criminals. But could ignoring these technologies mean missing out on something amazing?

Let’s unpack a few things to answer this. And to do that, we’ll start with the foundation: blockchain.

Picture a classroom. The teacher keeps attendance on a single sheet of paper. But what happens if the sheet is lost or someone fudges the entries? Big problem, right? So, the students come up with a better idea: everyone keeps their own attendance sheet. And every time a name is marked, the whole class updates their sheets too. So if someone tried to cheat, it’d be easy to catch because everyone else’s records would expose the discrepancy.

That, in essence, is how blockchain works. It’s a system where everyone has the same copy of a record, and changes are nearly impossible without everyone noticing. Plus, it’s decentralised, meaning no one person or entity owns it. Just like every student in the class had a copy of all the records, the responsibility to check all the data on the blockchain lies with something called nodes. Simply put, these are computers that validate and manage data on the blockchain.

But how does blockchain actually work?

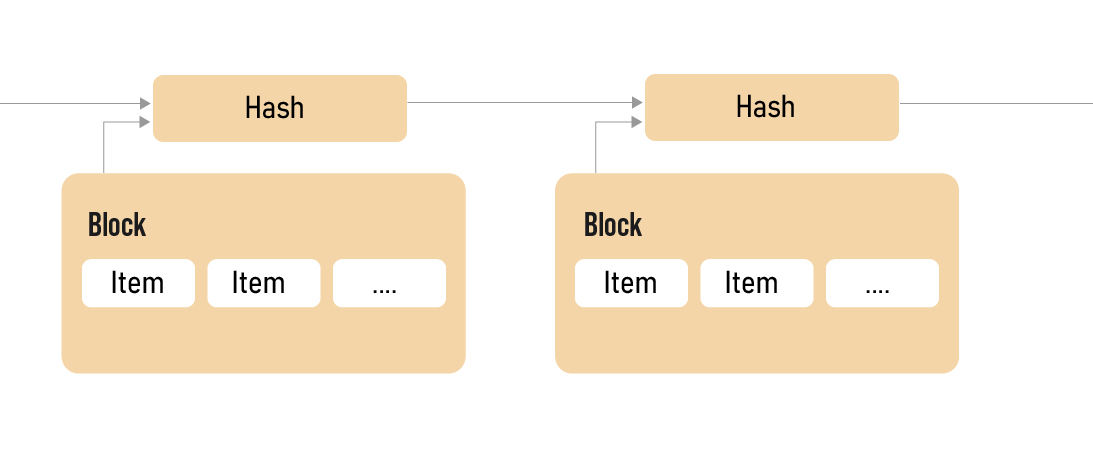

Well, the magic lies in its structure. Think of blockchain as a digital account that groups transactions (like attendance marks) into “blocks”. And each block is connected to the previous one, forming a continuous chain. (So block + chain = blockchain. Voila!)

Now, to keep everything secure, each of these blocks has a unique code called a “hash” ― a kind of fingerprint. And this hash is tied to the previous block’s hash, thereby creating a chain that links all the blocks together. So, if someone tries to mess with a block even in the tiniest manner, its hash changes and it breaks the entire chain and sets off alarms to everyone on the blockchain network. So, it’s like a tamper-proof vault that’s constantly being watched by everyone.

Adding new blocks isn’t easy either. It requires solving complex mathematical puzzles through a process called mining.

What’s mining, you ask?

Well, it’s where millions of computers worldwide race to solve a super-complex puzzle (we’ll come back to this in a bit). The first one to crack it gets to add a new block to the chain and earn cryptocurrency (cryptographic currency) as a reward. And here’s where it gets fascinating. The puzzle involves generating a 256-bit hash, a unique digital code. Think of it like a lottery where each guess requires massive computation power. And this whole process, dear reader, is something called a consensus mechanism (something they term as proof-of-work mechanism for Bitcoin and proof-of-stake mechanism for Ethereum) which ensures that the network remains honest.

But what happens if a node cheats? Well, that’s close to impossible. Because to manipulate a chain a hacker would need more computing power than the rest of the network that’s been previously established, combined. It’s a cost so astronomical it’s not even worth trying and downright unrealistic. This clever design makes blockchain a fortress of security.

In short, it’s like trying to rewrite history while everyone else is watching.

And speaking of history, let’s talk about Bitcoin — the first big use of blockchain technology!

Because well, if we’re talking cryptocurrencies, we can’t ignore bitcoin. Today it’s the reigning champ, commanding over 50% of the total cryptocurrency market with around $1.96 trillion market capitalisation. From humble beginnings, it has climbed to touch the $100,000 mark this year — a staggering achievement for any asset class in such a narrow time and for something once dismissed as a passing fad.

(Quick note: Bitcoin (with a capital B) is when we’re talking about the network or system. And when we say bitcoin (with a lowercase b), we’re referring to the currency itself)

In 2008, someone using the name Satoshi Nakamoto shared an idea for Bitcoin by publishing a groundbreaking whitepaper. It was introduced as a peer-to-peer electronic ledger system, sort of a new kind of money that didn’t need banks or governments. And it emerged during the global financial crisis when trust in traditional financial institutions had hit rock bottom. Bitcoin offered a decentralised alternative ― a currency that didn’t rely on banks or governments to be controlled but on mathematics and code.

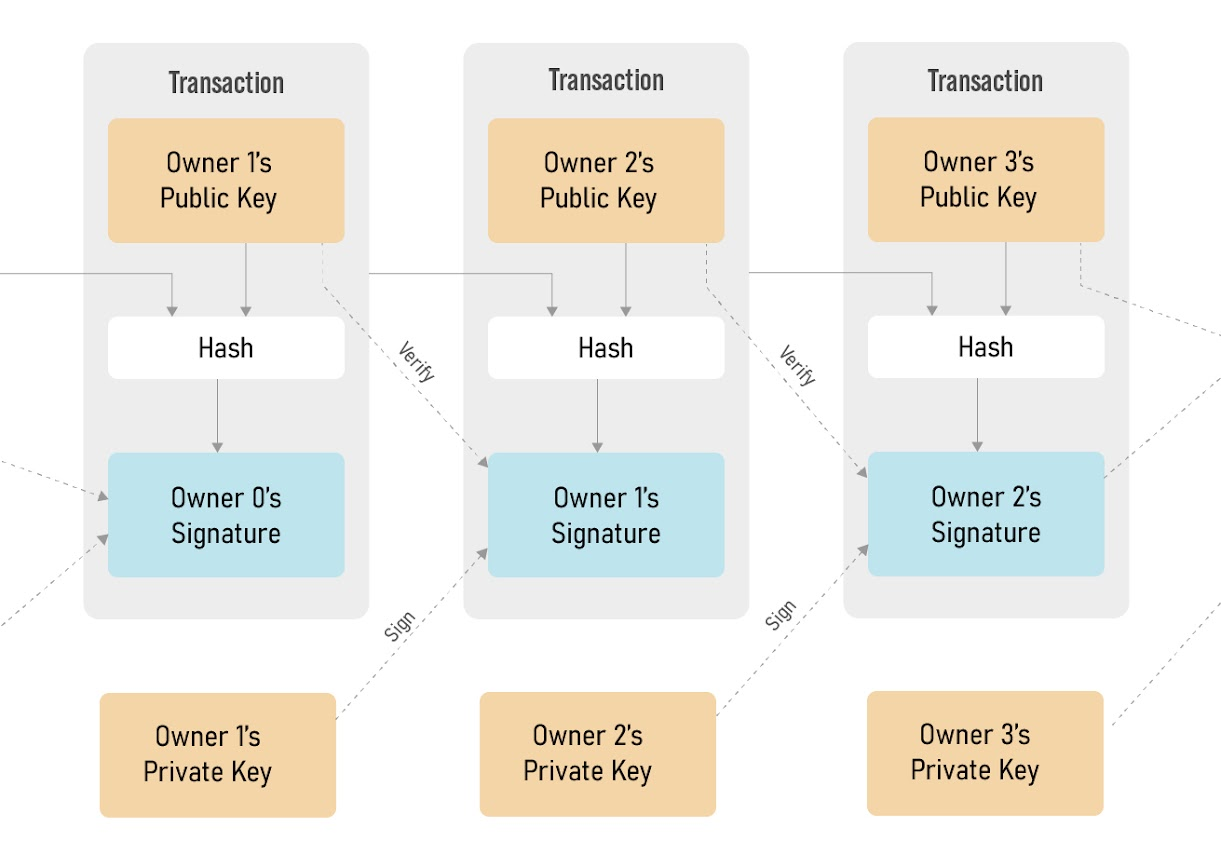

And to make this simpler, let’s first understand how this correlates with the blockchain tech and terms we just went through.

Bitcoin is built upon a unique network architecture. It works like a digital ledger that keeps track of who owns what. Think of each bitcoin as a chain of records showing its journey from one owner to the next. When someone sends bitcoin, they sign it with a unique digital signature, like a secure stamp, and link it to the next owner’s digital address. This process adds a new record to the chain, creating a clear and tamper-proof history of ownership.

To give you a visual representation, here’s how the process would flow…

What about trust though? Because in a normal world, we’d depend on a bank to make sure no one spends the same money twice. How do we do it on the Bitcoin blockchain?

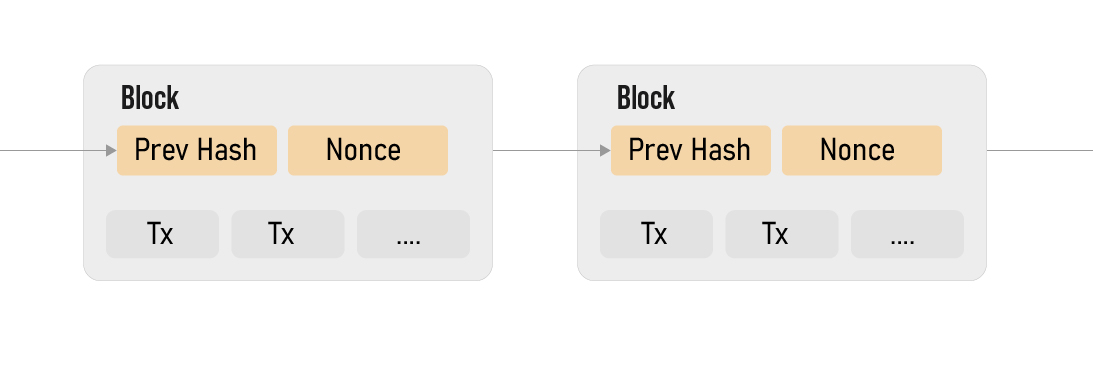

Well, Bitcoin changes all that because it uses a decentralised network where transactions are shared publicly, and everyone agrees on their order. This consensus mechanism removes the risk of double spending. Remember that super-complex puzzle we mentioned earlier? Here’s how it plays out on the Bitcoin network ― Each block bundles transactions, has its own unique hash, and includes a special number called a nonce. Miners adjust the nonce to solve a complex puzzle. And when one of them gets it right, the others validate it, and the block is locked into the chain. And that’s how this clever system makes every transaction transparent and secure.

Now, Bitcoin’s got a few sleek features.

First, it has no central authority. No one can block or reverse your transactions. Because, well, it’s built on the blockchain network. In regular banking, authorities can freeze accounts or stop payments. But Bitcoin’s decentralised system means no single authority has that power because it has peers or nodes validating transactions across networks. This is especially helpful in unstable economies. For example, during Argentina’s 2019 financial crisis, when the peso lost value, many turned to bitcoin to escape from currency swings or inflation. If you have questions on this, don’t worry, we’ll explain more on this in the upcoming chapters. But for now just know that Bitcoin is considered a sort of hedge against inflation.

Then it’s borderless and cost-effective. Usually, remittances to another country costs a lot and that’s how the banking industry makes money off your transactions. But with Bitcoin, it’s with no censorship and cheaper.

And because blockchain is programmable, cryptocurrencies like bitcoin can be used for things like smart contracts — agreements that automatically complete themselves. Imagine your car paying for its own charging or a fridge ordering and paying for groceries. These ideas could get real, thanks to blockchain.

But Bitcoin isn’t just about technology. It also challenges the very idea of how we think about money. Today, we trust some sort of authority to manage money. Bitcoin asks, what if we trusted math and code instead? By using private and public keys, similar to public usernames and private passwords, it removes the need for any middlemen. These keys let you securely send and receive money directly, without anyone else interfering. Bitcoin puts control back in your hands.

To top it off, it’s got a fixed supply — only 21 million bitcoins will ever exist, and as we said, it’s controlled by code, not people or central banks or policymakers. This scarcity makes it akin to digital gold. And it’s something that makes it deflationary in today's ever-increasing inflationary environment.

Of course, Bitcoin isn’t perfect. Its proof-of-work mechanism requires vast computational resources and therefore vast energy, and its volatility makes it less practical as a stable medium of exchange. But these challenges aren’t insurmountable because it’s worth remembering that the early days of the internet were fraught with challenges too. Yet, we persisted, and today, it seems indispensable.

So, to truly appreciate blockchain, let’s revisit a fundamental question: What is money?

Well, at its core, money is a social construct, a form of communication and a tool to facilitate exchange, store value and measure worth. Over time, money has evolved, from gold coins to paper bills to digital payments. And blockchain could represent the next step in this evolution: a form of money native to the digital age, unbound by geography or politics.

Yet, bitcoin’s true value lies in its ability to democratise finance. In regions where access to banking is limited, Bitcoin can provide an alternative. It’s not just money; it’s a tool for financial inclusion. Anyone with internet can have bitcoin without any service provider. In places where banks aren’t available, it can act as the bank itself!

So to sum it up, what truly sets bitcoin apart are some of these astounding properties. The digital currency isn’t tied to any physical form. It exists only as data, making it incredibly versatile. Store it in a hardware wallet, write it down on a piece of paper, or even encode it into a QR code. Its form adapts to how you choose to handle it! It can move at the speed of the internet, bypassing borders and bureaucracy. And your private key is all you need to access it. You memorize your private key, and your Bitcoin effectively hides in your brain! It’s there but invisible, safe from anyone who doesn’t know the spell (your private key).

Surely a new way to think about ownership, control, and freedom, eh?

So it'd be fair to say that Bitcoin and blockchain are still in their early days. Governments are grappling with how to regulate them. Some are welcoming it, others are banning it, and many don’t know what to do yet. But history shows that resistance to revolutionary ideas is often temporary. Electricity, cars, phones and even the internet all went through this. Maybe Bitcoin and blockchain might follow the same trajectory, or they might fall flat.

But one thing we know for sure is that this technology is something that’s been created and it can’t be undone. Imagine trying to unbake a cake once it’s out of the oven — you simply can’t, right? While its value might ebb and flow, the technology’s potential and its use cases are undeniable. Maybe that’s what we could learn from the Red Flag Act and embrace the possibilities instead of just getting hooked to the price movements.

We’ll end this chapter on that note.

In the next part of this series, we’ll look at the history of money — how trust, scarcity, politics and innovation have shaped the way we perceive, use and are bound by it in many ways. Because to understand where we’re going with cryptos, we need to know where we’ve been.

Until then…

Do give us a shoutout and share this story on WhatsApp, LinkedIn and X.

🚨ATTENTION: FINSHOTS FAMILY

Want to secure your family’s future in 2025?

Our free webinar on life insurance could be your first step!

📅 When? Saturday, 18th January

⏰ What time? 12:00 noon

We’re hosting an EXCLUSIVE session on one of the most important financial topics out there — LIFE INSURANCE.

Here’s what’s in store:

✔️ How to protect your wealth

✔️ The 5 biggest life insurance mistakes to avoid in 2025

✔️ Expert advice tailored for young Indians

✔️ Pro tips for creating a long-term financial plan

✔️ A breakdown of Endowment Plans, ULIPs and Term Insurance — which is better?

Click here to register now. Only 500 spots available! Don’t miss out.

Pro Tip: We’re expecting a big audience of over 400 attendees! Join early to ensure a smooth entry and secure your spot.