The Economic Survey 2024 Explained

In today's Finshots we offer a simplified analysis of the Economic Survey 2023-2024

Before we begin, if you're someone who loves to keep tabs on what's happening in the world of business and finance, then hit subscribe if you haven't already. We strip stories off the jargon and deliver crisp financial insights straight to your inbox. Just one mail every morning. Promise!

If you’re already a subscriber or you’re reading this on the app, you can just go ahead and read the story.

The Story

Yesterday, the Finance Minister Nirmala Sitharaman tabled the annual Economic Survey in the Lok Sabha. And it’s kind of a big deal for us here at Finshots. Because it gives us a glimpse into where the economy is headed. And this year’s survey has its fair share of interesting observations.

So let’s get straight into it.

The most controversial aspect of the report can be traced back to a few lines in Chapter 2.

We won’t quote the excerpt here. But it simply says a lot of new, young investors are jumping into the stock market because they've seen prices going up and think this will continue. They might be a bit too optimistic, expecting huge returns without fully understanding that the market can go down too. And if people were to liquidate their savings and deposits in an attempt to make money off the stock market, this could have real life implications for them and the banking ecosystem too. After all, if banks can’t mobilise deposits, that could affect borrowers and so on.

This has got a few people talking. Is it true that people are funnelling their savings to the stock market?

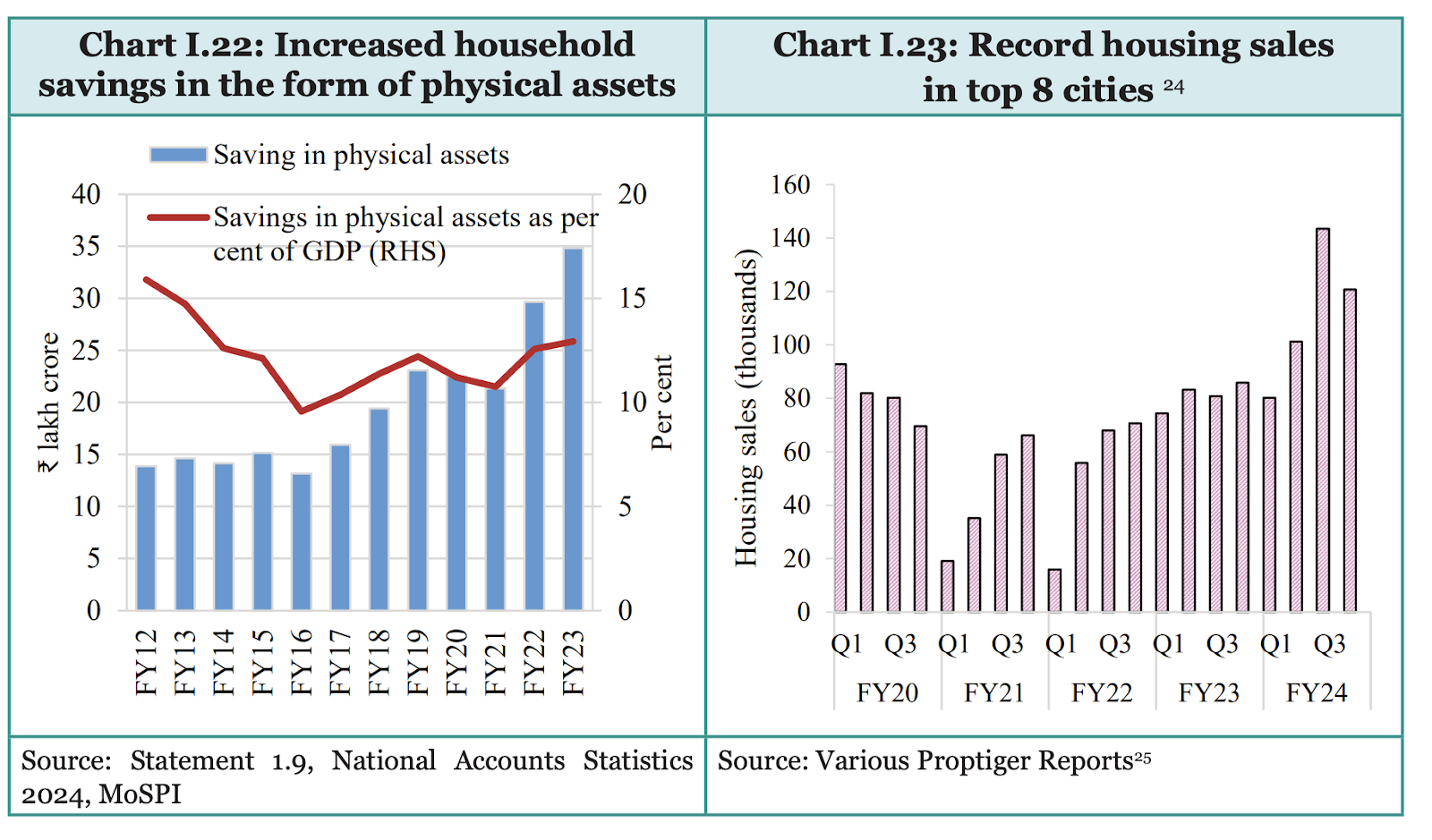

Well, kind of. This has been a spectacular year for Mutual Funds with total assets under management growing by nearly 35% to ₹53 lakh crores. This means that India is increasingly warming up to the idea of fully embracing financial markets. However, some investors have also found an opportunity to sell their holdings (thanks to the spectacular rise in stocks) and park it in Real Estate investments.

In 2023, residential real estate sales in India were at their highest since 2013, witnessing a 33 per cent growth, with a total sale of 4.1 lakh units in the top eight cities.

Now you could look at this data and argue that some of the household savings is moving away from banks. But you could also argue that this is a smart diversification strategy. This money is going into mutual funds. It’s going into real estate. And it’s what people in most developed countries do.

So this is a cue for banks to improve their offerings. Maybe it’s time to up the interest on savings deposits instead of moaning about the fact that people are looking out for their own best interests.

Okay, next on to inflation. There’s nothing really significant here. India managed to control inflation better than most countries since Covid. Yes, you had the occasional rise in prices–tomatoes, tur daal, milk, but you could pin most of it down to adverse weather conditions. This has been a feature of India’s inflation story. Bad weather translates to higher prices and the report accurately notes that the government may need to promote the cultivation of pulses in more districts (and in areas with assured irrigation facilities). And maybe also invest in better storing and processing facilities to stop all that food wastage.

There is also an interesting mention about edible oil. The domestic consumption of edible oils has been increasing faster than production, leading to increased import dependence. And yeah, that does not bode well for our future. So we probably need to look at that.

Then there’s the stuff around employment. Employment prospects in India have improved no doubt. Almost every indicator points to this aspect. But there is the elephant in the room. Only 4.4% of India's young workforce is formally skilled. This means that most young workers have not received formal training or education specific to their jobs. And this can be a big problem, especially considering India’s economic growth hinges on realising the potential of its young workforce.

Will AI play a role in this?

The economic survey doesn’t make any categorical conclusions. But it does offer some perspective.

It quotes the example of David Ricardo (a British economist) and his evolving views on technology and labour during the early Industrial Revolution. Initially, Ricardo believed that machinery wouldn't reduce the demand for labour. However, after observing the impact of technologies like the power loom, which replaced artisan weavers and reduced their wages, he revised his stance. By 1821, Ricardo suggested that if machinery could perform all tasks, it might eliminate the need for human labour altogether.

What's the moral of the story?

Well, perhaps the authors of the Economic Survey feel like we should be increasingly careful of deploying AI solutions in the workforce lest it replace human labour altogether.

Maybe there’s a need to strike a balance here.

There’s also a very important mention about unpaid work.

This invisible domestic work performed by women, which is usually neglected while calculating the labour force and the GDP, has been variously estimated as highly valuable yet invisible. But according to a recent report, it seems the economic value of women’s unpaid domestic and care work in India is 15 – 17 % of the GDP. That’s a lot isn’t it?

The document also places an explicit focus on climate change. Now there’s a lot to unpack here obviously. But considering this is a quick explainer in a 3 minute newsletter we will stick to one interesting detail we encountered —water conservation efforts.

In Navanagar, Gujarat, declining water levels due to farming led to unsustainable salt levels in the groundwater, making agriculture unprofitable. To address this, local farmers, with support from the Water Resource Department and the Gujarat Green Revolution Company, rejuvenated the village pond by connecting it to the Guhai Dam. They deepened the pond, built a sump for water storage, and installed water lifting facilities, bearing the cost themselves. They also introduced a piped water system and adopted drip irrigation, significantly increasing crop diversity and productivity while reducing water and power usage. This is an example where the community worked with public officials to solve a real problem precipitated by humans and climate change.

Also, needless to say, India aims to grow economically while reducing carbon emissions, which means balancing higher energy needs with cleaner, sustainable sources.

The document also spends considerable time extolling the virtues of the government and the progress we have made in many spheres of life. There isn’t much criticism or internal reflection if you were hoping for that kind of thing. But there is a beautiful passage that does offer some sage advice.

In the Preface the authors note -

The Indian state can free up its capacity and enhance its capability to focus on areas where it has to by letting go of its grip in areas where it does not have to. The Licensing, Inspection and Compliance requirements that all levels of the government continue to impose on businesses is an onerous burden. Relative to history, the burden has lightened. Relative to where it ought to be, it is still a lot heavier. The burden is felt more acutely by those least equipped to bear it – small and medium enterprises. It holds them back, leashes their aspirations, and, in the process, holds the country back. On the face of it, it does not seem to matter because the economic growth rates are good, and there are visible signs of progress. But, we will never know the counterfactual: “what it might have been”.

Quoting the Ishopanishad the authors note - “Power is a prized possession of governments. They can let go of at least some of it and enjoy the lightness it creates in both the governed and the governing.”

Hopefully today’s budget captures this emotion.

Until then…

Don't forget to share this story on WhatsApp, LinkedIn and X.

📢Finshots is also on WhatsApp Channels. Click here to follow us and get your daily financial fix in just 3 minutes.

🚨Term Life Insurance Prices are About to INCREASE!

A prominent insurer is set to raise their term insurance rates in the next few weeks. This means if you don’t secure a term plan now, your premiums could significantly go up!

Here’s why this matters: When you purchase a term life insurance policy, you pay a premium or a small fee each year to protect against financial risks. In the unfortunate event of your passing, the insurance company pays out a substantial sum to your family or loved ones.

The best part? By buying early, you can lock in your premiums, ensuring they're not affected by any future rate hikes.

If you've been considering a term plan, now is the perfect time to act. To assist you in the process, our advisory team at Ditto is here to help. Click on the link here to book a FREE call with our IRDAI-certified advisors.