Are G Secs really risk free?

In today’s Finshots, we take a look at whether government securities and bonds are really risk-free.

But here’s a quick sidenote before we begin. This weekend, we’re hosting a free 2-day Insurance Masterclass that helps you build real financial security by understanding health and life insurance the right way.

📅 Saturday, 21st March at 11:00 AM: Life Insurance

How to protect your family, choose the right cover amount, and understand what truly matters during a claim.

📅 Sunday, 22nd March at 11:00 AM: Health Insurance

How hospitals process claims, common deductions, the mistakes buyers usually make, and how to choose a policy that won’t disappoint you when you need it most.

👉🏽 Click here to register while seats last.

Now, on to today’s story.

The Story

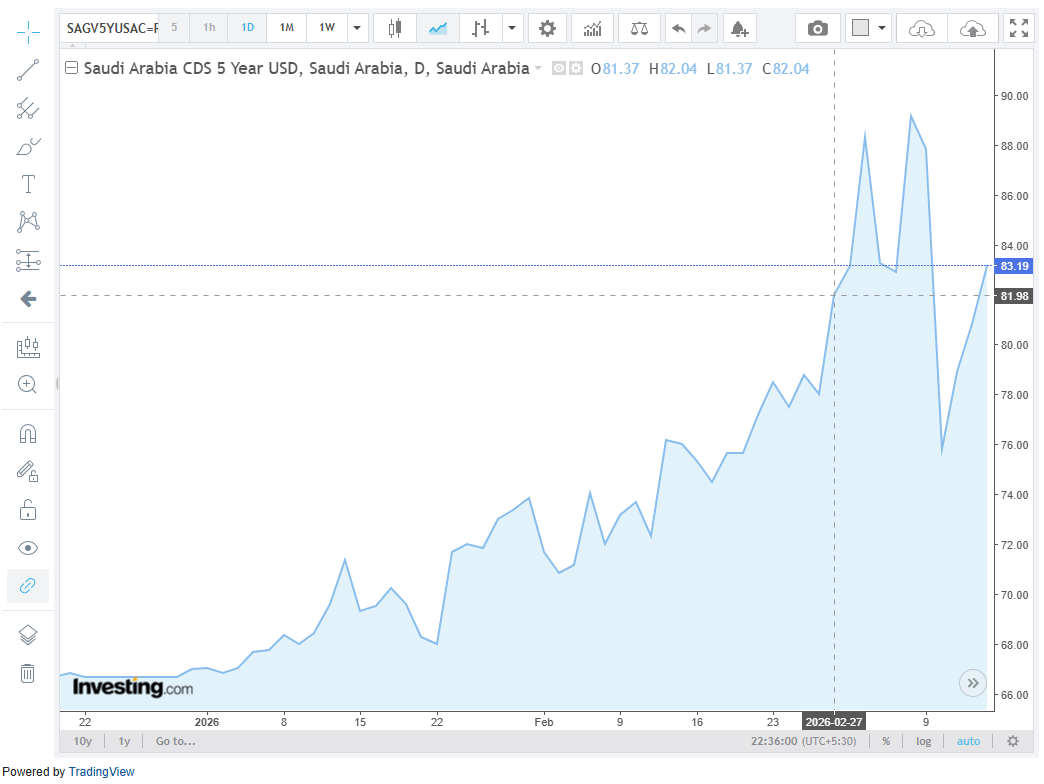

This is Saudi Arabia’s 5-year credit default swap rate. As you can see, it has been continuously increasing since the beginning of the year.

A credit default swap (CDS) is an instrument that’s used to insure against the risk that a borrower might not repay their debt.

At its core, it’s a simple idea. You lend money to someone. Then you go to a third party and say, “Hey, if this borrower defaults, will you cover my losses?” In exchange, you pay them a small annual fee. That fee is what we call the CDS spread.

What makes a CDS fascinating is not how it works. It’s basically just insurance for bonds. However, what it reveals is fascinating. Because investors don’t just buy this insurance on companies. They buy it on countries too.

You see, even stable economies have CDS spreads. If you look at something like Saudi Arabia’s 5-year CDS, it moves constantly. It rises when oil prices fall, when geopolitical risks flare up, or when fiscal conditions weaken. But it never drops to zero.

Which tells you something important: Markets never treat anything as perfectly risk-free. Not even governments.

And yet, in finance, we often hear the exact opposite.

Government securities are often described as the safest investment in the country. And for good reason. These are bonds issued by a country's government, meaning the borrower is the sovereign itself. Unlike companies, the government can tax, borrow, or even print more money to meet its obligations. So the probability of default is considered extremely low.

That’s why banks hold large amounts of G-Secs and why investors treat them as the “risk-free rate” benchmark for pricing everything from loans to equities.

But in practice, the “risk-free rate” only refers to the absence of default risk, not the absence of all risk. Because bonds, despite their reputation, are not always stable.

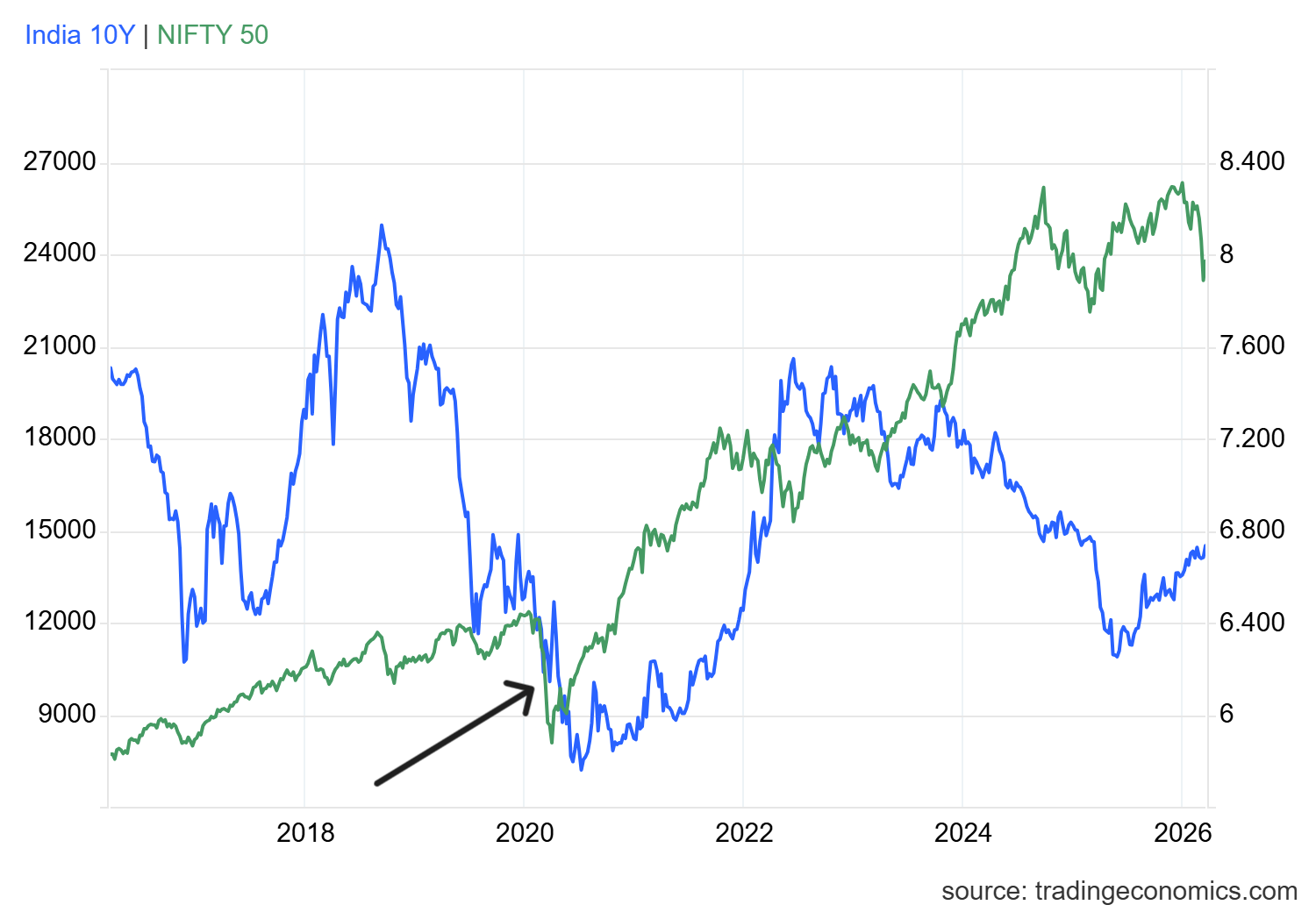

Under normal conditions, government bonds act as a hedge. When equity markets fall, investors typically move into bonds. Bond prices rise, yields (interest rate on the bond) fall, and bonds act as a cushion in the portfolio. This is why the classic 60/40 portfolio exists. 60% stocks for growth, and 40% bonds for safety.

But every now and then, that relationship breaks.

Take periods of geopolitical shocks driven by energy crises. In times like this, the stock market usually falls. And when war pushes oil prices higher, the expectation for inflation tends to rise, too. And instead of buying bonds, investors start demanding higher yields to compensate for that inflation.

Therefore, bond prices fall at the exact moment they’re supposed to protect portfolios.

As you can see, in 2020, during the pandemic, both the Nifty index as well as bond yields fell at the same time.

And we’ve seen this before in other markets, too. For instance, during the 1990 Gulf War, US bond yields initially spiked as oil prices surged. During the Vietnam War, US Bond yields rose steadily as government spending ballooned. And more recently, even in a world conditioned to buy the dip, bond markets have occasionally refused to play along when inflation risks dominate.

The logic is uncomfortable but clear:

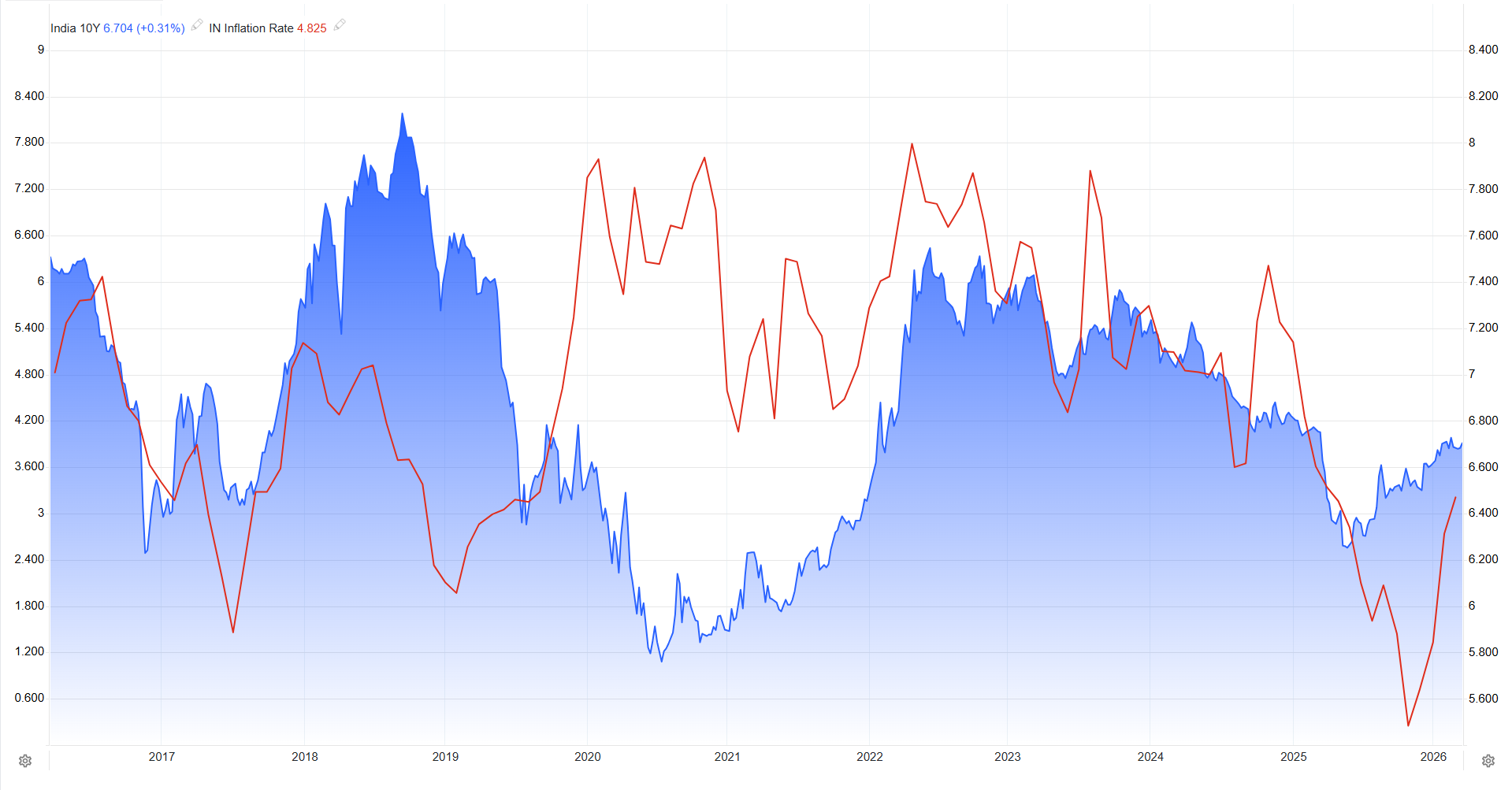

Government bonds are only safe if inflation is under control and fiscal conditions are stable. But when any event strains government finances, pushes up deficits, and fuels inflation, those very bonds start behaving like risky assets.

And that’s not the only problem.

Even outside crisis periods, G-Secs carry risks that investors often overlook. If interest rates rise, bond prices fall. If inflation remains elevated, the real return on a bond can turn negative. Even if investors receive all promised payments, the purchasing power of those payments may be significantly lower.

Liquidity risk can also matter. If an investor needs to exit before maturity, the bond may have to be sold at a loss depending on prevailing market conditions. In that sense, the path to repayment can be volatile even if the final outcome is certain.

Taken together, these factors show that government securities are not entirely risk-free. Bonds are largely free from default risk, but they remain exposed to interest rate movements, inflation, and broader macroeconomic conditions.

They tend to perform well in periods of stable inflation, predictable fiscal policy, and moderate to good economic growth. Step outside that environment, and their characteristics can change quickly. In inflationary or fiscally stressed conditions, they can behave in ways that are not very different from other financial assets.

This is also why the idea of a single universally safe asset is misleading.

Different risks are predominant at different times. So, when growth slows, bonds can provide stability. When inflation rises, assets such as gold, silver, and essential commodities may offer better returns. And in scenarios where both inflation and growth risks are elevated, even traditionally safe assets may struggle.

This is exactly where diversification comes in. Not the textbook version where you just hold stocks and bonds and assume they will offset each other. But a more practical version that recognises that different risks show up at different times.

That said, this doesn’t mean you need to constantly trade your portfolio or try to predict every macro shift. Consistently timing inflation cycles, interest rate moves, or geopolitical events is nearly impossible, even for professionals.

Instead, the idea is to build a portfolio that is already prepared for multiple scenarios. A mix of assets that respond differently to growth, inflation, and liquidity crunches can help reduce the impact of any one risk dominating at the wrong time.

So the next time someone calls G-Secs “risk-free”, maybe ask them:

Risk-free in what sense?

Because in investing, safety is always relative, and not absolute.

Until next time…

If you liked this explainer on bonds and macroeconomic risks, feel free to share this with your friends, family or even strangers on WhatsApp, LinkedIn or X. And subscribe to Finshots, if you haven’t already. Plis!