Are Indian banks underestimating the unsecured loan problem?

In today’s Finshots, we look at whether India’s easy credit boom is starting to show cracks.

Also, here’s a quick sidenote before we begin. This weekend, we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 4th April at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 5th April at 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.

👉🏽 Click here to register while seats last.

Now, on to today’s story.

The Story

A few years ago, getting a loan meant paperwork, approvals, and waiting. But today, it only takes a few minutes. A credit card gets approved instantly, personal loans are issued with a few taps, and buy now, pay later options are everywhere. Access to credit has never been easier than now.

And in a way, it’s a good thing. More access to credit means more consumption, more spending, and ultimately, more growth for the economy. It also brings first-time borrowers into the formal financial system, away from informal moneylenders. Ultimately, this gives people the flexibility to manage short-term needs without dipping into savings.

Banks and NBFCs have also actively pushed these products because they are high-margin, require no collateral, and scale easily through digital channels.

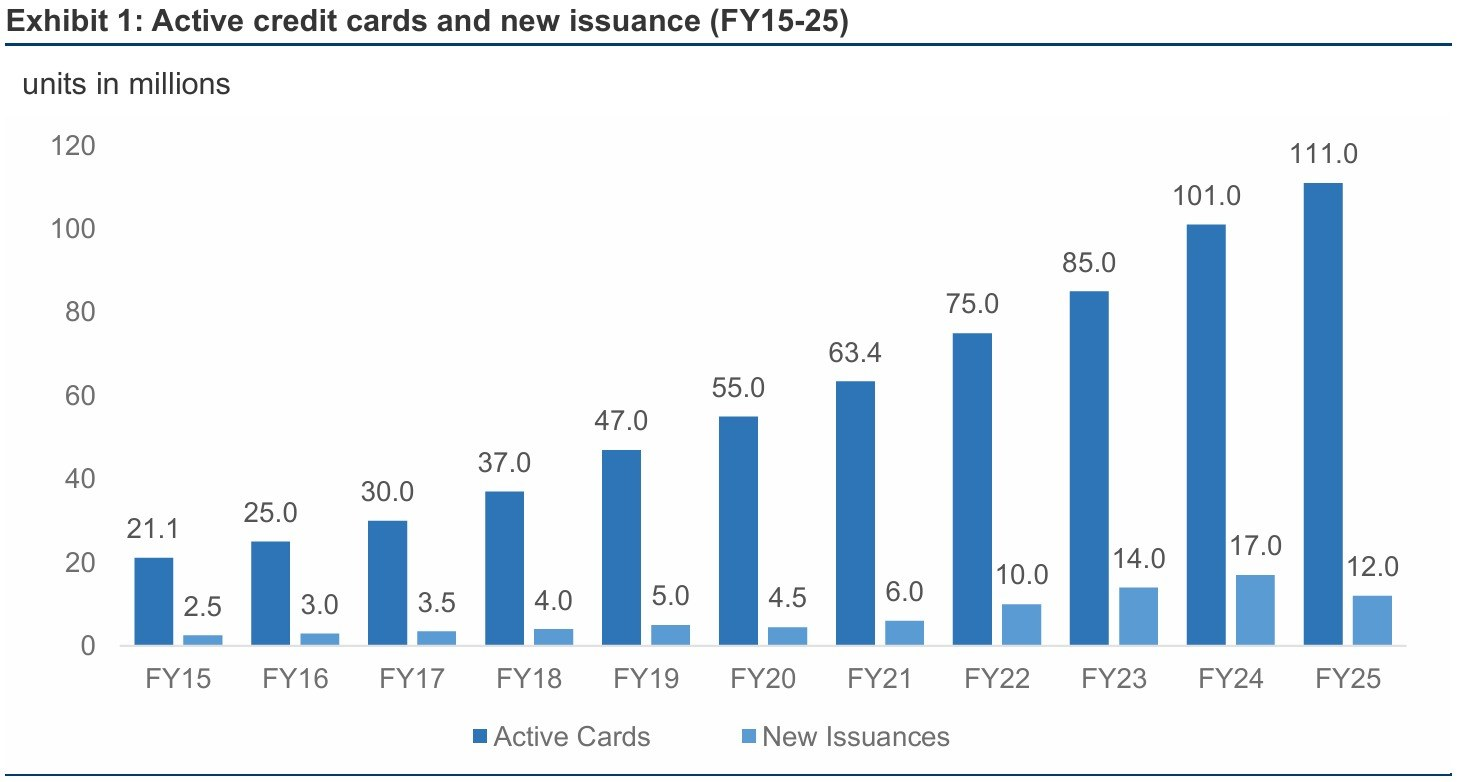

Let’s take credit cards, for instance: the number of cards approved has been steadily increasing over the last few years. From FY12 to FY25, the number of active credit cards surged 5x, and by the end of December 2024, there were over 100 million active credit cards in India.

And this is just credit cards. People have other kinds of loans, too. So, as the saying goes, too much of a good thing can also be a bad thing. Because when credit becomes this easy to access, it also becomes easy to overuse. And when millions of borrowers start taking on small loans at the same time, the risks don’t show up immediately. They build up slowly in the background. And that’s exactly what makes the current situation worth paying attention to.

The Reserve Bank of India has already flagged this trend. It has tightened norms by increasing risk weights on unsecured loans, meaning banks have to set aside more capital for every rupee they lend. Yet despite these signals, credit growth in this segment has continued.

Which raises a natural question: why are lenders still disbursing more loans?

To understand that, it helps to look at how credit cycles typically unfold.

In the early stages of a credit cycle, everything appears stable. Lending grows quickly, defaults remain low, and repayment behaviour looks strong. This creates confidence within the system, and banks expand further. In this stage, new borrowers enter the market, and credit becomes easier to access.

But, as we mentioned earlier, risks in unsecured lending tend to build slowly. The true risk emerges 18 to 36 months after the loan is disbursed. Credit card NPAs (non-performing assets) - which is essentially where cardholders have failed to make interest or principal repayments - have jumped by about 73% in FY22 and another 28% in FY24. And what this indicates is that loans originated 2-3 years ago are now cracking under stress.

This is because, unlike secured loans, there is no asset backing these loans. Repayment depends entirely on the borrower’s income. And when credit grows too fast, especially among first-time borrowers, risks slowly begin to build in the background.

So, when that stress starts to emerge, it often does so quickly, because multiple borrowers begin to struggle at the same time. (* couch couch * 2008 * cough cough *)

There are early signs of that stress beginning to show.

Retail lending, once considered one of the safer segments of banking, is now under pressure at the margins. Many first-time borrowers are managing multiple loans, often across different lenders.

At the same time, banks themselves are facing changing conditions. Deposit costs have been rising, which compresses margins. Regulatory scrutiny has increased. Growth, while still strong, is becoming more expensive to sustain.

Several banks have begun tightening their approach to unsecured lending following the RBI's warning. Credit card issuers, for instance, are recalibrating their customer base. Rewards are being reduced, fees are being adjusted, and low-value or high-risk users are being gradually discouraged. The focus is shifting toward retaining high-spending, low-risk customers who are more profitable and less likely to default.

A similar shift can be seen in areas other than credit cards, too. Take IDFC First Bank as an example. The bank is aggressively de-growing its microfinance (MFI) portfolio, with its share of the total loan book falling from 6.6% in March 2024 to 2.4% by December 2025. One can argue that this withdrawal is a response to the "over-indebtedness" and rising NPAs seen across the MFI sector in late 2024.

These kinds of withdrawals suggest that lenders are not ignoring the risks, which is a good sign.

However, the central tension is still unchanged - Banks continue to bet that strong economic growth will support repayments. And as long as incomes rise and employment remains stable, borrowers can continue servicing their loans. But if income growth does not keep pace with borrowing, or if households stretch themselves too thin, stress can build quickly.

But once a borrower defaults, recovery rates tend to be lower compared to secured loans. And that makes the system more sensitive to changes in borrower behaviour.

The concern, therefore, is not about an immediate crisis. India’s banking system today is far more resilient than it was in the past. Banks’ NPAs have declined from their earlier peaks, they hold better capital buffers, and regulatory oversight is stronger. But the nature of risk is also evolving. Instead of large corporate defaults, the next phase of stress could be driven by small household loans.

If defaults start rising, lenders may respond by tightening credit further. And since much of today's spending depends on easy credit, this could slow consumption. So, what begins as a financial-sector adjustment can spill over into the broader economy.

So, how can you, as a retail customer, come out ahead in this potential crisis?

First, treat easy credit like a trap, not a privilege. Just because your limit increases or a new card is instantly approved doesn’t mean you should use it. Use it only if you need it. Banks expanded their loan book aggressively when money was cheap. Now that they’re tightening, you don’t want to be caught over-leveraged when the tide turns.

Second, optimise for benefits while they still exist. If banks are cutting rewards and increasing fees, the smartest move is to actively evaluate your cards and accounts. Keep the ones that give you real value and don’t use the ones that don’t.

Third, protect your credit profile. As banks become more selective, high-quality borrowers will get better terms, while everyone else gets priced out. Paying on time, keeping utilisation low, and avoiding unnecessary loans will ensure you stay in the “profitable customer” bucket.

And finally, build your own safety net. If banks are preparing for a potential slowdown, maybe you should too. A solid emergency fund and lower dependence on credit can give you flexibility when lending tightens or costs rise.

Because in every credit cycle, the winners aren’t the ones who borrow the most. They’re the ones who borrow only when they need to.

Until then…

If you liked this story on India’s lending boom and the risks beneath it, share it with your friends, family or even strangers on WhatsApp, LinkedIn or X.

Also, if you’re someone who loves keeping tabs on the world of business and finance, hit subscribe if you haven’t already. And if you’re already a subscriber, thank you! Maybe forward this to someone who’d enjoy our stories but hasn’t discovered us yet.